If you're still paying vendors from a spreadsheet, approving wires in email, and reconciling card spend in a separate dashboard, the problem isn't just inefficiency. It's loss of control. Finance teams feel it when a supplier asks where the payment went, when a contractor in another country gets paid late because of cutoff times, or when treasury has to explain why FX costs were higher than expected.

That pain gets worse when the business operates across fiat and crypto at the same time. A typical AP tool can schedule a wire. A crypto wallet can move stablecoins. Neither one, on its own, gives operations and finance a clean system for running payroll, contractor payouts, treasury conversions, invoice settlement, and governance from one place. That's the gap many global startups, DAOs, and web3 companies are stuck in right now.

A modern payment automation platform fixes that by acting as a financial command center. It brings accounts, payment rails, approvals, cards, FX, and reconciliation into one operating layer. That shift isn't niche. The global AP automation market was valued at USD 5.7 billion in 2025 and is projected to reach USD 18.1 billion by 2034, with a 14% CAGR, according to Custom Market Insights research on the AP automation market.

Table of Contents

- An international SME paying people in multiple currencies

- A web3 treasury that has to operate in fiat and crypto

- Check the rails and workflows first

- Compliance can't be an afterthought

- Pricing discipline matters more than headline features

Moving Beyond Spreadsheets and Manual Wires

Friday afternoon, payroll is queued, three vendor payments are waiting on approval, and someone in treasury is checking whether the wallet transfer hit in time to fund a fiat wire. The work is spread across a bank portal, a spreadsheet, Slack, and an exchange account. Nothing is missing on purpose. The stack just was not built to run one controlled payment process across fiat and crypto.

That setup holds for a while. Then the company adds entities, hires contractors in new countries, pays software vendors in different currencies, or starts operating a web3 treasury that needs both onchain movement and off-ramping into fiat. At that point, manual work stops being an inconvenience and starts creating real financial risk.

Why manual workflows keep failing

Spreadsheets track status. They do not enforce policy, maintain approval chains, or create a reliable audit trail. Bank portals move money, but they rarely explain why a payment was made, who approved it, or how it should map back to the ledger.

The gaps get wider in cross-border operations. Teams end up managing cutoff times, beneficiary data, FX timing, and failed payment follow-up across several systems. For companies running international payouts, cross-border payment operations need one workflow with controls built in. Without that, every transfer depends on people remembering the process.

Web3 finance teams run into an extra layer of friction. Generic AP tools can route an invoice for approval, but they do not solve the handoff between wallet governance, stablecoin balances, exchange conversion, and fiat settlement. Treasury ends up reconciling screenshots, transaction hashes, exchange exports, and bank confirmations by hand. That is not modern finance infrastructure. It is a workaround.

Practical rule: If initiation, approval, funding, and reconciliation happen in different systems, the payment process is still manual.

What a payment automation platform changes

A payment automation platform centralizes how funds move through the business. Finance sets who can initiate payments, which approvals apply by amount or entity, what funding source is used, and how every transaction flows into reporting and reconciliation.

The operational gain is obvious. The strategic gain matters more.

In a unified setup, AP, treasury, and spend controls stop operating as separate disciplines. Finance can manage outgoing payments, incoming receipts, card activity, FX decisions, and treasury transfers from one operating layer. For a web2 business, that reduces delay and control gaps. For a web3 or DAO-linked treasury, it closes the gap between onchain assets and real-world obligations such as payroll, vendors, tax payments, and legal retainers.

A few changes usually show up first:

- Approvals become enforceable: Payment rules live in the system, not in inboxes or memory.

- Visibility improves: Finance can track pending, sent, failed, and completed payments without chasing updates across tools.

- Audit readiness gets better: Approvers, funding sources, invoices, and payment records stay connected.

- Treasury decisions improve: Teams can choose when to convert crypto to fiat, when to hold balances, and how to manage currency exposure with more control.

