You're probably here because a bank, accountant, vendor, exchange, or client told you to “send a SWIFT transfer,” and the phrase sounds more technical than it should. You need to move money across borders, but the practical questions are simple. How does it work, how long will it take, why does the received amount sometimes shrink, and what can you do about it?

For modern businesses, especially startups and web3 companies managing vendors, contractors, treasury, or exchange flows across countries, SWIFT still matters. But most explanations stop at “it's an international wire.” That's not enough. If you don't understand that SWIFT is a messaging system, not the money movement itself, the fees, delays, and tracking gaps all seem random.

Table of Contents

- The process starts with an instruction

- Correspondent banks handle the route

- A payment can pass through more institutions than you see

- Where delays and surprises usually happen

What Is a SWIFT Transfer Really

A SWIFT transfer is best understood as a secure message between banks. Think of SWIFT like a highly secure global postal service for financial institutions. It delivers the instruction to move money. It doesn't carry the money itself.

That distinction is more significant than widely recognized. When your bank says it has “sent the SWIFT,” what it has usually sent is the payment instruction to another bank. The actual funds are then settled through banking relationships behind the scenes.

According to Wikipedia's overview of SWIFT, SWIFT connects over 11,000 financial institutions across more than 200 countries and territories, and in 2020 it processed around 35 million messages daily. The same source also notes that SWIFT does not transfer physical money itself. It transmits payment instructions, while settlement happens through correspondent banking relationships.

Why people get confused

Most businesses experience SWIFT through the user interface of a bank portal. You enter recipient details, pick a currency, approve the payment, and see a status that says “wire sent.” That makes it feel like one direct action.

In reality, there are two layers:

- The message layer. SWIFT sends standardized instructions between institutions.

- The settlement layer. Banks adjust balances through their own cross-border banking relationships.

Practical rule: If you remember only one thing, remember this. SWIFT is a communication network, not a bank account and not the settlement itself.

Why SWIFT still matters

Even with newer payment options, SWIFT remains part of the plumbing of global commerce. Businesses use it because banks around the world already know how to receive and process these messages, and because it supports a very broad range of payment corridors and currencies.

If you're asking “what is SWIFT transfer” in plain English, the shortest accurate answer is this: it's a bank-to-bank instruction system for international payments.

That's also why a SWIFT payment can feel both familiar and frustrating. The message standard is global. The actual path the money takes is not. That path depends on which banks know each other, which currencies are involved, and whether intermediary institutions need to step in.

How SWIFT Payments Actually Work Step by Step

A finance lead approves a supplier payment on Monday morning and expects the funds to arrive like an email. By Wednesday, the supplier is still asking where the money is. The reason is usually simple. A SWIFT payment is a coordinated handoff between several banks, and each handoff can add time, checks, fees, or FX costs.

The process starts with an instruction

SWIFT works like a secure postal service for banks. The sender's bank creates a standardized message, often an MT103 for a customer payment, and sends it to the bank network. That message says who should be paid, in what currency, and through which institutions the payment should move.

In practical terms, the flow looks like this:

You submit the payment order.

Your bank collects the beneficiary name, account number or IBAN, SWIFT/BIC code, currency, amount, and payment purpose.The sending bank reviews the payment.

It checks balances, sanctions screening, formatting, and internal approval rules.The bank sends the SWIFT message.

The message moves quickly. The money still needs to be settled through banking relationships in the background.

Before going further, this short video gives a useful visual overview of the process.

Correspondent banks handle the route

If the sending bank cannot pay the receiving bank directly in the required currency, one or more correspondent banks step in. This is common in cross-border USD payments and in less direct currency corridors.

The core idea is simple. Banks keep accounts with each other so they can settle obligations without opening a direct branch in every country.

That is where Nostro and Vostro accounts appear:

- Nostro account means “our money held with your bank”

- Vostro account means “your money held with our bank”

Those terms sound technical, but they describe a ledger relationship. One bank holds funds with another bank, then uses those balances to complete cross-border payments.

A payment can pass through more institutions than you see

Take a UK company paying a supplier in Singapore in US dollars.

The UK company sends the instruction to its bank. The bank creates the SWIFT payment message. If that bank does not have a direct USD relationship with the supplier's bank, the payment may pass through a US correspondent bank, or more than one. Each bank in the chain may screen the transaction, deduct a fee, and process the settlement on its own timetable before the supplier's bank credits the final account.

