If you're running finance for a global startup, a DAO, or a fast-moving operating company, the pain usually looks the same. One team member needs to pay a SaaS bill in USD, another needs to settle a contractor invoice in EUR, and someone else has already put a personal card on a critical tool because procurement was too slow. By the time accounting closes the month, you've got wire confirmations in email threads, receipts in Slack, missing memos in spreadsheets, and FX surprises buried inside statement lines.

That setup breaks faster when the business grows across borders. It gets worse when part of your treasury sits in digital assets, part of your vendor base wants fiat, and your internal controls still depend on who remembered to ask in a chat channel before spending.

Virtual corporate cards solve a very specific operational problem. They turn spending from a loose reimbursement process into a controlled payment system. The reason this matters now is scale. The global virtual cards market is projected to grow from USD 6.43 trillion in 2026 to USD 15.14 trillion by 2031 at an 18.67% CAGR. That isn't just product hype. It's a signal that finance teams are rebuilding how business payments work.

Table of Contents

- Start with policy before cards

- Build approvals around exceptions

- Connect cards to your ledger and treasury stack

The End of Expense Report Chaos

The old workflow usually starts with good intentions. Finance wants centralized control, department leads want speed, and vendors want to get paid without friction. Then reality shows up. A founder in Lisbon books travel on a personal card because the corporate bank card is tied to someone in New York. A protocol contributor in Argentina needs software access today, not after a treasury committee reviews a wire. A Cayman entity pays a European service provider and discovers the payment cost wasn't the fee on the invoice. It was the fee chain around the invoice.

That kind of sprawl creates three problems at once. First, spending becomes hard to approve in advance. Second, reconciliation turns into detective work after the fact. Third, policy lives in documents instead of in the payment rail itself.

Virtual corporate cards change that operating model. Instead of handing out one broad funding credential and hoping people use it correctly, finance can issue a card for a specific vendor, project, user, amount, or time window. The payment method becomes programmable.

Practical rule: If a team can spend before finance can define the rules, your controls are cosmetic.

For global SMEs and web3 organizations, that shift matters more than it does for a domestic business with a simple AP stack. Cross-border vendor management adds FX decisions. DAO spending adds governance friction. Crypto-fiat workflows add timing risk. A virtual card won't solve every treasury problem, but it can remove a lot of operational mess from day-to-day spend.

The strongest teams don't treat these cards as a convenience feature. They treat them as infrastructure for controlled execution.

