You've probably felt the failure mode already. A team lead in London books travel on one card, a contractor in Latin America uses a virtual card for software, someone else pays an urgent vendor invoice after converting USDC to fiat, and finance still closes the month with screenshots, Slack approvals, and missing receipts spread across three systems.

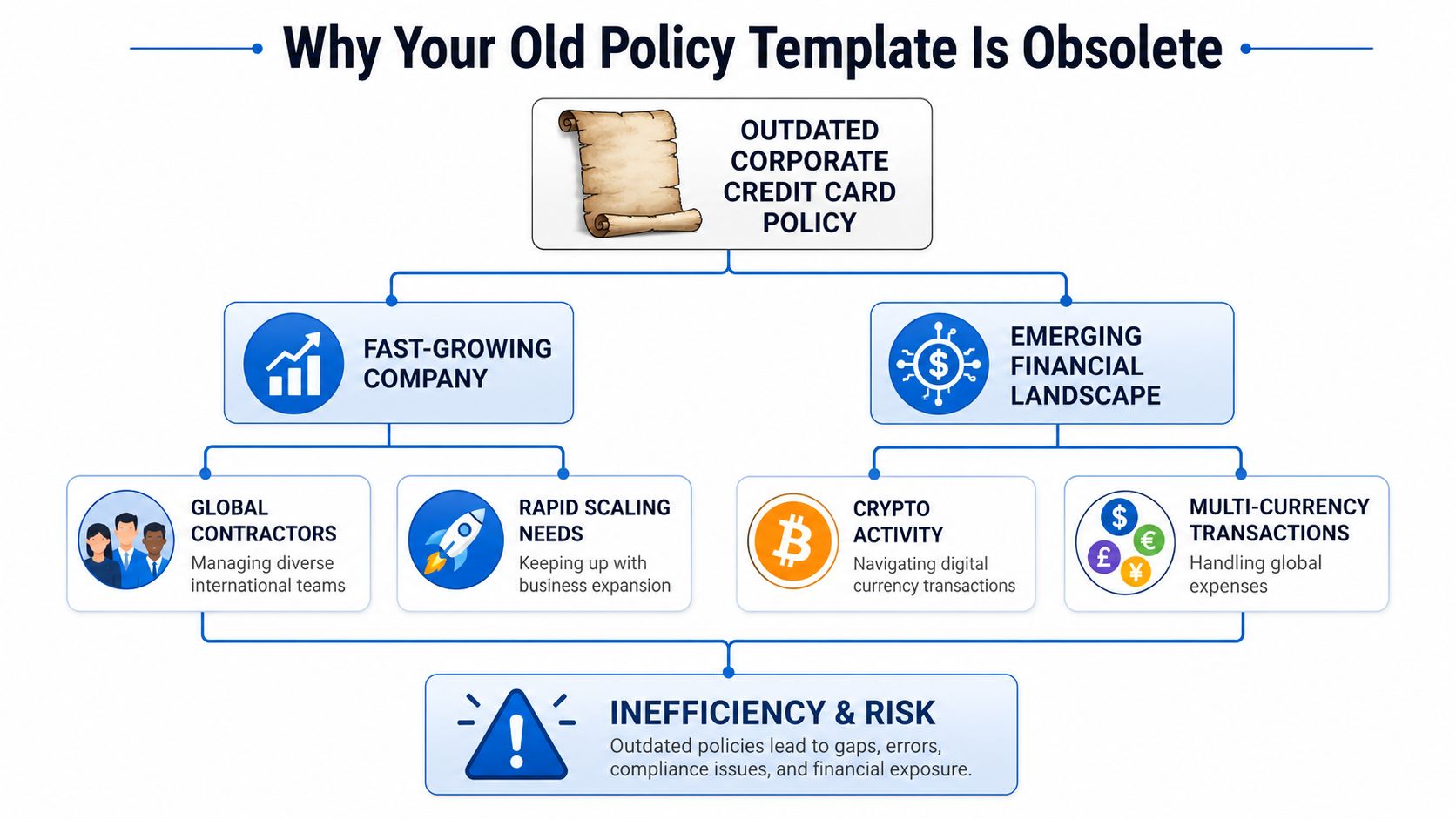

That's when a generic corporate credit card policy stops being an administrative document and starts becoming an operating risk. The old template assumes domestic employees, one base currency, standard reimbursements, and a clean line between banking and treasury. Fast-scaling global companies don't operate that way anymore, especially if they pay contractors, run multiple entities, or touch digital assets.