This hidden route matters for cost. Your outgoing wire fee is only the visible part. Intermediary charges, receiving bank fees, and FX spreads can all sit underneath the surface, which is why many finance teams compare traditional wire transfer fees against crypto payment costs before choosing a rail.

Where delays and surprises usually happen

A SWIFT transfer rarely stalls because the message failed to send. Delays usually happen at one of four points: compliance review, correspondent routing, currency conversion, or beneficiary bank processing.

For a modern business, especially a web3 company paying contractors, exchanges, or global vendors, that distinction matters. The message layer may be fast, but the settlement route can still be slow and expensive. Legacy SWIFT flows often leave senders with limited visibility until the payment lands or gets queried. SWIFT GPI improves that experience by giving participating banks better tracking and clearer status updates, but the route still depends on the banks involved.

The useful takeaway is practical. A SWIFT payment behaves less like a direct bank-to-bank push and more like a package moving through multiple logistics hubs. You can send it quickly. The final arrival time and total cost depend on the route.

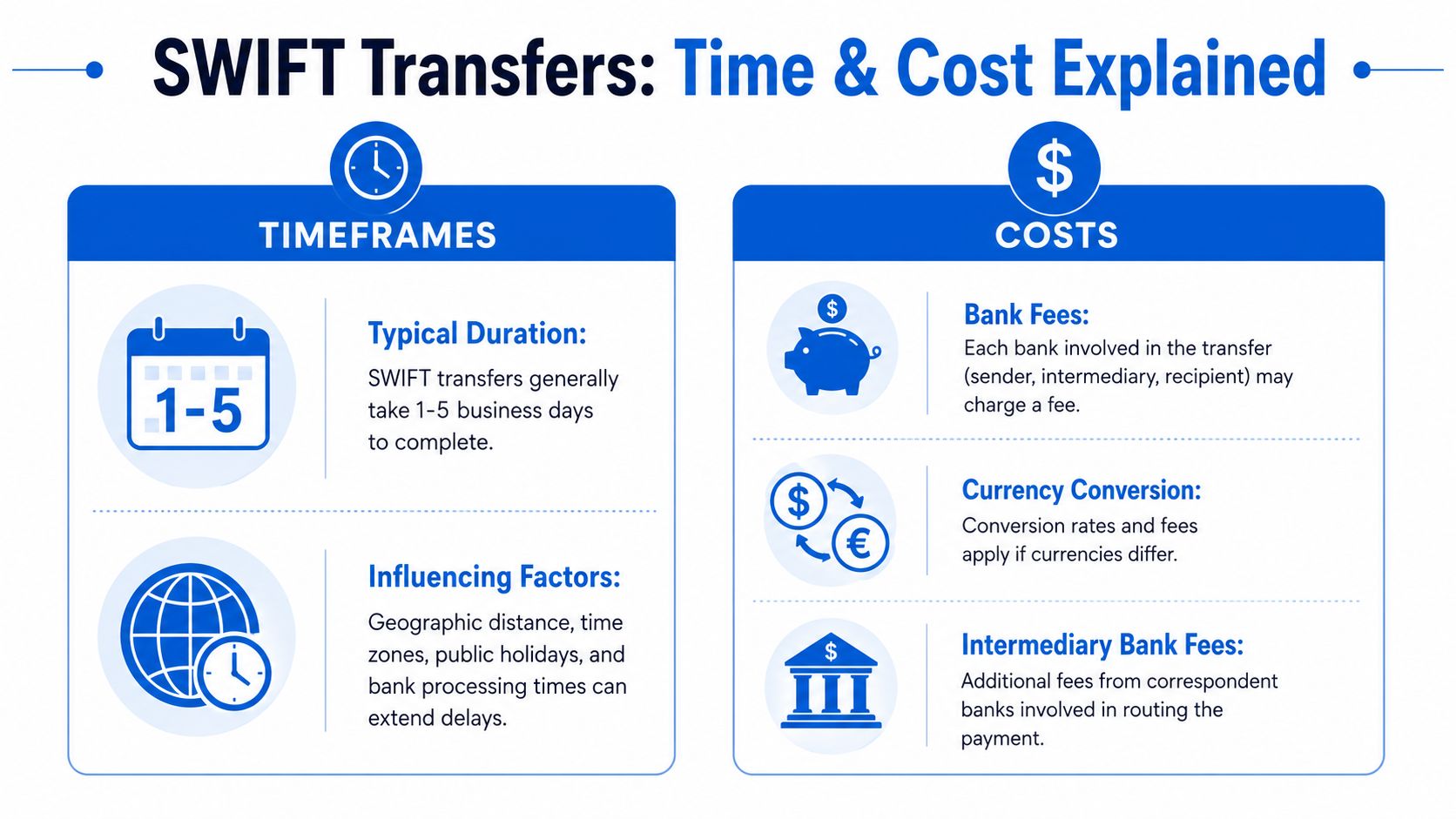

Decoding SWIFT Transfer Timeframes and Costs

A finance lead approves an international payment on Tuesday morning and sees the status change to “sent” a few minutes later. The supplier still has nothing by Thursday, and the amount that finally lands is lower than the invoice. That gap between what the sender sees and what the recipient gets is the part of SWIFT many guides skip.

A SWIFT transfer message can move quickly, but the money still has to pass through the banking route behind it. For a straightforward corridor between banks with a direct relationship, the payment may arrive within a couple of business days. Add one or two correspondent banks, a currency conversion, or a compliance review, and the timeline often stretches to several business days.

That difference matters for operations. If you are paying a contractor, topping up an exchange account, or settling an invoice tied to a shipment release, “usually fast” is not the same as “arrives on time.”

Why timing varies in real life

Transfer time depends less on the SWIFT message itself and more on the route the funds take after the instruction is sent. SWIFT works like a secure postal system for banks. The message is the letter. Settlement is the package changing hands across a chain of carriers.

A payment often slows down for a few practical reasons:

- Intermediary banks add extra stops and their own processing queues

- Cut-off times push instructions to the next banking day

- Time zone gaps shorten the overlap between banks