Finance teams are replacing manual payment processes because the old model breaks under scale, complexity, and governance pressure. That is even more true for companies operating across fiat and crypto, where disconnected tools create operational drag that ordinary AP software was never designed to fix.

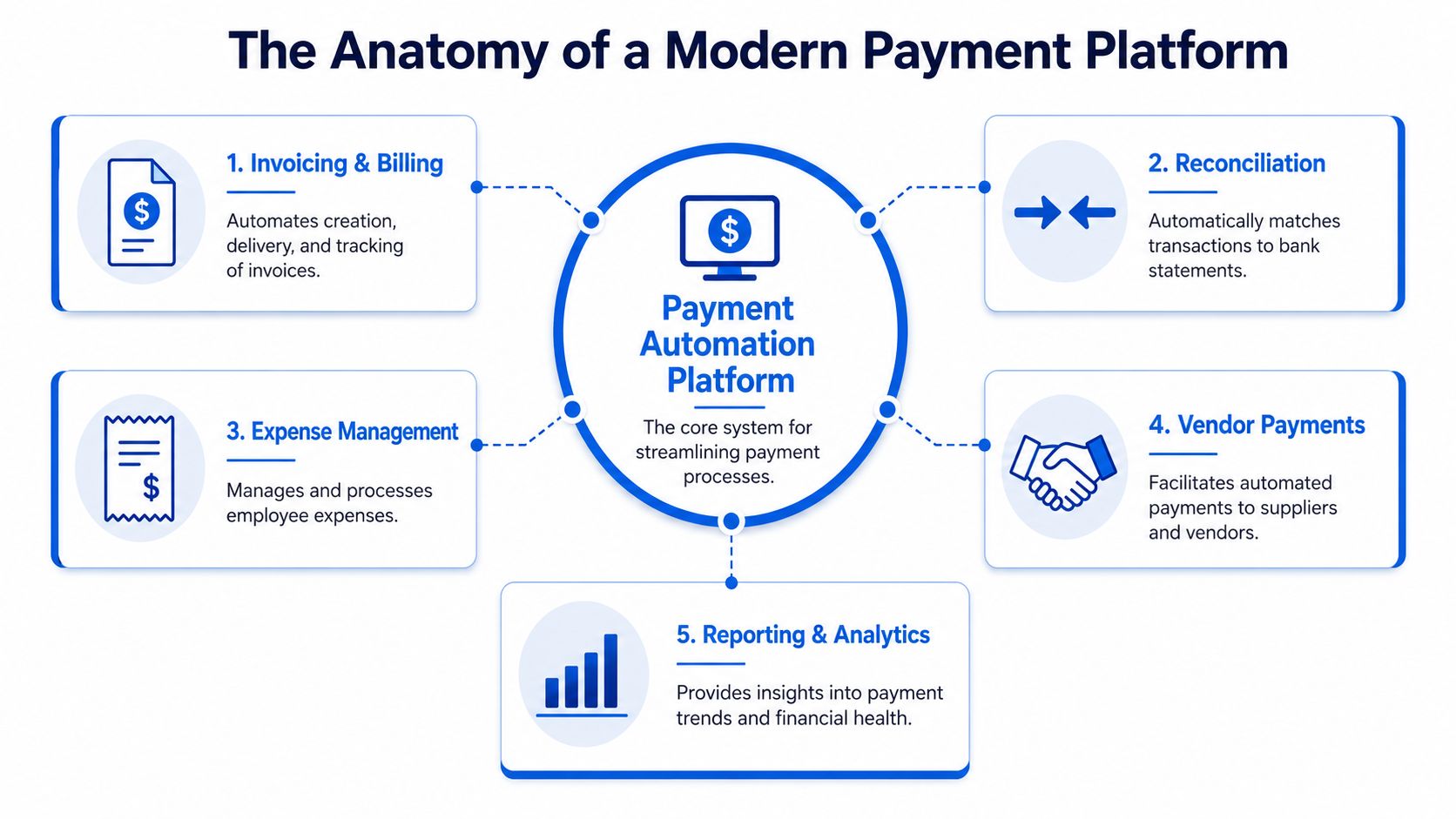

The Anatomy of a Modern Payment Platform

A strong payment automation platform looks less like a single feature and more like a financial operating system. The best way to evaluate it is to ask whether the pieces work together cleanly. If accounts, cards, FX, approvals, and reconciliation all exist but behave like separate products, finance still carries the integration burden.

