A lot of finance leads hit the same point at the same time. Revenue is climbing, payment volume is getting more international, someone on the treasury side has added crypto workflows because the business needs them, and then a banking partner or auditor asks a simple question: how are you monitoring transactions for suspicious activity across all of it?

That question exposes whether your controls are real or cosmetic. If your company moves money through ACH, wires, SWIFT, cards, stablecoins, and wallet transfers, every handoff between those rails creates risk. The trouble is that many teams still treat transaction monitoring as a compliance tool you buy after you scale. In practice, it becomes part of your operating model much earlier than that.

Table of Contents

- Do small teams need transaction monitoring tools

- Should finance or compliance own the system

- What causes most failed implementations

- Can one system really cover fiat and crypto

- What should the first ninety days focus on

The Unseen Risk in Every Global Transaction

A familiar scenario: the company has just expanded into new markets, contractor payments are going out in multiple currencies, customers want more payout options, and the treasury team has added digital asset rails to move faster. Operations feel modern. Controls often don't.

The first real test usually isn't an internal one. It comes from outside. A bank asks for more detail on transaction flows. An audit request drills into source of funds, counterparties, and unusual movement between wallets and bank accounts. Finance realizes too late that reporting is fragmented across providers, spreadsheets, and manual exports. At that point, transaction monitoring isn't a procurement project. It's a risk containment exercise.

This is why the market for these systems has expanded so aggressively. The global transaction monitoring tools market is projected at USD 21.44 billion in 2026 and approximately USD 48.06 billion by 2031, with a projected 14.62% CAGR, according to Mordor Intelligence's transaction monitoring market analysis. That kind of growth doesn't happen because firms enjoy buying compliance software. It happens because companies handling money can't stay credible with weak oversight.

What finance leaders often underestimate

New Heads of Finance usually walk in looking at cash flow, entity structure, payment operations, and close processes. All important. But transaction monitoring sits underneath those workflows because it answers a harder question: should this payment happen at all, and if it already happened, can the business explain it?

If you can't answer that cleanly, several things break fast:

- Banking relationships get fragile. Banks want confidence that suspicious activity won't move through your stack unchecked.

- Treasury visibility becomes misleading. You may know balances but not behavioral risk.

- Investigations get expensive. Teams burn time reconstructing context after an alert instead of reviewing an alert with context already attached.

Practical rule: If your team can't trace a transaction from initiation to beneficiary, with customer context and reason for payment, you don't yet have a monitoring program. You have records.

A good starting point for executive alignment is a concise boardroom guide for AML strategies, especially when you need directors and finance stakeholders to understand why monitoring belongs in core operations rather than in a side compliance queue.

What transaction monitoring really is

At a practical level, transaction monitoring is the business capability that lets a company review activity across accounts, payment methods, and counterparties in time to act. For a company operating across fiat and crypto, that means identifying patterns that don't make sense for the customer, don't fit expected treasury behavior, or suggest concealment, layering, sanctions exposure, or misuse of company rails.

The mistake is to think only obviously criminal transactions matter. In real life, what triggers scrutiny is often inconsistency. Amounts that don't fit a profile. Round-trip flows between rails. Velocity that defeats review windows. A payment that looks harmless on one ledger and suspicious once paired with wallet activity.

That's the unseen risk in every global transaction. Not the single payment. The missing context around it.