- Currency conversion may happen at an intermediary or receiving bank

- Compliance screening can trigger manual review

- Local bank holidays pause processing even if your bank is open

This also helps explain the gap between legacy SWIFT and SWIFT GPI. Legacy flows often feel opaque because the sender sees the instruction leave but gets little visibility after that. SWIFT GPI improves tracking and status updates among participating banks, and many payments move faster under that standard. It does not remove every delay. If the route includes extra banks or manual checks, the payment can still take time.

The hidden cost stack

The outgoing wire fee is only the visible layer. The full cost usually includes the sending bank fee, one or more intermediary deductions, a receiving bank fee in some corridors, and the exchange rate spread applied during conversion.

Razorpay's breakdown of SWIFT fees shows the pattern clearly:

- Sender fee: typically $25 to $50

- Intermediary bank fees: typically $10 to $50 per hop

- FX markup: often 2% to 3%

The same source notes that on a $10,000 transfer involving two intermediary banks, the total cost can exceed $150 (1.5%).

For a business, the FX spread is often the easiest cost to miss. A bank may quote a transfer fee that looks reasonable, then recover more margin inside the exchange rate. On small payments, that can be annoying. On recurring treasury flows, it becomes a budgeting problem.

If the recipient gets less than expected, the shortfall often comes from deductions and FX spread applied somewhere along the route.

A business example

Suppose a web3 company sends USD to pay overseas counsel, a market maker, or a contractor who invoices in another currency. The treasury team budgets for the wire fee shown on the bank screen. The payment then passes through two correspondent banks, picks up deductions along the way, and converts at a weaker rate than expected. The vendor receives less, accounts payable has to reconcile the gap, and the team may need to send a second payment just to close the invoice.

That is why many operators compare the full economics of rails, not just the headline bank fee. This review of Bank of America wire transfer fees compared with crypto payment costs is useful because it highlights how visible fees and actual delivered cost can differ.

For modern businesses, especially web3 firms moving funds across exchanges, entities, and service providers, the practical question is simple: how much leaves your account, how much arrives, and how long that takes. SWIFT can work well for many cross-border payments. You just need to price it as a route with multiple toll booths, not as a single flat-fee transfer.

Tracking Your Payment with MT103 and SWIFT GPI

The most frustrating part of a traditional international wire isn't always the delay. It's the lack of visibility while you wait.