One operating layer instead of disconnected tools

At the center is the account structure. Most companies need business accounts in multiple currencies, plus the ability to receive and send funds over the rails vendors and contractors use. That usually means some combination of ACH, domestic wire, international wire, and SWIFT, with card-based spend controls layered on top for software, travel, and recurring operational expenses.

Then there are the workflows around those rails:

| Component | What it should do in practice |

|---|---|

| Multi-currency accounts | Hold operating balances in the currencies the business uses most |

| Payment rails | Support local and international payout methods without forcing manual workarounds |

| Corporate cards | Give teams controlled spending power with limits and merchant policies |

| Approval engine | Route transactions by amount, entity, team, or vendor |

| Reconciliation layer | Match movement of funds back to invoices, expenses, and ledger entries |

A capable system also has to bridge edge cases that become normal at scale. A vendor may invoice in EUR while your treasury holds USD. A contractor may want a local transfer while procurement prefers card settlement for another category. A web3 team may receive USDC but need to pay legal counsel via wire. Good platforms make those flows routine instead of exceptional.

Why the architecture matters

Under the hood, modern systems are increasingly built with event-driven, cloud-native orchestration. That matters because payments aren't one step. They involve acceptance, execution, clearing, settlement, controls, and reporting. According to AWS guidance on real-time payment orchestration, this approach enables real-time processing of ACH, SWIFT, and crypto with sub-second latency and can reduce infrastructure costs by 40–60% compared with legacy systems.

That architecture has practical consequences for operators:

- Faster state updates: When a payment status changes, risk, reporting, and reconciliation can update quickly.

- Cleaner exception handling: Failed or held payments don't disappear into a manual review black hole.

- Modular upgrades: Teams can improve one workflow without rebuilding the whole stack.

- Better resilience: A single failure doesn't have to stop the full payment process.

The easiest way to spot an old platform is simple. It treats cards, bank transfers, and crypto as separate universes. Modern finance operations can't afford that split.

What works is consolidation with real controls. What doesn't work is buying one tool for AP, another for treasury, another for cards, and expecting finance to build the connective tissue manually.

Strategic Benefits of Payment Automation

The business case for a payment automation platform isn't just labor savings. The bigger payoff is operational discipline. Once payments move through one controlled layer, finance stops acting like an emergency response team and starts operating with policy.

What improves first

The first gain is efficiency, but not in the abstract. Teams stop rekeying vendor data, chasing approvals across messages, and reconciling from exported CSV files. That reduction in handoffs changes the daily rhythm of AP and treasury.

Control improves next. A payment system with defined roles, approval chains, spend limits, and method-specific permissions narrows the surface area for mistakes. If legal can approve counsel invoices, procurement can approve supplier terms, and finance can retain release authority, the process becomes both faster and safer.

For teams thinking more broadly about workflow design, this business process automation guide is useful because it frames automation as a control and coordination problem, not just a software purchase.

What finance leadership gains

For CFOs and heads of ops, the strategic benefit is visibility. When bank transfers, cards, and treasury conversions run through one system, you can see liquidity usage, upcoming obligations, and operating spend without waiting for manual consolidation.

That matters most in global structures. The moment a company opens in multiple markets or runs several entities, fragmentation starts to distort cash planning. A centralized setup for global treasury management gives finance a cleaner way to manage balances, approvals, and payment timing across jurisdictions.

A useful before-and-after comparison looks like this:

Before automation: Payments are possible, but controls are uneven and reporting is delayed.