A modern policy has to do more than list approved expenses. It has to define who can get a card without relying on outdated personal-credit assumptions, control spend before it happens, document crypto-to-fiat activity in a way auditors can follow, and keep reconciliation from turning into month-end archaeology.

Table of Contents

- Replace personal-credit logic with role-based eligibility

- Set more than one limit

- Choose card types intentionally

- Block merchants you'll never approve

- Write separate rules for currency and funding source

- Define the crypto-to-fiat chain in plain language

- Treat web3-specific spend as a distinct class

- Separate spend approval from treasury approval

- Use the Always OK Ask First Never OK model

- Security controls need named owners

- Build an audit trail before anyone asks for it

Why Your Old Policy Template Is Obsolete

Most legacy policy templates were written for a business that no longer exists. They assume cardholders are employees in one country, expenses are paid in fiat, eligibility depends on personal credit, and reconciliation happens after the fact. That model breaks quickly when your company has global contractors, multiple entities, and treasury activity that moves between crypto and bank rails.

The scale of the shift isn't theoretical. The global corporate credit card market was valued at USD 37.2 billion and is projected to reach USD 65.4 billion by 2030, driven in part by real-time policy enforcement such as merchant category blocks and per-employee spending caps that modern platforms can automate (Grand View Research corporate cards outlook). That growth reflects a practical change in how companies manage spend. Finance teams want fewer reimbursements, tighter controls, and cleaner data at the point of purchase.

Start with purpose and scope

A usable policy starts with two plain statements.

First, purpose. Spell out that the card program exists to support legitimate business spend while controlling risk, preserving documentation quality, and reducing manual reimbursement workflows.

Second, scope. Name who the policy covers and what it covers. Include employees, contractors where permitted, entity-specific cardholders, virtual cards, physical cards, travel spend, recurring software, and any card activity connected to crypto-funded operations. If your company uses separate entities for hiring, treasury, or tax reasons, the policy should say which entity owns the liability for each card program.

Practical rule: If a finance reviewer has to guess whether a cardholder, entity, or transaction type is in scope, the policy is already too vague.

Use principles people can apply in real time

The strongest corporate credit card policy documents are short on legal filler and strong on operating principles. Three work well in practice:

- Business purpose first: Every charge must have a clear business reason, not just a receipt.

- Trust but verify: Cardholders can move fast, but the system records enough evidence for later review.

- Prevent before chasing: Use controls that stop bad spend at authorization instead of finding it weeks later.

This is also where modern treasury matters. Companies that are already rethinking how bank rails connect to digital assets should apply the same logic to spend controls and policy design, especially as banks and crypto integration continue to reshape finance operations.

A dated template usually fails in one of two ways. It's either too narrow to cover how the company spends, or so broad that nobody can enforce it. The fix isn't a longer document. It's a policy written for the current operating model you have today.

Building Core Controls for Card Issuance and Spending

A card policy gets tested at issuance, not at audit time. If the wrong people get access, the wrong limits get assigned, or the wrong merchants are allowed, finance inherits avoidable cleanup work every month.

There's also a behavioral reality to account for. A survey found that 27% of employees admit to using their company card for personal expenses, and 57% of organizations require receipt submission for every use as a baseline control for reconciliation and audit readiness (Upgraded Points company card survey). That's why core controls need to be explicit, not implied.

Replace personal-credit logic with role-based eligibility

Traditional card programs often assume eligibility starts with a personal credit check. That's a poor fit for international teams, newly formed entities, and contractor-heavy operating models.

A better approach is to issue cards based on role, spend pattern, and business need. For example:

- Frequent travelers: Physical cards with travel-related permissions.

- Vendor owners: Virtual cards tied to named subscriptions or suppliers.

- Country managers or entity leads: Higher limits with tighter approval expectations.

- Contractors with operational buying responsibility: Restricted cards with category controls and shorter review cycles.

If you need a platform that supports card controls as part of the operating setup, OneSafe corporate cards are one example of a system built around spend limits, merchant controls, and approval-based usage rather than a simple static card issue.