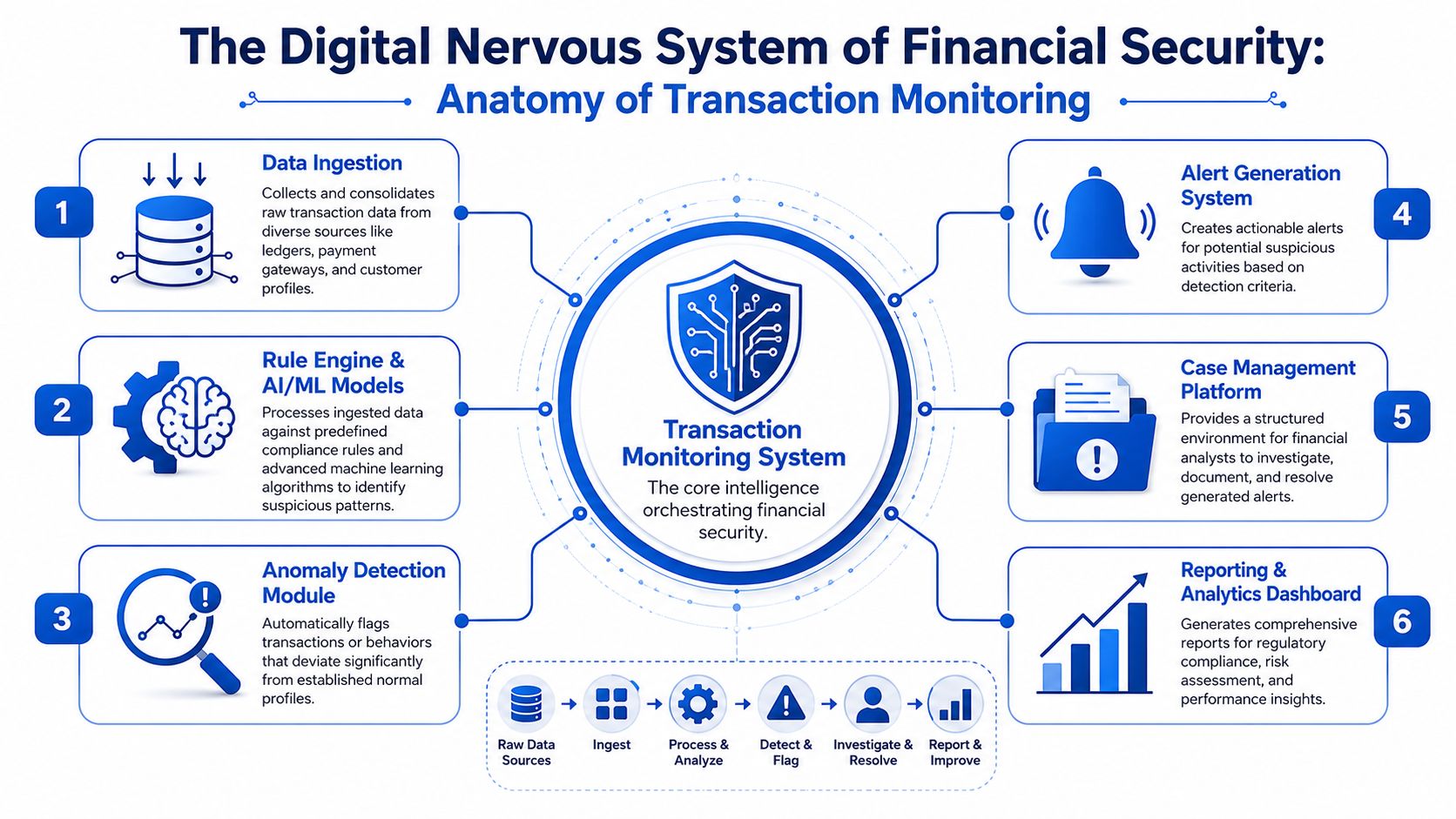

Anatomy of a Transaction Monitoring System

The easiest way to understand transaction monitoring tools is to stop thinking about them as one product. They are closer to a security system for a vault. Cameras collect evidence. Sensors look for triggers. A control panel decides what matters. An alarm routes work to humans. An investigation room documents what happened and what to do next.

What enters the system

The first layer is data ingestion. At this stage, many implementations fail before rule writing even starts. A monitoring engine is only as good as the inputs it receives and the consistency of those inputs.

For a cross-border business, useful inputs usually include:

- Payment rail data: ACH records, wire messages, SWIFT details, card activity, payout files, and internal transfers.

- Customer and account data: KYB or KYC details, beneficial ownership information, jurisdiction, expected activity profile, and account status.