After automation: Payments are policy-driven, easier to audit, and much easier to trace.

Before automation: Treasury reacts to cash movement after the fact.

After automation: Treasury can plan funding, conversions, and payouts inside one operating model.

Before automation: Teams add headcount to handle complexity.

After automation: Teams absorb growth with better systems and fewer manual checkpoints.

Operator note: The best outcome isn't that your team works harder with a nicer dashboard. It's that fewer payment decisions depend on memory, heroics, or side conversations.

Security also gets stronger when the platform supports MFA, asset segregation, and defined user roles. In crypto-inclusive environments, custody and governance have to sit alongside ordinary payment operations. If they don't, teams end up with secure wallets on one side and weak payment controls on the other. That's not modernization. That's fragmentation in a different form.

Payment Automation in Action Real World Use Cases

Theory is easy. The ultimate test is whether the platform removes friction from the exact payment paths your company uses every week.

An international SME paying people in multiple currencies

Take a services business with contractors in Europe, software vendors in the US, and suppliers elsewhere. In a manual setup, AP receives invoices by email, someone checks bank details in a spreadsheet, another person confirms FX availability, and finance pushes each transfer through the bank portal. Card spend sits somewhere else. Nobody sees the full picture until reconciliation.

A payment automation platform changes the workflow in a more practical way than most demos suggest. Contractor invoices can enter one queue, approvals can route by team or amount, and treasury can decide whether to pay from local balances or convert centrally. The finance lead can also track what has been approved but not yet funded.

What usually works well for this type of company:

- Centralized vendor records: Beneficiary details live in one place instead of several files.

- Method-based payment rules: Contractors get local transfers, larger suppliers get wires, recurring software spend goes to cards.

- Currency discipline: Finance chooses when to hold or convert funds, instead of converting in a rush on payment day.

What doesn't work is bolting automation onto an unchanged process. If the company still collects approvals in chat and only uses the platform as a release tool, most of the operational risk stays intact.

A web3 treasury that has to operate in fiat and crypto

Such scenarios often reveal the shortcomings of generic AP software. A web3 startup or DAO may receive treasury inflows in USDC, but its real-world obligations remain familiar. Payroll support vendors want fiat. Law firms want wires. Infra subscriptions hit cards. Tax, audit, and entity administration often require conventional banking rails.

According to Planergy's 2025 AP automation analysis, automation can reduce invoice processing costs by 78%, yet only 17% of current payment platforms support digital wallets. That gap matters because web3 teams often absorb 3%–5% FX and timing costs when they manually bridge crypto and fiat.

The practical problem isn't that crypto exists. It's that treasury and operations still sit in separate systems.

A better model looks like this:

- Treasury receives stablecoin inflows.

- Finance applies approval and policy rules before funds move.

- The platform converts crypto to fiat when needed.

- Payments go out over wire, ACH, SWIFT, or card from the same interface.

- Reporting captures the chain from source of funds to operational spend.

For teams building around digital asset operations, adjacent infrastructure matters too. If you're evaluating market plumbing or settlement environments tied to exchange activity, this overview of high performance crypto exchange development is a useful technical reference.

After the treasury side is stable, invoicing becomes the next pressure point. Web3 companies often need invoices that can settle in fiat or crypto without forcing the counterparty into a separate process. That's where web3 invoicing workflows become operationally important, not just convenient.

Here's a quick explainer that captures why orchestration matters:

The governance angle is just as important. DAOs and crypto-native teams need role-based controls that mirror how decisions are made internally. A platform that can move both fiat and crypto under one approval model reduces the chance that treasury decisions happen in one system while operating spend happens in another.

When fiat and crypto live in separate workflows, finance closes the books twice. Once for the bank side, once for the wallet side.

That split is exactly what many teams should eliminate.