Set more than one limit

One limit is almost always the wrong limit. Monthly caps are useful, but they don't stop misuse on their own.

Use a mix of controls:

| Control type | What it does | Good use case |

|---|---|---|

| Per-transaction limit | Stops oversized purchases | Ad hoc buying and travel |

| Monthly limit | Caps aggregate exposure | Team leads and recurring spend |

| Category sub-limit | Restricts spend within a class | Meals, software, transport |

| Frequency limit | Stops repeat low-value misuse | General-purpose cards |

The point isn't to make cards hard to use. It's to match the card's permissions to the job.

Choose card types intentionally

Many teams treat physical and virtual cards as interchangeable. They aren't.

- Physical cards work for travel, in-person client meetings, and local transport.

- Virtual cards fit recurring SaaS, trial tools, agency retainers, and one-time online purchases.

- Single-purpose vendor cards reduce downstream confusion because the merchant, budget owner, and accounting treatment are usually obvious.

Don't issue a general-use card when a single-vendor virtual card will do the job. Broad access creates broad ambiguity.

Block merchants you'll never approve

Merchant Category Code controls are one of the cleanest first-line defenses in a corporate credit card policy. If a category is never acceptable, block it in software instead of writing a stern paragraph about it.

That often includes cash equivalents, gambling-related merchants, and categories your business has no valid reason to use. In many environments, it also makes sense to treat high-risk digital asset merchants separately unless treasury has expressly approved them.

A policy that relies on after-the-fact review alone asks finance to police behavior manually. A policy with issuance rules, layered limits, card-type logic, and merchant controls does most of the heavy lifting before the transaction ever posts.

Handling Multi-Currency and Crypto Transactions

In these circumstances, most standard templates typically collapse. They know how to describe airfare and meals. They don't know what to do when a company converts digital assets to fiat, funds operating spend from that conversion, and then needs an audit trail that ties treasury activity to card transactions across entities and currencies.

That gap is bigger than many teams expect. Seventy-three percent of finance teams report that their expense software can't automatically reconcile crypto transactions with fiat bank statements, which leaves a real compliance blind spot for companies using crypto in operating workflows (Concur on corporate card policy gaps).

Write separate rules for currency and funding source

Most policies focus only on the expense category. Modern teams need two extra fields in policy logic:

- What currency is the expense charged in?

- What funding path supported that expense?

For multi-currency operations, define whether the cardholder may:

- spend in local currency,

- spend in a non-home currency,

- accept issuer FX automatically,

- request treasury pre-funding in a specific currency,

- or use a dedicated entity card tied to a local account.

If your company operates across multiple balances and currencies, a platform like multi-currency business accounts can support the operational side. The policy still needs to state who approves foreign-currency spending, who owns FX exposure, and how those charges are documented.

Define the crypto-to-fiat chain in plain language

The hardest policy problem isn't “Can someone spend on the card?” It's “Can finance later prove how the spending was funded?”

For crypto-linked operations, your policy should require a documented chain with these elements:

- Treasury approval: Who approved the conversion from digital assets to fiat.

- Source record: Wallet or treasury reference for the originating digital asset movement.

- Conversion record: Evidence of the crypto-to-fiat conversion.

- Account destination: The bank or operating account that received fiat funds.

- Spend linkage: The card transaction or batch of transactions funded from that balance.

- Business purpose: Why the resulting spend was necessary for operations.

That language matters because many finance tools still treat the crypto event and the fiat event as unrelated records. Your policy should force them into the same evidence package.

Treat web3-specific spend as a distinct class

A corporate credit card policy for global and crypto teams should explicitly name web3-related expense types. Not because every one should be allowed, but because silence creates inconsistency.

Use a structure like this:

| Expense type | Default treatment | Evidence required |

|---|---|---|

| Standard SaaS in fiat | Allowed within role limit | Receipt and cost center |

| Travel in foreign currency | Allowed with travel rules | Receipt and trip purpose |

| Crypto-funded card spend | Ask first | Conversion and funding records |

| Direct crypto payment tied to operations | Ask first or treasury only | Invoice, wallet record, approver |

| Exchange-related spend | Treasury only or blocked | Named approval and purpose |

If your policy mentions “approved business expenses” but never mentions USDC, wallet-funded operations, exchange exposure, or invoicing in crypto, it doesn't reflect how your company actually spends.

