A lot of finance teams are stuck in the same loop. Employees put travel, software, and vendor purchases on personal cards. Contractors wait on wires. Accounting exports statements, chases receipts in Slack, and tries to reconstruct what each charge was for after the month has already moved on.

That setup breaks faster when the company is global. It breaks even faster when treasury sits partly in fiat and partly in crypto. A SaaS bill hits in USD, a contractor wants EUR, the treasury holds USDC, and nobody wants another spreadsheet that tries to bridge all of that manually.

The market is moving in a clear direction. The global expense card market reached USD 37.7 billion in 2025 and is forecast to grow at a CAGR of 10.3%, hitting USD 82.6 billion by 2034, driven by demand for real-time spend controls and multi-currency capabilities for companies operating across borders and in web3, according to Growth Market Reports on the expense card market.

Table of Contents

- Introduction Why Expense Management Is Broken for Modern Companies

- The card is only one part of the system

- Why this changes finance operations

- How do FX fees on expense cards actually work

- Can a newly incorporated offshore entity get a business expense card

- How can a DAO use expense cards for contributor payments

- What should I look for in provider pricing beyond the monthly plan

Introduction Why Expense Management Is Broken for Modern Companies

Finance leaders usually notice the problem before anyone else. Cash leaves the business in small, messy ways. Team leads buy subscriptions without procurement context. Employees submit reimbursements late. Month-end becomes a cleanup exercise instead of a reporting process.

For a distributed startup, the friction multiplies. A developer in Portugal pays for a tool in EUR. A founder in Singapore books travel in SGD. A US entity settles software in USD. If the business still runs on personal cards plus reimbursement, finance loses visibility at the exact moment it needs control.