- Crypto data: wallet addresses, deposit and withdrawal records, blockchain exposure data, conversion events, and custody activity.

- Operational context: invoice references, merchant category, employee card controls, approval metadata, and support notes.

If those records sit in different systems with different timestamps, different identifiers, and different naming conventions, the monitoring tool will generate weak alerts. Teams often blame the vendor when the underlying problem is poor data mapping.

How detection actually happens

Once data lands in the platform, the next layer is the rules engine. Rules catch straightforward risk signals. Think of transactions just under a reporting threshold, bursts of activity from a new customer, payment routes that don't match stated business purpose, or movement involving restricted jurisdictions. Rules are not glamorous, but they remain the foundation because they are explainable and easy to defend.

Then comes AI or machine learning scoring, where the system looks for patterns that simple thresholds miss. According to Alessa's review of transaction monitoring software, advanced AI and analytics can reduce false positives by 30 to 50 percent while increasing genuine alert detection. That's not just a model performance detail. It changes whether analysts spend their day clearing noise or working actual risk.

A functioning setup usually combines both:

- Rules for policy certainty. These align to known typologies, internal risk appetite, and regulator expectations.

- Models for behavior shifts. These help surface combinations of events that look normal in isolation but suspicious together.

- Anomaly detection for edge cases. This catches activity that breaks from a customer or treasury pattern even when no single rule fires cleanly.

Good systems don't replace analysts. They give analysts less noise and better evidence.

The final stages are alert generation, case management, and reporting. During these stages, operations either become disciplined or chaotic. A solid case management layer should show the transaction, the trigger logic, linked customer data, prior alerts, review notes, and disposition history in one place.

If that workflow is weak, analysts start working outside the platform. They copy data into spreadsheets, use chat threads for escalation, and leave no coherent audit trail. The tool may still produce alerts, but the program won't stand up under scrutiny.

A mature monitoring stack also needs a reporting layer. Not because dashboards are impressive, but because leadership and auditors need to see whether rules are firing appropriately, whether alerts are escalating sensibly, and whether the system is aligned to real risk instead of theoretical coverage.

Why Regulators Mandate Transaction Monitoring

The main reason regulators mandate transaction monitoring is simple. They don't trust manual review to catch suspicious activity at operational scale, and they're right not to.

When a business handles customer funds, cross-border payments, card spend, or digital assets, regulators expect more than a written AML policy. They expect a live control environment that can detect, escalate, and document suspicious patterns across actual transactions. That's why transaction monitoring tools have shifted from optional software into expected infrastructure.

The market reflects that shift. Transaction monitoring tools are projected to reach USD 49.07 billion by 2030, according to Research and Markets' transaction monitoring report. That projected growth is tied to escalating financial fraud and stricter requirements for real-time monitoring. The practical takeaway isn't about market size. It's that regulators, banks, and examiners now treat monitoring capability as part of basic operational fitness.

This is really about access to the financial system

Most finance leaders first interpret AML controls as a legal requirement. That's true, but it misses the bigger operating reality. Monitoring is what keeps counterparties, banks, and payment partners comfortable enough to keep doing business with you.

A weak program creates predictable consequences:

- Bank reviews become harder. Your team gets repeated requests for evidence instead of a straightforward control narrative.

- New corridors become slower to open. Partners will hesitate if your payment flows look opaque.

- Incidents become reputation events. If suspicious activity moves through your platform and you can't explain your response, the issue spreads beyond compliance.

For crypto-linked businesses, that pressure is even stronger because the business model already sits closer to perceived risk. The firms that stay bankable are usually the ones that can show transaction oversight in concrete terms, not the ones with the longest policy manual. That's also why many operators are moving toward automated compliance for the future of digital assets, where monitoring is embedded into the operating flow instead of bolted on afterward.

What regulators expect to see

Regulators don't all use the same words, but the operational expectations are consistent. They want automated systems that monitor activity continuously, cover the breadth of the business, and produce an auditable record of how alerts were handled.