Separate spend approval from treasury approval

One of the most common mistakes is letting a cardholder approval stand in for treasury approval. Those are different decisions.

A department lead can approve the need for software or travel. Treasury or finance should approve the funding path when digital assets, FX timing, or entity-level balance movements are involved. That separation reduces confusion later when auditors ask whether the purchase itself was approved or the conversion that enabled it was approved.

The practical trade-off is speed. More approvals can slow urgent purchases. The answer isn't to remove approval layers entirely. It's to pre-approve common scenarios, define escalation paths for edge cases, and keep crypto-linked funding workflows narrow enough that exceptions remain readable.

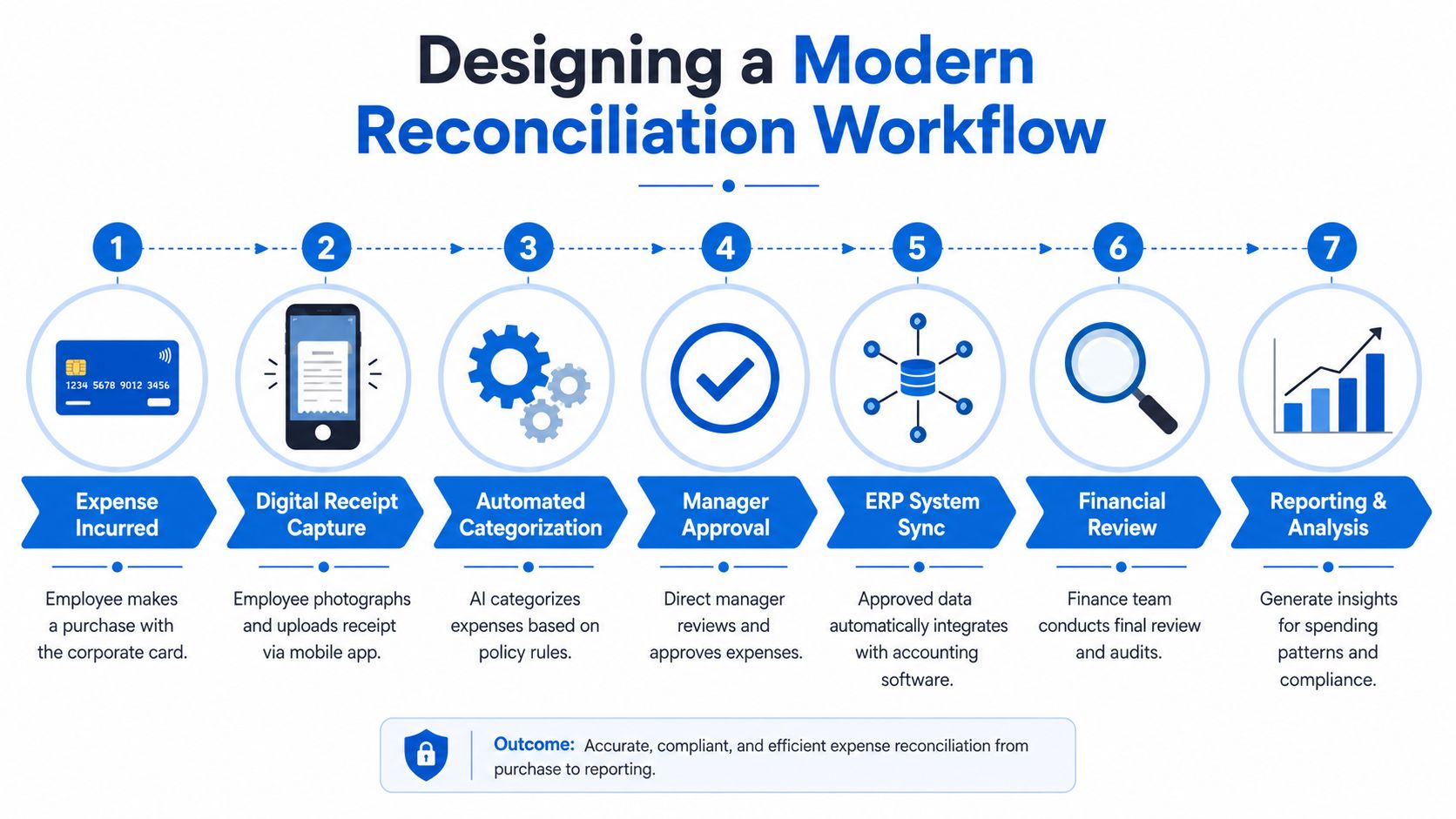

Designing a Modern Reconciliation Workflow

A policy only works when a transaction can move from purchase to ledger entry without finance stitching together five missing pieces. The cleanest workflows don't depend on memory. They depend on a sequence that cardholders can follow quickly and reviewers can verify without interpretation.