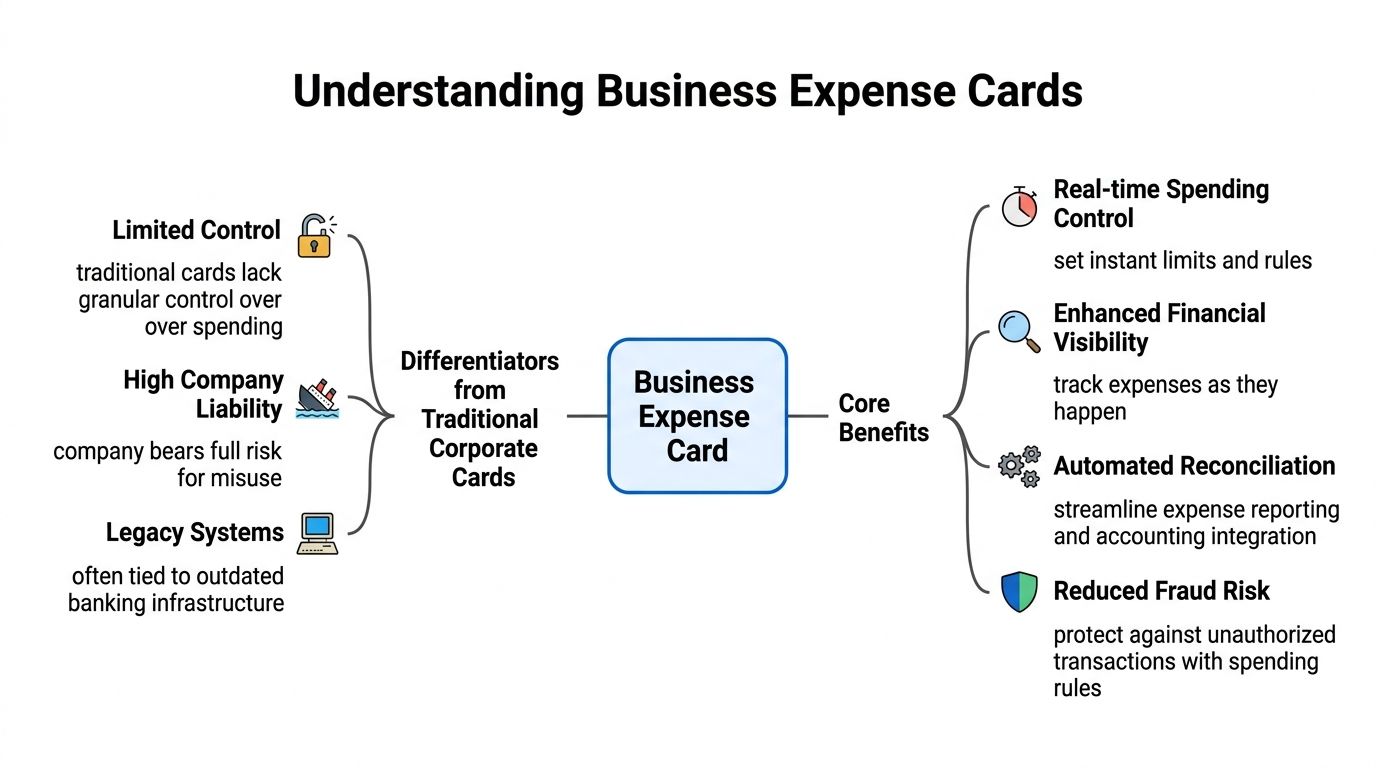

That's why a modern business expense card matters. It isn't just a nicer company card. It's a control layer for spend that sits inside the operating system of finance. It gives the Head of Finance a way to decide who can spend, where they can spend, and how transactions land in the books.

Practical rule: If your team learns about spend after the statement closes, you don't have spend control. You have spend reporting.

The companies getting this right are treating card infrastructure as part of treasury, accounting, and policy enforcement. That's especially important for firms with cross-border operations and web3 exposure, where card transactions often intersect with foreign exchange, entity structure, and treasury conversion decisions.

Three patterns usually signal it's time to change the model:

- Out-of-pocket spending is common: Employees are effectively lending money to the company.

- Approvals happen in chat: Policy exists, but enforcement depends on someone being online.

- Reconciliation is delayed: Accounting sees transactions in batches instead of in context.

When those problems show up together, a business expense card stops being a nice-to-have. It becomes finance infrastructure.

What Exactly Is a Business Expense Card

A business expense card is a company-issued payment card, physical or virtual, tied to software that applies spend policy at the point of purchase and sends transaction data into the finance stack. Mastercard explains that virtual and commercial card programs can be configured with controls for merchant type, spend limits, and usage rules, which is the key distinction from a basic card with after-the-fact review in its overview of virtual cards for business payments.

The card is only one part of the system

The card matters less than the control layer behind it.

In practice, a modern expense card program combines card issuance, policy rules, receipt collection, approval logic, and accounting sync. Employees see a card in Apple Pay or a plastic card in their wallet. Finance sees a governed payment rail with user-level permissions, audit trails, and transaction metadata that can be mapped into ERP and expense tools.

That architecture matters more for global and crypto-native companies than many finance guides admit. If a team operates across entities, currencies, and contractors, a card transaction is rarely just a card transaction. It can affect VAT handling, subsidiary allocation, treasury planning, and, in some cases, the timing of fiat conversion from digital assets.

The software typically checks rules such as:

- Merchant category: whether the card can be used for travel, software, ads, or other approved categories

- Transaction amount: whether the purchase stays within a set limit

- Geography: whether usage is allowed in specific countries or regions

- Time or duration: whether the card works only during a project window or approved travel period

- User or team permissions: whether the cardholder is approved for that spend type

If a transaction falls outside policy, it can be declined or routed for review before it becomes a reconciliation problem.

Why this changes finance operations

The operational gain is straightforward. Finance spends less time cleaning up exceptions because fewer exceptions get through in the first place.