In practice, that means your program should answer questions like these:

- Coverage: Are all relevant accounts, payment channels, and transaction types included?

- Calibration: Do the rules reflect your real risk profile, products, geographies, and customer base?

- Governance: Who reviews alerts, who escalates, and who decides whether a case is suspicious?

- Evidence: Can you show why an alert fired and what information the analyst used?

A monitoring program fails long before an enforcement action. It fails the moment your team can't explain why a risky transaction was missed or why a harmless one consumed hours of review.

What doesn't work is a checkbox deployment. Buying a tool, enabling generic scenarios, and assuming coverage is enough tends to create two bad outcomes at once: too many low-value alerts and gaps in the places that matter. Regulators notice both.

The better view is this: transaction monitoring is the mechanism that proves your company can be trusted with payment access. That's the core license-to-operate issue.

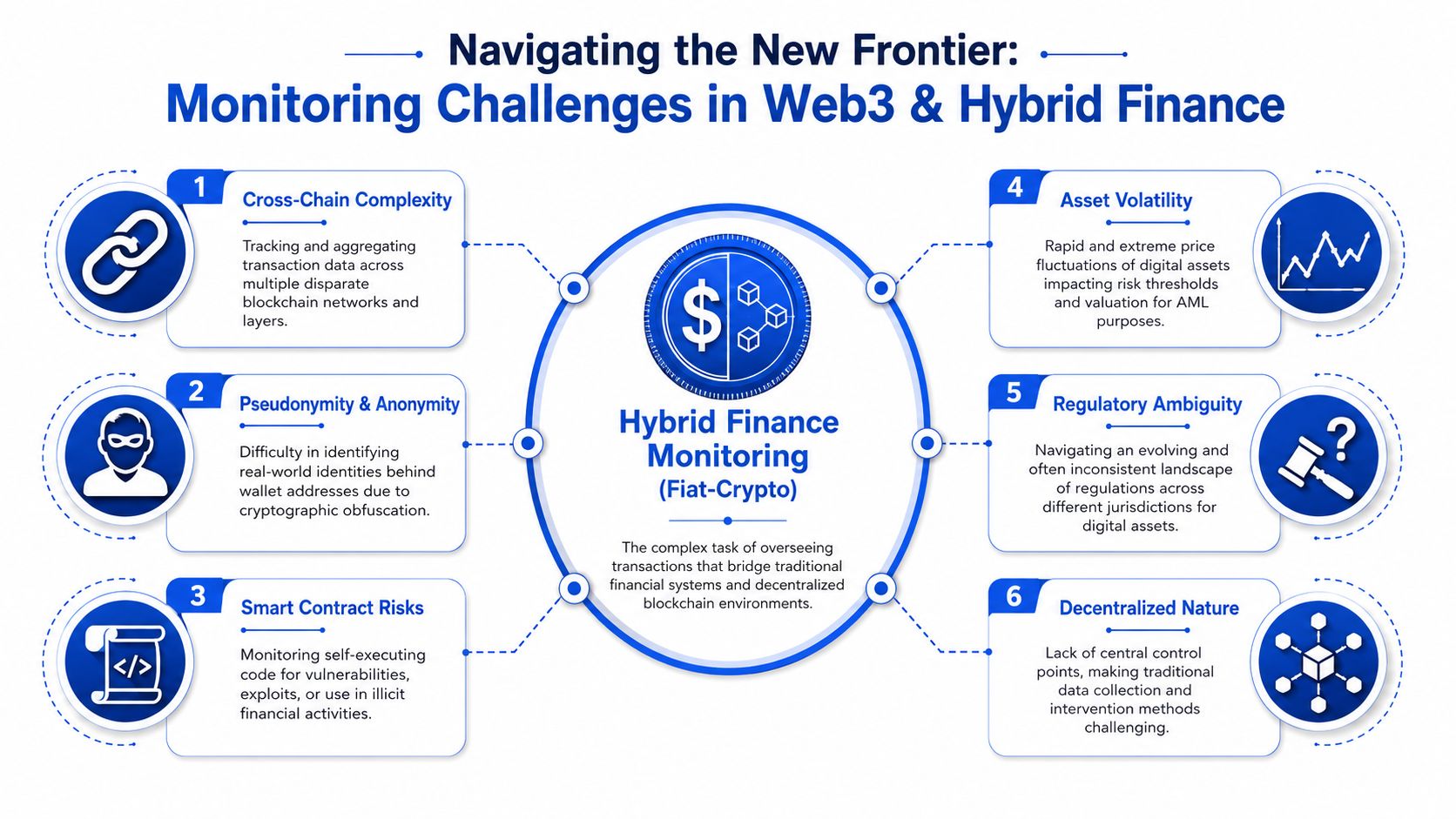

Unique Monitoring Challenges in Web3 and Hybrid Finance

Most guidance on transaction monitoring tools still splits the world into two buckets. Traditional finance on one side. Pure crypto monitoring on the other. That split doesn't help teams operating in the middle, where money moves from bank accounts to wallets, from stablecoins to fiat balances, and back again inside one treasury flow.

That middle ground is where the hardest monitoring problems live.

Where standard setups break

The most useful framing here comes from the underserved fiat-crypto hybrid monitoring gap described by Complytek's guidance on selecting a transaction monitoring tool. Regulators expect automated systems to cover all accounts and transactions, including crypto transactions, yet many vendor guides still don't explain how to tune controls for hybrid risk patterns.

That gap shows up in several ways:

- Fiat tools often ignore blockchain context. They can review wires and ACH activity but miss what happened before or after value moved on-chain.

- Crypto tools often stop at wallet behavior. They may identify risky exposure on-chain but don't connect that signal to bank account activity, invoice behavior, or card usage.

- Data integrity breaks across providers. One provider holds payment data, another holds custody data, and a third holds customer profile data. Analysts end up investigating fragments.

This is why hybrid teams need more than a list of vendor features. They need a monitoring design that can correlate events across rails and time windows.