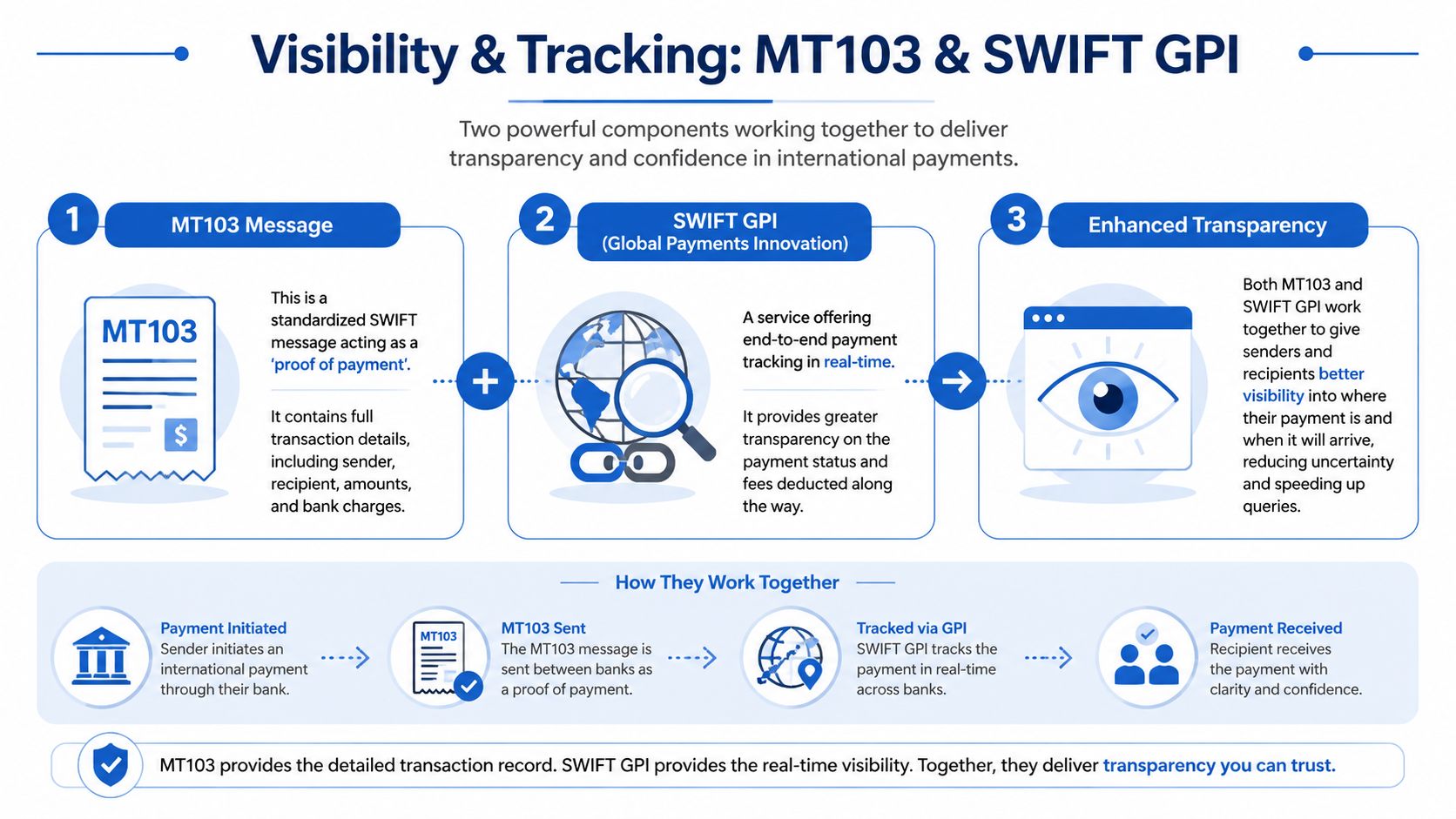

What the MT103 tells you

An MT103 is the standard customer payment message often used in SWIFT transfers. In practical terms, it acts like the formal proof that a payment instruction was issued.

Finance teams ask for it when they need to verify:

- who sent the payment

- who should receive it

- the amount and currency

- the banks involved

- the reference details tied to the transfer

If a vendor says funds haven't arrived, the MT103 is often the first useful document to request from the sending bank. It doesn't guarantee final credit, but it proves the instruction entered the banking system in a standardized form.