That shift matters once spend becomes distributed. SaaS subscriptions get bought by function leads. Travel happens across time zones. Agencies and contractors need controlled purchasing access. Web3 teams may also need cards for fiat operating spend while treasury sits partly in stablecoins or other digital assets. In that setup, the expense card works as a policy enforcement tool between treasury and day-to-day spending.

A well-designed program changes the workflow:

| Old model problem | What a business expense card changes |

|---|---|

| Missing receipts | Receipt prompts happen close to the transaction |

| Policy violations | Rules block or flag spend at authorization |

| Slow coding to GL | Transaction data can sync into accounting systems |

| Shared card misuse | Named cardholders and virtual cards create accountability |

For a Head of Finance, that is its fundamental definition. A business expense card is not just a payment method. It is a spend control system that uses card rails to enforce policy, capture context, and keep distributed teams moving without giving up governance.

The Main Types of Business Expense Cards

Teams typically don't need one card type. They need a mix. The right setup depends on whether the spend is recurring, travel-heavy, temporary, or online-only.

Corporate expense cards

These are the cards commonly envisioned first. They're assigned to employees or team leads for ongoing operational spend such as travel, client meals, software purchases, or recurring departmental expenses.

They work best when the employee needs repeat access and the finance team wants central oversight without issuing ad hoc approvals for every purchase.

Good fit:

- Frequent travelers

- Department heads

- Ops or procurement staff

Watch-out: if you issue these too broadly without strong controls, you recreate the same governance issues as a legacy corporate card program.

Prepaid expense cards

Prepaid cards are useful when finance wants to cap exposure tightly. They're effective for project budgets, contractor use cases, event spending, and temporary workers where the company wants a fixed spend envelope.

This model works well when the budget is known in advance. If a field team needs a defined amount for a short activation, prepaid is often cleaner than opening a more flexible line.

Best use cases include:

- Event budgets

- Short-term project allocations

- Controlled contractor purchases

Trade-off: prepaid can be too rigid for teams with variable spend, especially if budgets need frequent adjustments.

Virtual expense cards

Virtual cards are the sharpest tool for online spend. They're ideal for SaaS subscriptions, digital ads, one-time vendor purchases, and secure online procurement.

The strongest use case is vendor-level isolation. A unique card per subscription makes it far easier to track renewals, cancel services, and contain fraud exposure if a card number is compromised.

Here's the practical comparison:

| Card Type | Funding Model | Best For | Key Benefit |

|---|---|---|---|

| Corporate expense card | Company-funded operating spend | Employees with recurring business purchases | Ongoing flexibility with policy controls |

| Prepaid expense card | Preloaded company funds | Fixed budgets, projects, temporary teams | Hard cap on spend exposure |

| Virtual expense card | Company-funded digital issuance | SaaS, ads, online vendors, one-time payments | Strong security and vendor-level control |

A strong program usually pairs physical cards for travel and in-person spend with virtual cards for online vendors. That split keeps the policy simple. It also makes auditing much easier because each spend type has a cleaner trail.