What Exactly Are Virtual Corporate Cards

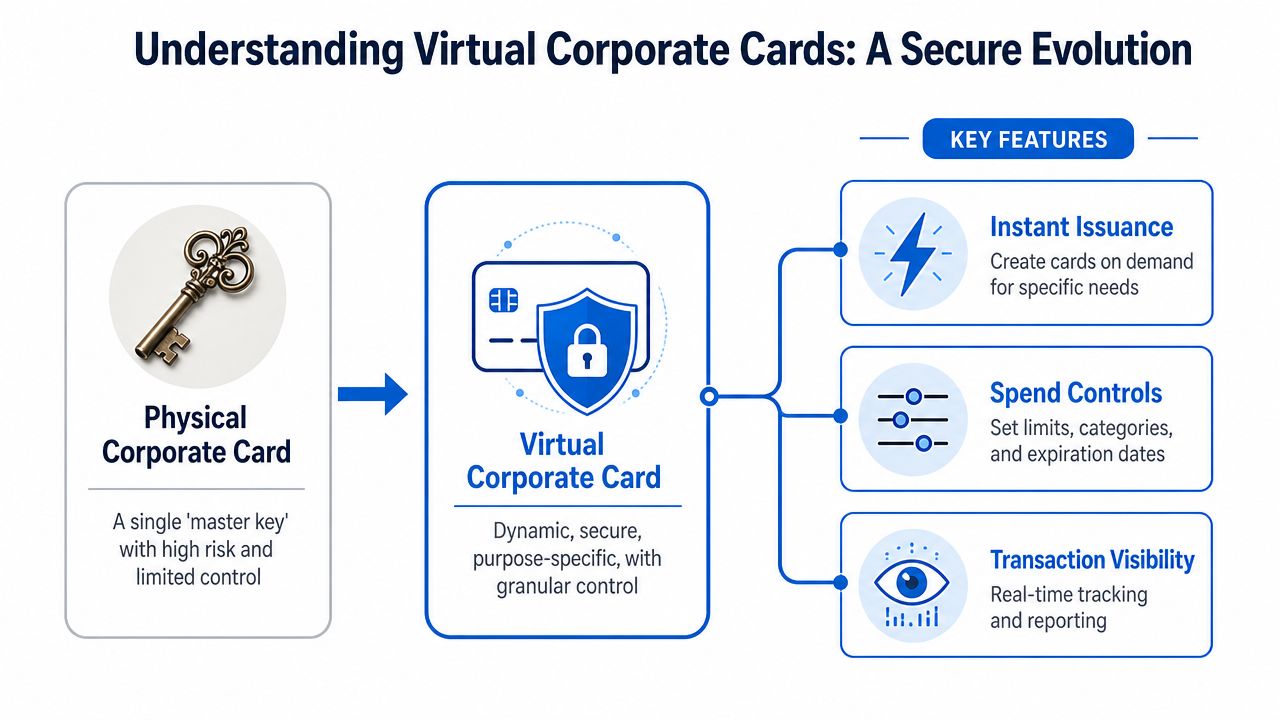

A physical corporate card is often used like a master key. It enables many purchases, across many merchants, for a long period of time. That's convenient until the key is copied, lost, or used in a way nobody intended.

A virtual corporate card is closer to a digital key issued for a defined purpose.

A better mental model

Each virtual card has its own 16-digit number, expiration date, and CVV, separate from the underlying funding source. That separation is the core concept. The vendor processes the virtual credential, not the primary account details.

This is why finance teams like them. You can create a card for one software renewal, another for ad spend, another for a contractor tool budget, and another for a short-term project. If one credential is exposed, the underlying funding source isn't the same thing as the number the merchant saw.

If you're comparing providers, the practical question isn't whether they offer virtual cards. Most do. The question is how much control you get over issuance, limits, merchant restrictions, approvals, and visibility. That's where the operating value sits. Teams evaluating card programs often start with a provider's virtual card controls and issuance workflow rather than just looking at the card itself.

The two card types most teams use

Most finance teams end up using two patterns.

- Single-use cards work best for one-off vendor payments, fixed invoices, or approval-sensitive purchases. They reduce reuse risk and make overcharging harder.

- Recurring cards fit ongoing software subscriptions, agency retainers, cloud services, and other repeat spend where the vendor is stable but the finance team still wants bounded control.

A simple way to decide is this:

| Spend type | Better card setup |

|---|---|

| One invoice, one vendor, fixed amount | Single-use card |

| Monthly tool or service with known owner | Recurring card |

| Short project with temporary budget | Time-limited virtual card |

| Shared team spend without a clear owner | Usually a process problem, not a card problem |

Use a virtual card only when you can name the owner, purpose, and budget. If you can't, don't issue the card yet.

The biggest implementation mistake is treating virtual cards like digital copies of plastic cards. They're not. Their value comes from specificity. The tighter the scope, the better the control.

Strategic Benefits Beyond Basic Payments

Virtual corporate cards matter because they give finance leverage without slowing operators down. That's why adoption is broadening beyond large enterprises. In 2024, SMB cards accounted for 63% of all global commercial card volume, equating to USD 2.7 trillion. Smaller teams aren't adopting these tools for prestige. They're adopting them because headcount is limited and mistakes are expensive.

Control that finance can actually enforce

Most spending policies fail because they're written after the purchase. Virtual cards let you put the rule before the transaction.

That means finance can define:

- Amount boundaries so a card can't exceed an approved budget.

- Merchant restrictions so a card meant for a cloud provider isn't suddenly used for travel.

- Time windows so project-based cards expire when the work ends.

- Role-based access so team leads can request or initiate spend without becoming full finance admins.

This is especially useful when teams operate across entities and currencies. A local manager may need autonomy, but not unrestricted access to the parent company's funds.

Visibility before month end

Month-end surprises usually come from delayed information, not bad intentions. A reimbursement submitted late, a recurring charge nobody owned, or an FX-heavy purchase booked without context can distort the close.

With virtual corporate cards, transactions hit systems in real time or near real time, depending on the provider and integration setup. Finance can tag expenses by vendor, project, wallet, department, or entity at the point of issuance instead of reconstructing the story later.

That visibility is one reason multi-entity finance stacks increasingly pair cards with multi-currency business accounts. The useful combination isn't just "pay by card." It's "pay by card from the right account with the right approval path and settlement context."

A fast-growing company doesn't lose control all at once. It loses control one unowned recurring charge at a time.

Efficiency that compounds

The operational gain isn't only fewer reimbursements. It's fewer exceptions.

When finance can issue cards instantly for a known purpose, teams stop improvising with personal cards, card sharing, or rushed bank transfers. Procurement gets simpler for low-risk purchases. Subscription management gets cleaner because every tool can have a named owner and dedicated credential. Offboarding gets easier because canceling spend doesn't require hunting through a wallet full of shared cards.