A good mental model is not "fiat plus crypto." It's one customer risk story expressed through different transaction systems.

The hybrid risk patterns teams miss

The tricky cases usually aren't dramatic. They're operationally subtle.

A customer receives funds through one rail, converts quickly, moves value through a wallet path that shortens visibility, then returns proceeds to fiat with a business explanation that sounds ordinary. A traditional rules engine may see several acceptable events. An on-chain tool may see exposure but not know the customer profile or the related fiat disposition. The risk sits in the sequence.

Common blind spots include:

- Settlement timing mismatches: blockchain movement can finalize faster than fiat settlement and create windows that criminals exploit.

- Wallet attribution gaps: the address may be visible, but ownership and relationship to the fiat account may be unclear.

- Conversion events without context: a crypto-to-fiat or fiat-to-crypto conversion may be legitimate treasury management, or it may be a laundering step. The distinction depends on behavior, counterparties, and customer profile.

- Cross-rail layering: activity that looks clean on one rail may become suspicious once linked to another.

Hybrid monitoring fails when each team reviews its own rail and assumes someone else is connecting the dots.

For global operators serving web3 entities, this challenge is not theoretical. Treasury, payments, compliance, and operations all touch the same value movement from different systems. If your company supports businesses that live in both worlds, your controls have to do the same. That's why a growing number of teams evaluating infrastructure for digital-asset operations start with providers that already understand web3 financial operations as a combined fiat-and-crypto problem, not as two separate procurement decisions.

The best monitoring design for hybrid finance does three things well. It unifies identifiers across rails, preserves complete event history, and lets investigators see time-sequenced behavior instead of isolated transactions. Without those three elements, the tool may still be useful, but it won't close the hybrid gap.

How to Choose Your Transaction Monitoring Solution

At some point, every finance lead sees the same failure mode. A payment leaves the fiat account, value converts into a digital asset, funds move across wallets, and the team cannot reconstruct the full path fast enough to decide whether it was routine treasury activity or something that needs escalation. The selection mistake usually happened earlier, during procurement. The company bought a tool that worked on one rail and assumed the rest could be stitched together later.