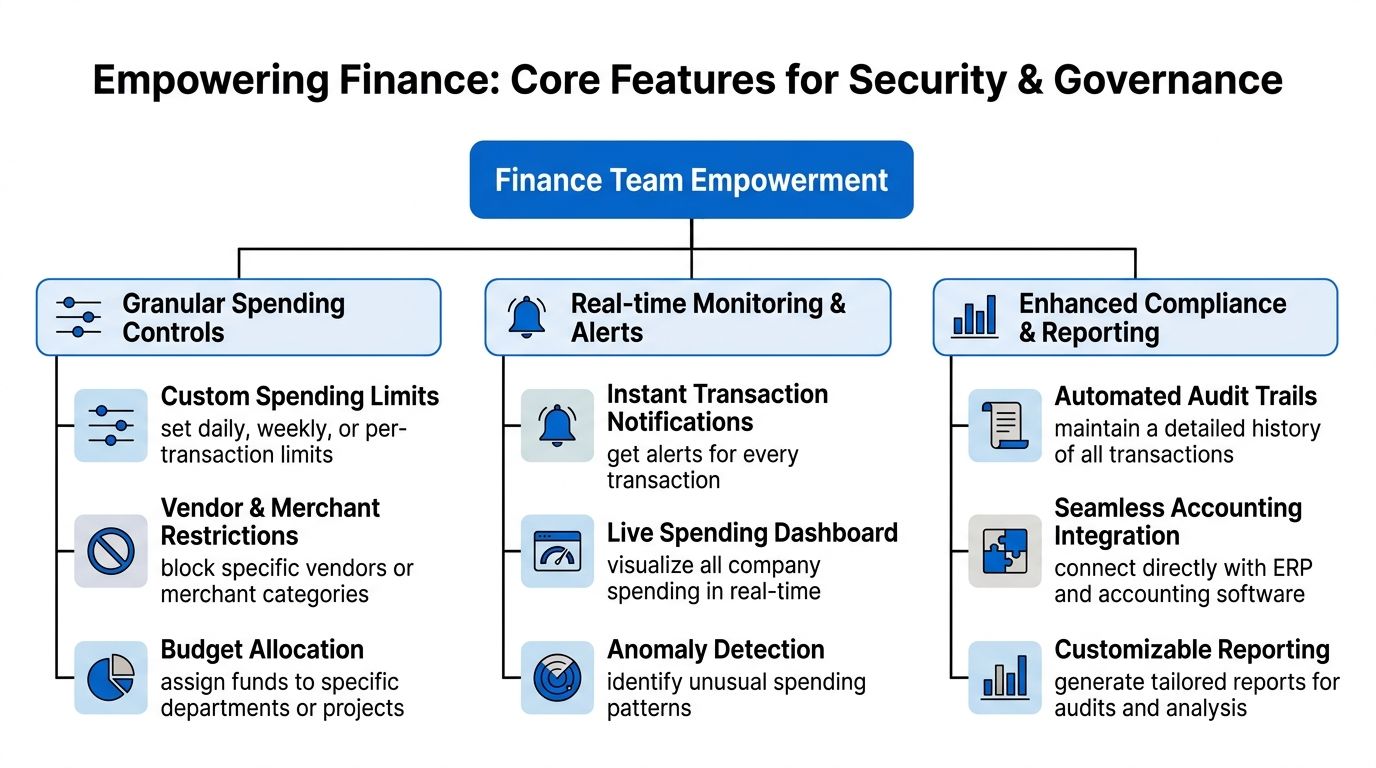

Core Features for Security and Governance

The difference between a useful card program and a chaotic one is configuration. Most providers can issue cards. Fewer can give finance real governance without making the employee experience miserable.

Controls that matter in practice

The first layer is spending control. Not broad limits. Specific, enforceable rules.

The controls worth prioritizing are:

- Per-transaction and periodic limits: Set caps by purchase, day, week, or month.

- Merchant category restrictions: Allow approved business categories and block obvious out-of-policy spend.

- Approval workflows: Route larger or unusual transactions to a manager or finance approver before funds are used.

- Card-level permissions: Give marketing, travel, and procurement different rule sets instead of using one generic policy.

If you're designing internal controls, it also helps to borrow ideas from mainstream fraud prevention workflows. Teams that want a broader checklist beyond card settings can review this guide on preventing credit card fraud, especially for practical controls around monitoring and misuse response.

A modern card stack should also support:

- Instant card freezing

- Real-time transaction notifications

- Audit-ready transaction history

- Direct integration with the provider's card controls interface, such as corporate cards and spend controls

Governance only works if the workflow is usable

A lot of programs fail because policy is technically strong but operationally clumsy. Employees get blocked on legitimate purchases. Receipts are requested too late. Finance creates workarounds that bypass the system.

What works better is a combination of strict defaults and targeted flexibility.

The best approval workflow is the one employees rarely notice because the right purchases go through cleanly and the wrong ones stop immediately.