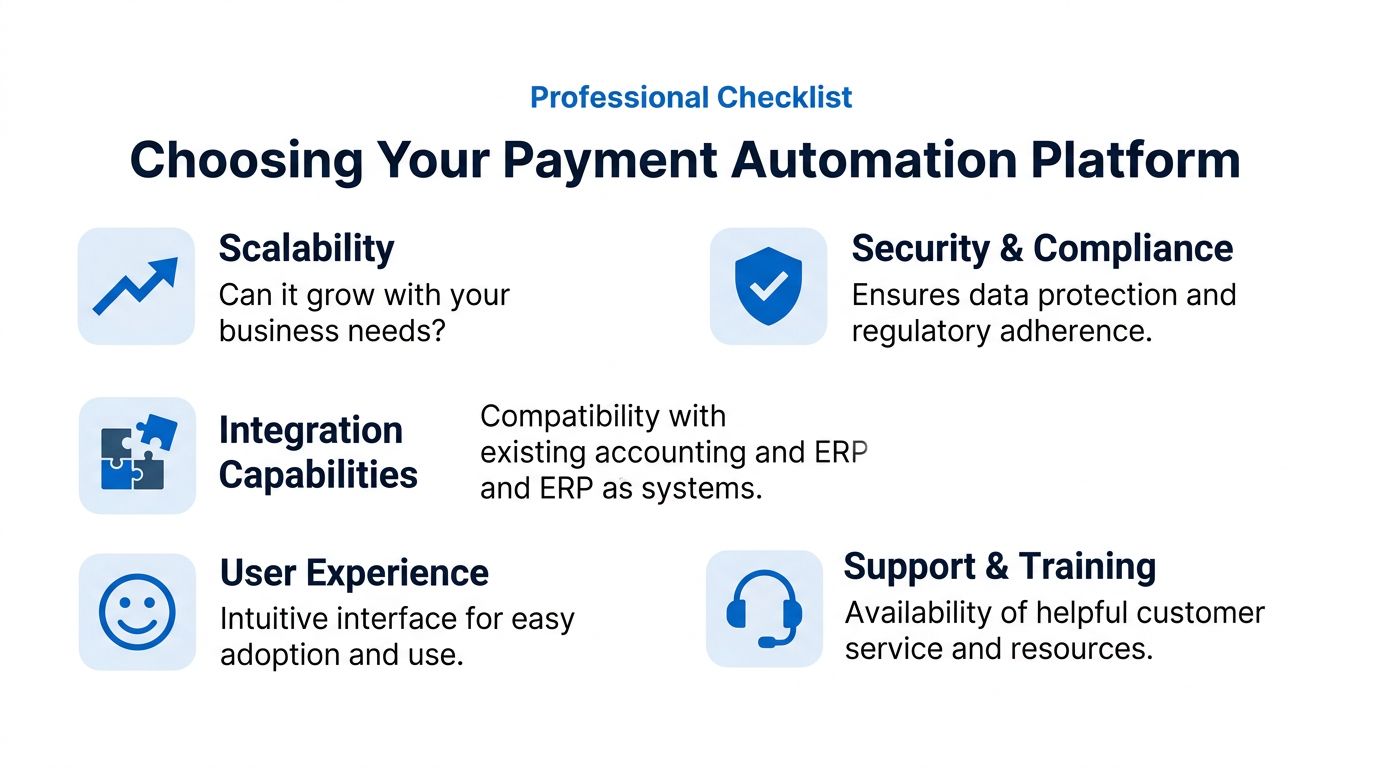

How to Choose the Right Payment Automation Platform

A lot of buyers choose a platform by feature count. That's usually a mistake. The better approach is to test how the system handles your actual payment paths, your approval structure, and your compliance constraints.

Check the rails and workflows first

Start with the obvious but often skipped question. Can the platform support the currencies, payment methods, and account structure your business uses today, plus the ones you're likely to add next? If your team pays contractors by local transfer, vendors by wire, and software via cards, all of that should sit inside one workflow.

Use this shortlist during evaluation:

- Required currencies: Make sure you can hold and settle in the currencies your business invoices and pays in.