That assumption gets expensive.

Choose a monitoring platform based on how it will run inside your operation day after day. Alert volume, investigation time, evidence retention, rule tuning, and cross-system handoffs matter more than a polished dashboard. A strong demo shows the full lifecycle in your environment: ingestion, alert creation, enrichment, analyst review, escalation, SAR support, and closure with an audit trail intact.

Questions that matter in vendor reviews

Start with the hard test. If your business moves money across bank accounts, stablecoins, exchanges, and customer wallets, ask the vendor to walk through one complete cross-rail scenario in the product. The case should include the customer profile, source of funds context, conversion event, wallet behavior, and final payout. If they can only show fiat monitoring in one screen and blockchain activity in another, you are still buying fragmentation.

Signal quality matters just as much. Alessa's transaction monitoring overview notes that advanced AI and analytics can reduce false positives while improving detection quality. That is a practical buying criterion. Teams rarely fail because the system produced too few alerts. They fail because analysts spend their day clearing weak alerts and miss the one case that deserves attention.

These questions separate usable systems from expensive backlog generators:

- Can it monitor both rails in one investigation flow? Analysts should not have to export fiat activity from one system and reconstruct wallet movement in a spreadsheet.

- Can compliance tune scenarios without waiting on engineering? If every threshold change sits in a product queue, your rules will lag behind your risk profile.

- Does it keep evidence in a regulator-ready form? You need alert logic, inputs, case notes, linked entities, approvals, and disposition history preserved and easy to retrieve.

- How well does it connect to adjacent controls? The monitoring stack should pass data cleanly to onboarding, sanctions screening, case management, and finance records. Teams that already review control quality in adjacent processes often see the same weak spots during a detailed audit of accounts payable controls.

- What happens under load? Ask how alerts are prioritized, deduplicated, and routed during spikes in payment volume or market stress.

- Can investigators explain the alert? Black-box scoring creates problems during escalation. Analysts need to see why the system flagged the activity.

A useful adjacent read for anyone evaluating workflow-heavy regulated tooling is this guide to legal tech for law firms. Different function, same operational lesson. Tools that look strong in isolation often break at the handoff points where real work gets done.

Build vs Buy analysis for transaction monitoring

For startups and mid-market operators, the decision is usually less about philosophy and more about whether the company can support monitoring as an ongoing product.

| Factor | Build (In-House) | Buy (Vendor Solution) |

|---|---|---|

| Coverage | Can be customized tightly to your business, but only if you already understand the typologies, data model, and edge cases you need to detect | Faster route to baseline coverage, though hybrid edge cases still need configuration |

| Speed to launch | Slow if customer, payment, and wallet data live in separate systems | Faster if APIs, entity resolution, and case workflows are already mature |

| Control | Full control over rules, interfaces, and data handling | Less control over roadmap, model design, and release timing |

| Tuning burden | Your team owns thresholds, regression testing, governance, and documentation | Vendor supplies baseline logic, but your team still owns calibration and approvals |

| Audit readiness | Strong if you build logs, versioning, evidence capture, and review controls from the start | Often better on day one because logs, case trails, and permissions are already built |

| Maintenance | High ongoing burden across engineering, data, product, and compliance | Lower technical burden, but vendor oversight and periodic validation still sit with you |

| Hybrid specialization | Possible if your business has unusual fiat-crypto flows and enough internal expertise to model them | Varies widely. You need to test real cross-rail scenarios, not accept generic claims |

My rule is simple. Build if hybrid monitoring is part of your product advantage and you have the budget, data discipline, and long-term ownership to maintain it. Buy if you need a dependable control environment soon and your team cannot justify building a monitoring platform beside the core business.