The infographic below shows the shape of that sequence.

From swipe to ledger entry

A well-run workflow usually looks like this in practice.

An employee makes a permitted purchase. Right after the transaction, they upload the receipt, add the business purpose, and code the cost center while the context is still fresh. Their manager reviews only what requires review. Finance then checks exceptions, not every routine line item.

That basic path gets more important when the transaction sits inside a more complex funding story. A crypto-funded software charge, for example, still needs a normal employee receipt and business explanation. But finance also needs the treasury-side records that show how fiat became available for that spend.

The best reconciliation workflows reduce the number of decisions people make after the transaction. They capture evidence while the facts are still obvious.

For teams tightening month-end close quality, a structured general ledger reconciliation guide is a useful companion because it shows how transaction support, account matching, and review discipline fit together beyond just card expenses.

Later in the workflow, many teams also benefit from seeing the process visually before they standardize it across departments.

Where teams usually break the chain

The workflow usually fails in one of four places:

- Receipt capture breaks first: The cardholder waits too long, loses the receipt, or uploads a non-itemized version.

- Coding gets deferred: Nobody tags entity, project, or department until month-end, when memory is weak.

- Approvals become performative: Managers approve in bulk without checking business purpose.

- Treasury and spend records live apart: Card data sits in one system, while conversion evidence sits in another with no shared reference.

A resilient corporate credit card policy should force the workflow to answer these questions for every transaction class:

- Who submits the evidence?

- What must be attached?

- Who approves it?

- When does finance escalate it?

- Where is the final record stored?

Make exceptions easy to spot

Good workflows don't ask finance to inspect every normal charge with the same intensity. They let standard purchases move through a light process and surface exceptions clearly.

That means your policy should distinguish between:

- routine recurring software,

- ordinary travel and meals,

- first-time vendors,

- foreign-currency exceptions,

- and anything connected to crypto conversion or web3 invoicing.

When every transaction follows the same generic queue, important edge cases get buried. When the workflow is tiered, the finance team spends time where judgment is needed.

Enforcement Security and Audit Preparedness

A corporate credit card policy fails when it promises controls that the system can't enforce. Finance teams then end up arguing over violations after the money is gone. That's expensive, inconsistent, and avoidable.

A stronger model uses technology for routine enforcement and people for judgment. One practical framework is a two-tiered system where automated controls handle about 80% of enforcement, while human review focuses on periodic oversight and escalations. A common failure is publishing rules that don't map to actual card-software controls, which creates policies that look strict and operate loosely (Ken from Finance on corporate card policy enforcement).

Use the Always OK Ask First Never OK model

This framework works because employees can apply it quickly.

Always OK should include clearly permitted, low-ambiguity spending categories tied to role and purpose. Think approved software on a named vendor card, in-policy travel, or a budgeted recurring service.

Ask First should cover transactions that might be legitimate but need context. Foreign-currency exceptions, unusual project costs, crypto-linked operating spend, and new vendors usually belong here.

Never OK should be short, specific, and blocked where possible. Personal purchases, card sharing, unapproved cash-equivalent transactions, and prohibited merchant categories should not rely on a warning in a PDF alone.

Operating principle: Every written rule should point to a control, an approver, or a stored record. If it points to none of those, it's probably not enforceable.

Security controls need named owners

Security language in card policies often stays too generic. “Keep card information secure” isn't enough for a global team handling cards, digital assets, and multiple banking environments.

Name the control and the owner. Examples include:

- cardholder MFA for platform access,

- role-based permissioning for card creation and limit changes,

- immediate freeze and reporting steps for compromised cards,

- and secure digital asset custody procedures for treasury-controlled funds.