A good operating model usually includes:

| Feature | Why finance cares | Why employees care |

|---|---|---|

| Real-time alerts | Faster exception review | Fewer mystery declines |

| Receipt capture on mobile | Better documentation | Less month-end admin |

| ERP or accounting sync | Cleaner books | Fewer follow-up requests |

| Role-based access | Better segregation of duties | Clearer spending authority |

Security isn't just about fraud. It's about governance, tax support, and clean evidence during audits. If the card platform can't show who spent, what policy applied, what documentation was attached, and where the transaction landed in accounting, the finance team still ends up doing detective work.

Integrating Cards with Global Financial Workflows

A card program works best when finance can trace a purchase from the moment it happens to the final ledger entry. For a startup running across entities, currencies, and remote teams, that is the difference between controlled spend and a month-end cleanup project.

The first test is basic but revealing. Card data should flow into QuickBooks, NetSuite, or Xero with the merchant, amount, currency, receipt, employee, and entity context intact. If the process still depends on CSV exports and manual recoding, finance has not solved the workflow. It has only moved it.

Good integration improves day-to-day operations in a few concrete ways:

- Transactions reach the ledger faster

- Receipts and supporting documentation stay tied to the spend

- Category coding stays more consistent across teams

- Entity-level reporting is easier to maintain

- Audit review takes less reconstruction

For global companies, card infrastructure also needs to match how cash is held. A provider may offer decent spend controls but still create friction if cards sit outside the company's banking and treasury setup. Teams operating across regions usually get better control when card issuance is connected to multi-currency business accounts for global companies, rather than bolted onto a separate platform.

That matters even more for crypto-native businesses.

A web3 finance team might hold treasury in stablecoins, keep fiat operating balances in several currencies, and pay vendors, travel, and SaaS expenses by card. If cards are isolated from the rest of that stack, every funding cycle adds avoidable work. Treasury converts funds, moves them into a bank account, waits for settlement, then allocates spend back to the right entity and currency. The card program functions, but the workflow stays fragmented.

Multi-currency card design reduces a lot of that friction. Stripe's guide to business expense cards in Germany and cross-border usage notes that international card programs benefit from the ability to hold and spend in local currencies instead of forcing every transaction through one base currency.

The practical gain is clearer cost control. If a company funds EUR card spend from a EUR balance, finance sees the actual local cost without layering in unnecessary conversions. The same applies to GBP software spend, CAD operating costs, or regional budgets managed by local team leads.

A workable setup usually follows four rules:

- Hold operating funds in the currencies the business uses

- Issue cards with the right entity and currency alignment

- Push transaction data into accounting with merchant, receipt, and coding details attached

- Review exceptions centrally, instead of fixing classification after close

This approach is less exciting than card rewards. It is far more useful if the goal is cleaner books, lower FX leakage, and tighter control across a distributed company.

Why Traditional Cards Fail Web3 and Global Businesses

Legacy card products were built for fiat-only companies with straightforward banking rails. That model doesn't hold up when treasury, payouts, and vendor payments move across currencies and, in many cases, across fiat and digital assets.

The gap is no longer niche. Brex notes that over 60% of Web3 startups face compliance and FX friction with traditional cards because they lack native crypto-to-fiat switching and multi-currency settlement support in its discussion of business expense cards and the crypto-native gap.

The fiat-only workflow creates operational drag

Here's what usually happens in practice. Treasury holds stablecoins. The company needs to pay for software, flights, legal fees, or contractor tools with a card. Finance converts funds externally, moves them into a bank account, waits for settlement, and then funds card spend separately.

That creates multiple problems at once:

- Treasury fragmentation: fiat sits in one system, crypto in another, cards in a third

- Approval friction: spend policies don't map neatly to treasury movements

- FX exposure: conversion timing can change the actual cost of operating spend

- Reconciliation pain: accounting has to connect on-chain movement to off-chain card usage

DAOs and web3 teams feel this more sharply because operations don't always fit the assumptions of a traditional bank card program. Contributor payments, protocol-related expenses, and mixed fiat-crypto vendor relationships require tighter workflow design.