The worst option is the half-owned model. A company buys a vendor, turns on default scenarios, and assumes the tool will stay effective on its own. It will not. Someone has to own rule changes, alert reviews, model validation, and feedback from investigations. If ownership is vague, alert quality declines fast, especially in fiat-crypto environments where typologies shift faster than standard rule packs do.

Implementing and Operating Your Monitoring System

A monitoring program usually breaks during implementation for boring reasons. Missing fields. Bad timestamps. Duplicate customer records. Inconsistent identifiers between payment systems and case tools. The implementation plan matters because the quality of your daily operations is largely set there.

Modern systems are built for speed. According to Instant Payment Guide's overview of real-time transaction monitoring systems, event-driven architectures using tools such as Apache Kafka and Apache Flink can score and flag transactions in milliseconds, reducing risk assessment latency to under 100 milliseconds. That matters when value can move across channels before a batch process even starts.

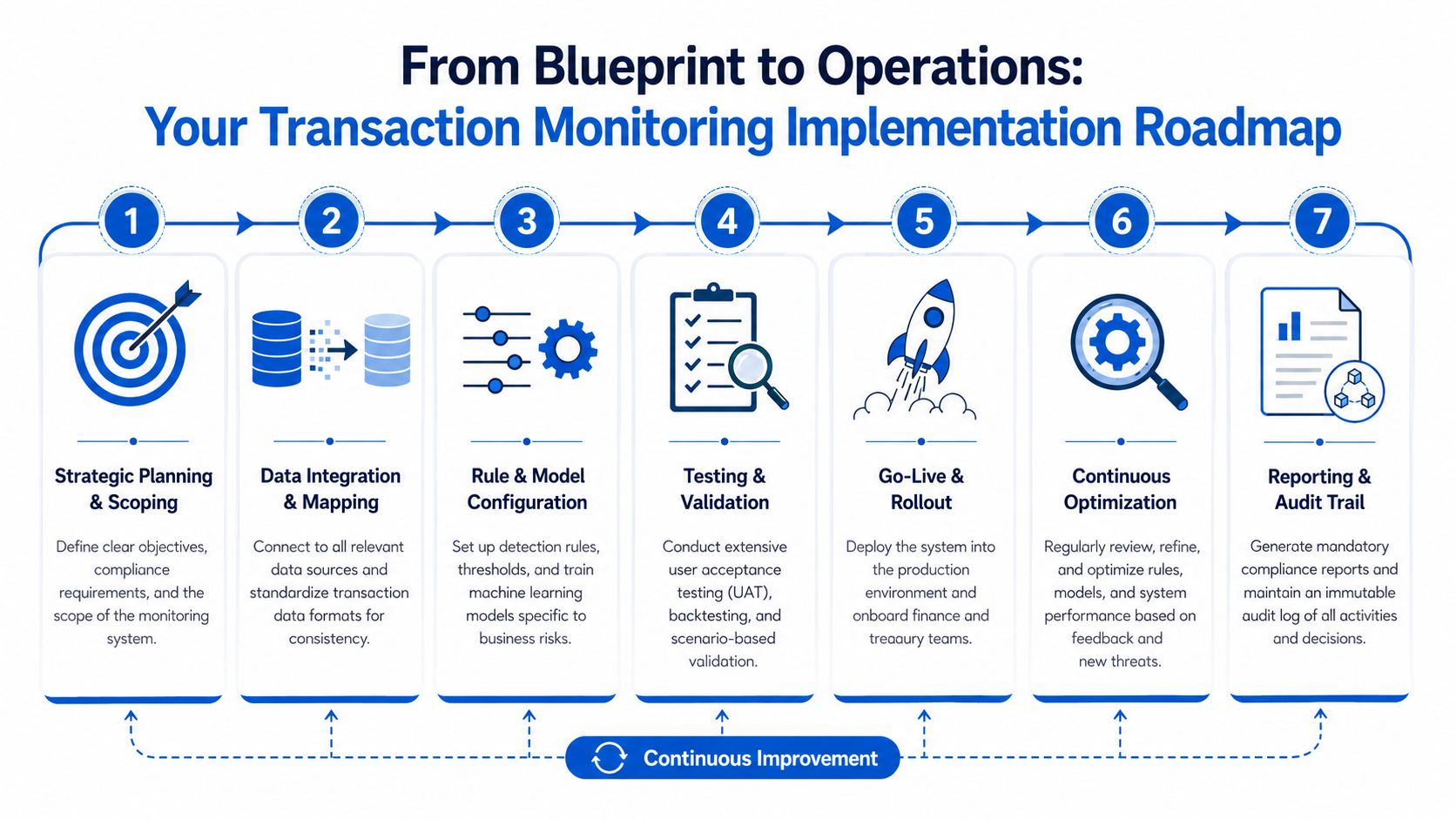

A rollout sequence that works

The cleanest implementations follow a phased approach. Not because methodology is fashionable, but because alert quality depends on sequencing.

- Scope the risk model first. Define which products, entities, geographies, counterparties, and payment types the system must cover. If you skip this, you'll end up with generic scenarios that don't fit the business.

- Map data before writing rules. Tie together payment events, customer identifiers, approval records, and wallet references. This stage surfaces most hidden operational debt.

- Configure initial rules conservatively. Start with a defensible core set tied to known risk patterns and your actual business model.

- Run testing with historical and simulated activity. Compare expected outcomes to system behavior. Review both missed cases and noisy alerts.

- Launch with escalation ownership defined. Every alert type needs a queue, a reviewer, a disposition standard, and a path for escalation.

The architecture should support streaming ingestion where possible. For hybrid businesses, that usually means transaction events from fiat payment systems, card processors, conversion workflows, customer systems, and digital asset infrastructure all flow into one monitoring layer or into coordinated layers with shared case context.

A useful implementation check is whether finance can reconcile what compliance sees. If the monitoring team and the treasury team can't line up the same event history, your data model still needs work. This is similar to what good finance teams already do when improving accounts payable audit readiness. The principle is the same: consistent records, clear approvals, and a traceable chain of events.