A few patterns work especially well:

Vendor-specific cards for software

Assign one card to each major SaaS vendor. If the tool is canceled, shut the card off. No need to reissue a broad company card across multiple systems.Campaign cards for marketing

Create a separate card for each paid channel or region. That keeps spend segmented and makes variance review easier.Project cards for web3 operations

Short-term grants, audit expenses, event logistics, and infrastructure purchases often need quick execution with a clear cap. Virtual cards fit that model well when the spend begins in fiat but treasury oversight includes digital assets.

The key trade-off is discipline. If you issue cards too freely, you recreate the sprawl you were trying to fix. If you issue them with clear ownership and expiration logic, they become one of the cleanest ways to decentralize spending without decentralizing accountability.

Enhancing Security and Compliance by Design

Security is where virtual corporate cards are most misunderstood. Many teams think the value is "no plastic card." That's too shallow. The primary advantage is architectural.

Why the architecture matters

A virtual corporate card acts as a proxy that masks the underlying card number. Each one carries a unique 16-digit number, expiration date, and CVV, which means the merchant doesn't handle the static funding source itself. That's why merchant breaches don't automatically expose the underlying account in the same way they can with traditional card setups.

This matters more than many operators realize. A breach at a vendor isn't a theoretical issue. It's a recurring operating risk. If you follow incident reporting, resources like these ninja defenders breach details are useful reminders of how payment credentials and adjacent systems can become targets.

The practical implication is simple. If a card is single-use, merchant-locked, amount-capped, or short-dated, the stolen credential has very little residual value.

- Single-use controls cut off replay risk after the intended charge clears.

- Merchant locks stop cross-merchant misuse.

- Short expiration periods reduce the attack window.

- Instant freeze or closure gives finance a fast response path when a charge looks wrong.

Security improves when your payment credentials are disposable and purpose-built, not permanent and widely reused.

Compliance gets easier when controls are native

Compliance teams usually don't want more dashboards. They want fewer exceptions.

Virtual corporate cards help because policy can be embedded in issuance. If only approved merchants are allowed, if budgets are capped, and if card ownership is explicit, many policy breaches never occur. The audit trail improves as a side effect. Every card can map to a user, function, vendor, and approval event.

For web3 organizations, this is particularly useful. Treasury governance often focuses on wallet approvals, signer controls, and custody. But operational spend leaks through ordinary business tools. A compliant workflow needs both sides. Strong wallet governance for assets, and strong card controls for fiat spending.

The gap to watch is organizational behavior. No security model survives sloppy delegation. If teams share credentials in chat, leave recurring cards unowned, or skip review of dormant vendors, the system weakens quickly. The card architecture helps, but governance still has to be maintained.

An Implementation Plan for Modern Teams

Rolling out virtual corporate cards is less about issuing cards and more about redesigning how spend gets approved. Teams that skip that step usually end up with cleaner card numbers but the same messy process.

Start with policy before cards

Before anyone gets a card, define the categories of spend you want to support. Most companies can start with a short list: software, advertising, travel, contractor tools, infrastructure, and approved vendor services.

Then assign each category four things:

| Policy element | What to define |

|---|---|

| Owner | Who requests and who is accountable |

| Limit logic | Fixed amount, recurring budget, or case-by-case |

| Approval path | Manager, finance, or both |

| Expiry rule | Single-use, monthly, project end, or indefinite with review |

Many DAOs and global startups stumble. They assume decentralized operations require loose payment permissions. They don't. They require clearer payment permissions because entity structure, treasury source, and team geography are already complex.

Build approvals around exceptions

Don't force finance to approve every low-risk transaction manually. That scales badly and pushes teams back toward workarounds.

A better model is to pre-approve ordinary spend and route exceptions upward. For example:

- Known recurring vendors can run on recurring cards with owned budgets.

- New vendors may require finance review before the first card is created.

- Large or unusual purchases should trigger extra approval.

- Cross-functional spend should have one accountable budget owner, even if multiple teams benefit.

This creates a system where most normal operations move quickly, while riskier transactions get attention.

The strongest approval flow is the one people will actually follow under time pressure.

Connect cards to your ledger and treasury stack

If card transactions don't sync cleanly into your accounting process, you've just moved the mess downstream. The useful setup is cards tied to your chart of accounts, vendor records, entity structure, and close process.

In practice, that means:

- Map card activity to accounting software such as QuickBooks or Xero.

- Standardize expense metadata at issuance time, not weeks later.

- Separate entities and currencies clearly so intercompany confusion doesn't creep into routine spend.

- Define the treasury source for each payment path, especially if operating cash may originate from both fiat balances and converted digital assets.