Some teams even build internal monitoring around their vendor ecosystem and treasury events using tools such as a web scraping api to collect payment, pricing, or vendor data from external systems. That helps, but it still doesn't solve the core issue if the card product itself can't bridge treasury and spend.

What modern teams actually need

The missing capability is unified settlement logic. A global or crypto-native company needs card infrastructure that fits the way money moves inside the business.

That usually means:

- Multi-currency balances for local operating spend

- Near-instant switching between treasury sources and card funding

- Controls that apply across teams, vendors, and geographies

- Clear support for crypto-related business flows, including crypto business payments for web3 operations

If treasury can move quickly but spend controls can't, finance still becomes the bottleneck.

Many generic guides often fall short. They explain cards as a reimbursement upgrade. For web3 companies, that's incomplete. A key challenge is stitching together treasury conversion, card authorization, vendor settlement, and accounting evidence in one workable operating flow.

A short product walkthrough helps make that workflow more concrete:

Traditional cards aren't useless. They're just built for a narrower operating model. Once a company becomes international, entity-heavy, or crypto-adjacent, the old assumptions start causing friction in places finance can least afford it.

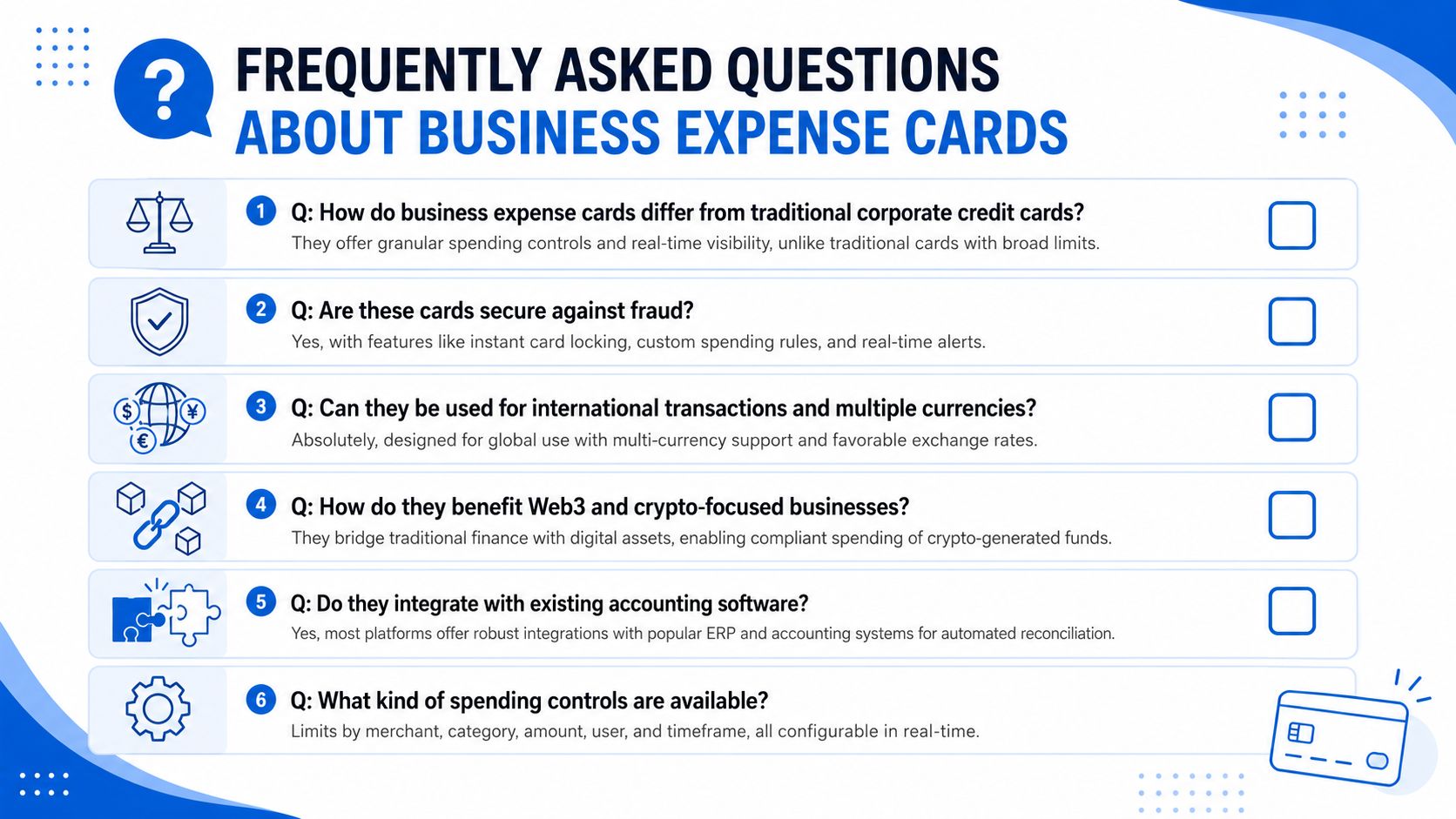

Frequently Asked Questions About Business Expense Cards

The questions below usually come up once a finance team moves from “we need better cards” to “we need the right operating model.”

How do FX fees on expense cards actually work

There are usually two cost layers. First, the conversion spread or FX fee itself. Second, the operational cost of converting at the wrong moment because the card settles from a currency you didn't intend to use.

That's why local currency balances matter. If the team spends in the same currency the business already holds, finance avoids unnecessary conversions and gets cleaner cost attribution.

Can a newly incorporated offshore entity get a business expense card

Sometimes yes, but the practical answer depends on the provider's onboarding appetite, jurisdictions supported, and KYB requirements. Newly formed BVI, Cayman Islands, or Panama entities often struggle when providers want long operating history, domestic directors, or a conventional business model.