How SWIFT GPI changes the experience

Legacy SWIFT often had the reputation of being slow and opaque. That reputation didn't come from nowhere. But it's now incomplete.

According to Payoneer's guide to SWIFT payments, the newer SWIFT Global Payments Innovation (GPI) standard, which launched in 2023, now processes over 90% of payments within one hour. The same source notes that many online guides still cite legacy timelines without separating old SWIFT behavior from GPI-enabled flows.

That distinction matters. If your bank supports GPI on the corridor you use, your experience may be very different from the old “wait a few days and hope” model.

Key takeaway: Ask whether your bank or payment provider supports SWIFT GPI for your specific currency route. “SWIFT” alone doesn't tell you enough about speed.

What GPI means in practice

With GPI, the experience starts to look more like package tracking:

| Tool | What it helps with | What it doesn't guarantee |

|---|---|---|

| MT103 | Confirms the payment instruction exists | Final credit timing |

| SWIFT GPI | Better tracking and faster visibility | Universal instant delivery on every corridor |

For a business owner, the practical move is to ask for both when needed. Ask for the MT103 if you need payment proof. Ask whether the payment is traveling on a GPI-enabled route if you need better status visibility and a more realistic arrival estimate.

SWIFT vs Other Payment Rails for Global Businesses

A finance lead at a web3 company might pay the same supplier three different ways in one quarter. A law firm in the US may require a bank wire. A European contractor may prefer SEPA. A crypto-native market maker may want USDC. That is why the key question is not whether SWIFT is good or bad. It is where SWIFT fits, and where another rail gives you lower cost, faster delivery, or fewer surprises.

SWIFT still matters because it reaches banks almost everywhere and works well for larger cross-border payments into traditional bank accounts. But broad reach comes with a tradeoff. A SWIFT payment can pick up costs at several points in the chain, including the sending bank fee, one or more intermediary bank deductions, and foreign exchange markup if conversion happens along the route. For businesses that care about margin, that hidden cost stack matters as much as headline speed.

A practical comparison

| Payment Rail | Speed | Typical Cost | Best For | Reach |

|---|---|---|---|---|

| SWIFT | Usually business-day based, sometimes quicker on supported routes | Sender fees, possible intermediary fees, and FX spread can all apply | Large international vendor payments, cross-border corporate transfers | Global |

| Domestic wire | Usually same day or next day within one country | Often clearer and more predictable than cross-border wires | High-value local payments | Country-specific |

| ACH | Slower than wires, but low-cost for routine transfers | Usually lower than wires | Recurring domestic payments, payroll, lower-urgency transfers | Primarily domestic or corridor-specific variants |

| SEPA | Efficient for euro payments within supported regions | Often low-cost and predictable for EUR transfers | EUR payments inside Europe | Regional |

| Stablecoin rails such as USDC | Often fast and available around the clock | Network fees may be low, but total cost depends on conversion and off-ramp setup | Global contractor payouts, treasury movement, crypto-native operations | Global where recipients can receive or off-ramp |

The easiest way to compare these rails is to picture different delivery networks. SWIFT works like a secure postal system for banks. It is trusted and widely accepted, but the route may pass through multiple hands before the funds arrive. SEPA is more like a well-organized regional courier for euros. Stablecoin rails act more like sending value directly over the internet, fast in transit, but only useful if both sides can receive it and convert it cleanly when needed.

How businesses usually choose

Strong finance teams choose by payment job, not by habit.

- Use SWIFT when the recipient needs funds in a bank account, the payment is cross-border, and banking acceptance matters more than absolute speed.

- Use domestic wire for high-value local transfers where timing is important and both parties bank in the same country.

- Use ACH or SEPA for repeatable payouts where cost predictability matters more than same-day settlement.

- Use stablecoin rails when counterparties are crypto-capable, treasury needs are time-sensitive, or you want to avoid some correspondent banking friction.

- Use multiple rails together if your business pays a mix of vendors, employees, exchanges, and service providers across different regions.

For web3 companies, this choice is especially practical. You may raise capital in digital assets, pay cloud bills in fiat, settle exchange obligations quickly, and reimburse a global team through local bank systems. In that setup, SWIFT is often one rail in a broader treasury stack, not the whole stack.

A useful resource when comparing software across these options is this directory of BookkeepDIY payment and accounting tools, especially for teams that also want cleaner AP workflows and reconciliation.