If your workforce includes contractors, employer-of-record staff, or PEO-supported hires across jurisdictions, it also helps to understand how enforcement choices intersect with workforce policy risk. The legal risks of PEO policy enforcement are worth reviewing when your card rules apply across mixed employment structures.

Build an audit trail before anyone asks for it

Audit readiness isn't a separate project. It's the byproduct of consistent evidence capture.

For standard card transactions, retain:

- receipt,

- business purpose,

- approver,

- coding information,

- and any exception note.

For crypto-adjacent spend, retain the normal card record plus:

- treasury authorization,

- conversion evidence,

- account movement support,

- and a reference tying the treasury event to the expense event.

The audit test is simple. Could a reviewer who wasn't present understand why the charge happened, who approved it, which entity bore the cost, and how the funding moved? If not, the documentation standard is still too weak.

Enforcement should feel predictable, not dramatic. First-time accidental misuse should trigger re-education and cleanup. Repeated or intentional misuse should change privileges. That's not punitive. It's what makes the policy believable.

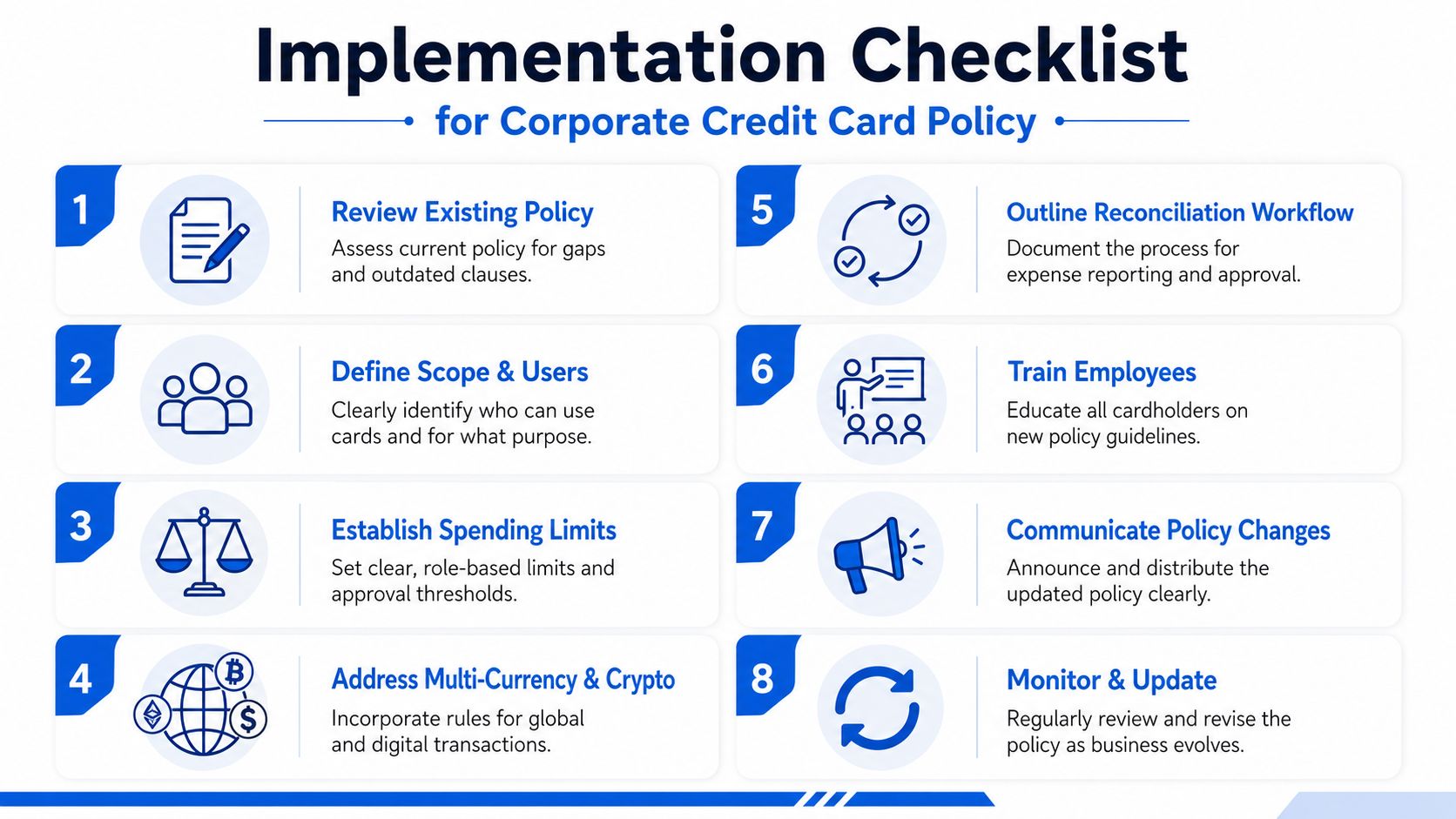

Implementation Checklist and Sample Policy Language

Organizations don't need another abstract policy template. They need a rollout path that turns a draft into operating behavior. That means fewer pages, clearer ownership, and language that covers edge cases before they show up in closing week.

A common weak point is documentation. Policies that fail to specify receipt format, submission rules, or similar documentation details can create a 60% increase in reconciliation delays, and mature programs also use trigger-based reviews such as adding 25+ employees or opening a new entity to keep the policy current (Ramp best practices for corporate credit card policy).

Implementation checklist

Use this sequence when you roll out or rebuild your corporate credit card policy.

Audit current reality

Pull recent transactions and identify where the existing policy doesn't match actual behavior. Focus on cardholder types, foreign-currency spending, recurring vendor use, and any crypto-linked workflows.Define cardholder classes

Separate employees, contractors, executives, entity leads, and vendor-card owners. Each group should have different permissions and review expectations.Map rules to system controls

Before publishing anything, confirm your card platform can enforce the rules you're writing. Limits, merchant restrictions, approval routing, freeze controls, and user permissions should all be testable.Standardize evidence requirements

Decide what counts as valid documentation. Be explicit about formats, timelines, and required fields.Create an exceptions lane

Foreign-currency edge cases, new vendors, and treasury-linked expenses need a clear escalation path.Train before issuing