For newly incorporated global entities and crypto-native teams, onboarding can also become a blocker. Traditional banking stacks often slow down on KYB when the company is new, offshore, or web3-linked. That's one reason some teams use providers built for those operating realities. OneSafe is one example. It offers business accounts, cards, global payments, and crypto-fiat workflows in one interface for companies operating internationally and in web3.

The implementation principle stays the same whichever provider you choose. Start narrow. Put a handful of high-friction spend categories onto virtual cards first. Review what breaks. Then expand with clearer policies, not more exceptions.

Analyzing the True Cost of Virtual Cards

Virtual corporate cards are often presented as if they automatically make payments cheaper. Sometimes they do. Often they don't. The answer depends on the payment type, merchant acceptance, settlement currency, and how often your team pays across borders.

Where the cost hides

For domestic software spend or controlled online purchasing, cards can be operationally efficient enough that the cost trade-off is acceptable. For high-FX vendor payments, the picture changes.

The issue isn't just card processing. It's the combination of card fees and currency conversion. For cross-border businesses, virtual card transactions can incur higher processing fees, including up to 3% FX on cards, compared with ACH or wire methods. That can materially affect margin on frequent international payments, especially for web3 firms, global SMEs, and offshore entities managing multiple currencies.

This is the question finance teams should ask before expanding card usage: is the card solving a control problem, a speed problem, or a treasury problem? If it's solving the first two while worsening the third without immediate notice, you need to know that early. Transparent fee schedules matter. A provider's published pricing and transfer fee structure is more useful than a generic promise of efficiency.

A practical comparison for an international payment

The right way to compare methods is not to pretend one rail wins every time. It's to compare visible and hidden costs side by side.

Cost Comparison: $1,000 USD Payment to EUR Vendor

| Metric | Virtual Corporate Card | SWIFT Wire Transfer |

|---|---|---|

| Speed to issue payment | Often faster for card-accepting vendors | Depends on banking path and vendor details |

| Spend controls | Strong. Limits, merchant controls, expiry | Weaker at payment instrument level |

| Reconciliation context | Often easier if linked to card program | Depends on bank memo quality and accounting workflow |

| Vendor acceptance | Only works if vendor accepts cards | Broad for international business payments |

| FX cost exposure | Can include card FX fees, with fees up to 3% in some cases | Can include bank FX spread and transfer fees |

| Best fit | Online spend, subscriptions, bounded vendor purchases | Larger vendor settlements, bank-to-bank payouts, vendors that don't take cards |

Two things tend to be true in practice.

- Cards are often better for control and speed.

- Wires are often better for direct settlement of larger international invoices, especially when card FX costs stack up.

The mistake is using a card solely because it's easy to issue. Finance should choose the rail that fits the transaction economics, not the one that feels modern.

Use Cases FAQ and Best Practices with OneSafe

Three common operating scenarios

A DAO needs to pay recurring infrastructure bills while keeping a clean approval trail between contributors and treasury signers. Virtual corporate cards work well when each service gets its own owner, budget cap, and renewal review date.

A global SME runs software, ads, and contractor tooling across several currencies. Cards help when each recurring platform has a dedicated credential instead of one shared card spread across teams.

A tech firm hires freelance developers worldwide. Cards are useful for tools, platforms, and services around those relationships, while direct contractor compensation may still belong on bank rails.

FAQ for global and web3 teams

Can virtual corporate cards be used in person?

Sometimes. Some virtual cards can be added to mobile wallets for tap-to-pay at merchants that accept them. The open question is narrower and more relevant for web3 teams: there still isn't clear industry guidance on how well these cards work with crypto-native merchants or for settling web3 invoices tied to non-custodial or crypto-heavy workflows.

Should we use cards for all cross-border payments?

No. Use them where control, approval logic, and merchant compatibility matter most. Be more selective where FX sensitivity is high.

How should teams set limits?

Tie limits to a known purpose, not to the seniority of the requester. A junior operator with a tightly scoped vendor card is lower risk than a senior employee holding a broad, reusable credential.

What should web3 finance teams pair with virtual cards?

A treasury process that connects fiat operations to digital asset balances cleanly. If you're also thinking through how to manage stablecoin treasuries, the key is to keep operational spend, conversion timing, and approval ownership in one coherent workflow.

What's the best practice for recurring spend?

One vendor, one card, one owner. Review dormant vendors regularly. Cancel cards when services end, not when accounting discovers the charge later.

If you're evaluating OneSafe, look at it the same way you'd evaluate any finance stack. Check whether the cards, multi-currency accounts, payment rails, and crypto-fiat workflows match your actual operating model. For global and web3 teams, the win isn't just having virtual corporate cards. It's having them inside a system that keeps control, treasury, and reconciliation connected.