The better question to ask is not “do you issue cards” but “what entity types do you underwrite, and what documents do you need for approval and ongoing compliance?”

How can a DAO use expense cards for contributor payments

Most DAOs shouldn't start by giving broad card access to many contributors. The cleaner model is to designate an operational entity or controlled treasury function, issue cards only where ongoing spend is necessary, and keep contributor compensation on a separate payment workflow.

Cards work well for:

- Software subscriptions

- Travel for approved representatives

- Event and community operations

- Vendor purchases with clear policy ownership

They work poorly when the DAO is trying to use a card program as a substitute for contributor payroll, grants administration, or unmanaged treasury disbursement.

What should I look for in provider pricing beyond the monthly plan

Ignore the headline subscription first. Look at the full movement of money.

Review:

- Card FX charges

- Wire and SWIFT fees

- Fiat deposit and withdrawal costs

- Physical card issuance or replacement fees

- Failed payment or exception handling fees

- Whether the provider publishes pricing clearly

If your treasury includes stablecoins, it also helps to monitor the asset you'll likely convert from or receive. For teams handling PayPal USD, Current PYUSD market data can be a useful reference point during treasury planning.

A final note on tax and compliance. In markets such as Germany and the broader EU, companies need strict separation between business and personal expenses to preserve deductibility and reduce liability. That's one reason modern card controls matter so much operationally, not just administratively.

Choose the provider whose workflow matches your business model, not the one with the loudest card marketing. For global and web3 finance teams, the edge comes from settlement design, policy control, and reconciliation quality.

If your team needs business cards, multi-currency accounts, and crypto-compatible payment workflows in one place, OneSafe is built for that operating model. It gives global and web3 companies a way to manage spend, treasury movement, and cross-border payments without stitching together separate systems.