Don't send the policy as an attachment and hope people absorb it. Run a short onboarding session and require signed acknowledgment.Launch with review dates

Put review triggers in the policy itself so it gets revisited when the company structure changes.Track violations by pattern

If the same mistake repeats, fix the rule, the training, or the system control. Don't just keep sending reminder messages.

Sample policy language

These clauses are meant to be adapted, not copied blindly.

Card eligibility is based on business need, role, and approval by the designated department lead and Finance. Personal credit history is not the primary basis for issuance where the company uses role-based controls and corporate liability.

Cardholders may use company cards only for approved business expenses within assigned limits, merchant restrictions, and entity scope. Personal use is prohibited, even if the cardholder intends to reimburse the company later.

All transactions require supporting documentation in the format specified by Finance. Acceptable documentation must be legible and must include the merchant, date, amount, and business purpose. Itemization is required where available.

Foreign-currency transactions are permitted only where the cardholder's role allows them or where pre-approval has been recorded. The applicable entity, business purpose, and project or department must be identified at submission.

Any expense funded directly or indirectly through crypto-to-fiat conversion must include a linked record of the treasury approval, conversion event, destination account, and corresponding expense documentation sufficient to support accounting, audit, and tax review.

Web3-specific expenses, including crypto invoicing, exchange-related charges, gas-fee reimbursements, or wallet-linked operating costs, require review under the company's designated approval path and may be restricted to treasury-authorized personnel.

Lost, stolen, or compromised cards must be reported immediately through the approved reporting channel. Finance may suspend the card pending review and reissue subject to operational need.

Repeated failure to comply with documentation, approval, or usage requirements may result in limit reduction, temporary suspension, or revocation of card privileges. Intentional misuse may trigger disciplinary action under company policy.

A final drafting note matters more than teams expect. Keep the full policy readable. If cardholders need counsel to interpret ordinary cases, they won't use it during real purchases. The document that works in practice is the one people can apply under time pressure.

If your team operates across entities, currencies, and crypto-linked workflows, it helps to use a system built for that reality. OneSafe offers multi-currency business accounts, payments, and corporate cards with spend controls, approvals, and support for both fiat and crypto-connected operations, which can make it easier to enforce the kind of policy described here without stitching together separate tools.