If you are comparing rails at the operating-model level, this guide to cross-border payment options for modern businesses gives a helpful overview of how bank rails and newer alternatives fit together.

One more practical point. The performance gap between legacy SWIFT and newer GPI-supported flows is real, but it does not erase the cost question. Faster status updates and better routing visibility help operations. They do not automatically remove intermediary deductions or FX markup. For many businesses, the best payment rail is the one that arrives on time, costs what you expected, and matches how the recipient wants to get paid.

Tips for Minimizing SWIFT Costs and Delays

You can't control every bank in the chain, but you can remove a surprising amount of friction before the payment is sent.

Payment setup mistakes that cause friction

Most avoidable SWIFT problems begin with basic data quality.

- Match the beneficiary name exactly. If the legal entity name on the bank account doesn't match what you entered, compliance review can slow the payment or stop it.

- Use complete bank details. Missing account numbers, bank identifiers, addresses, or payment references create manual review work.

- Confirm the receiving currency. If your vendor expects one currency but your bank sends another, somebody in the chain may convert it at a rate you didn't plan for.

- Check who bears fees. If the receiving party expects the full invoice amount, fee deductions can create disputes unless you align expectations upfront.

Questions worth asking your bank or provider

A short conversation before sending can save a lot of back-and-forth later.

Ask these questions:

Will this payment use intermediary banks?

If yes, the chance of extra deductions rises.Is this route supported by SWIFT GPI?

Better tracking changes how you manage vendor expectations.Where does FX happen?

The answer tells you whether your own bank, an intermediary, or the recipient side may set the conversion economics.Can you provide the MT103 quickly if needed?

Finance teams shouldn't need a multi-day support thread just to get proof of payment.

Clean payment instructions do double duty. They reduce operational delays and make AML and KYC reviews easier for the banks handling the transfer.

If you work in cross-border payments or hire for teams that do, market demand is visible in roles like this Unlimit sales VP on Blockchain Jobs, which shows how much attention companies now give to modern payment infrastructure.

For web3 startups, there's one more habit worth adopting. Keep a corridor-by-corridor playbook. Document which bank routes are slow, which currencies create surprise fees, and which counterparties are better paid by another rail. Over time, that operating knowledge becomes as valuable as any bank relationship.

How OneSafe Streamlines Global and Web3 Payments

A modern platform helps by adding a clear operating layer around SWIFT that many traditional banks do not provide.

A good way to frame the problem is simple. SWIFT moves the message, but finance teams still need a dashboard for approvals, balances, payment records, FX decisions, and reconciliation. Banks often offer the rail without offering much visibility around the full job.

One example is OneSafe's business account for international payments. It supports SWIFT transfers alongside ACH, domestic wires, multi-currency accounts, corporate cards, and crypto-compatible workflows. For a business handling both fiat and digital assets, that matters because money rarely moves through just one system anymore.

Cost control is a big part of the value. OneSafe publishes a SWIFT fee of 0.35% + $50 in its stated pricing, which gives finance teams a clearer starting point than the usual bank model of base fee plus unclear intermediary deductions plus FX spread. That does not remove every corridor-specific cost, but it makes the first layer of the cost stack easier to predict.

That visibility matters even more for web3 companies.

A web3 finance team often has to pay a law firm over bank rails, receive revenue in stablecoins, convert part of treasury into fiat for payroll, and keep records that auditors and tax advisers can follow. SWIFT and stablecoins are not competing realities in that setup. They are two parts of the same operating system.

The practical challenge is coordination. If your team manages USD wires, multi-currency balances, and crypto movements in separate tools, simple questions become harder than they should be. Where did the fee hit? When did FX happen? Which payment reference matches the invoice? A platform that brings those workflows together can reduce manual follow-up and make month-end reconciliation less painful.

For founders expanding internationally, fundraising and payment operations often develop in parallel. Resources like this list to find Web3 investors in the US can help as you build the broader financial stack around global growth.

The broader lesson is practical. Understanding SWIFT helps you choose the right rail for each payment. Using a platform with clearer pricing and better operational visibility helps you control the hidden cost stack, set better expectations on speed, and run global finance with fewer surprises.

If your team needs one place to manage international wires, SWIFT transfers, multi-currency balances, and crypto workflows, OneSafe is worth evaluating. It is built for global businesses and web3 companies that need both fiat banking rails and digital asset operations without juggling separate systems.