- Payment coverage: Check ACH, domestic wire, international wire, SWIFT, cards, and crypto-related flows if they're relevant.

- Approval flexibility: Test whether rules can route by entity, amount, department, or vendor type.

- Accounting fit: Confirm the data exports and integrations won't create extra cleanup work downstream.

A smooth demo isn't enough. Ask the vendor to walk through a failed payment, a changed approver, a held transaction, and a beneficiary update. Those are the moments where weak systems expose themselves.

Compliance can't be an afterthought

Cross-border payments create exposure fast. If the platform can't adapt rules dynamically around restricted jurisdictions, sanctioned entities, or changing geographies, automation can amplify risk instead of reducing it.

That concern is more pressing because, as noted in the BillingPlatform 2025 AR automation survey, 39% of firms plan to add global payment method support, yet content in this area rarely explains how automated compliance checks should work in practice. For companies dealing with OFAC-sensitive restrictions, that omission matters.

Ask direct questions:

| Evaluation area | What to ask |

|---|---|

| Geo-fencing | Can the system block or restrict transactions by jurisdiction in real time? |

| Auditability | Are approvals, edits, and releases logged clearly enough for review? |

| Access controls | Can you separate preparers, approvers, and releasers by role? |

| Security | Are MFA and asset protection controls mandatory and visible? |

Red flag: If a vendor talks about compliance as a static onboarding task, they're not describing the operational reality of global payments.

Pricing discipline matters more than headline features

A platform can look efficient and still cost more than expected if pricing is opaque. FX markups, wire fees, card settlement costs, and spread leakage add up quickly when the business pays across currencies every week.

The right buying question isn't "what's the monthly subscription?" It's "what will a normal month of treasury conversions, contractor payouts, supplier wires, and card spend cost us?" If the answer is vague, finance should keep digging.

In crypto-inclusive setups, this matters even more. A tool that handles payments but forces manual conversion between digital assets and fiat may reintroduce timing risk and extra handling work. The surface feature looks modern. The operating model remains clumsy.

Your Implementation Roadmap and The OneSafe Advantage

Month one after rollout usually exposes the actual operating model. A supplier needs same-day payment in EUR, a contractor wants USDC, payroll still runs in fiat, and three people are stuck in separate tools trying to confirm who approved what. The implementation plan has to solve that coordination problem, not just replace one dashboard with another.

Start with process mapping, but keep it practical. Track how payments are requested, approved, funded, converted, and reconciled across fiat accounts, cards, wallets, and accounting systems. In web3 and DAO environments, add one more layer. Document who controls treasury decisions, how signer authority works, when assets move from crypto to fiat, and where governance slows routine payouts.

Then set policy before migration. Define approval thresholds, role separation, wallet and banking permissions, card controls, and rules for treasury conversion. At this juncture, many teams either reduce risk or recreate the same chaos inside a new tool. If crypto-to-fiat conversion still sits outside the payment workflow, finance keeps carrying timing risk, manual handoffs, and avoidable reconciliation work.

Roll out in phases. Start with a controlled payment lane such as contractor payouts or vendor bills, confirm the approval path works under normal and exception cases, then expand to treasury conversions, employee spend, and higher-volume disbursements. Teams that try to move everything at once usually discover policy gaps too late.

For companies that need multi-currency accounts, ACH, wires, SWIFT, cards, crypto-compatible treasury workflows, and policy controls in one environment, OneSafe is one example of a platform built for that operating model. It brings fiat and crypto payment activity into one interface, supports team-based governance, and gives finance clearer control over conversion and payout workflows. That matters for global startups and DAO-linked teams that have outgrown generic AP software built around fiat-only assumptions.

If the current stack still depends on bank portals, wallet tools, spreadsheets, and Slack approvals, the next step is to consolidate the workflow and tighten control. OneSafe gives finance and operations teams a practical way to run payments, treasury, cards, and crypto-to-fiat activity from one system.