What day to day operations should look like

Once live, the system needs operational discipline more than technical novelty.

A working daily model usually includes:

- Triage queues by risk type or urgency. Not every alert should compete in one flat inbox.

- Case enrichment at the moment of review. Analysts need transaction details, linked customer data, and prior history without hunting across systems.

- Clear closure reasons. "Reviewed" is not a closure reason. The decision should explain why the activity was consistent with expected behavior or why it escalated.

- Regular tuning reviews. False positives, repeated low-value scenarios, and missed patterns should trigger rule changes, not frustration.

Fast alerting only helps if case handling is equally disciplined. Real-time detection with slow investigation still leaves the business exposed.

What doesn't work is a set-and-forget launch. Criminal typologies shift, product flows change, and business expansion creates new normal behavior that old rules may misread. Good teams treat transaction monitoring as a living control. They review it with the same seriousness they apply to treasury, approvals, and customer risk.

Frequently Asked Questions About Transaction Monitoring

Do small teams need transaction monitoring tools

Yes, if the business moves customer funds or operates across higher-risk rails. Team size doesn't change the need for visibility. Smaller teams suffer more when monitoring is weak because they have less capacity to reconstruct events manually.

A lightweight setup can still be credible if it covers all relevant transaction types, routes alerts clearly, and preserves an audit trail.

Should finance or compliance own the system

Compliance should own the policy logic, escalation standards, and suspicious activity review process. Finance should own the operational data quality, payment context, and reconciliation alignment. The system works best when neither function treats it as someone else's problem.

In practice, one senior owner should be accountable for the program, with named support from treasury, operations, data, and engineering.

What causes most failed implementations

Three issues show up repeatedly.

- Bad data mapping: transactions, customer records, and wallet events don't join cleanly.

- Generic scenarios: the rules reflect a vendor template instead of the company's actual risk profile.

- No tuning owner: everyone assumes someone else will refine thresholds and alert logic after launch.

If you're seeing lots of alerts with little investigative value, the problem is usually calibration or data quality, not just alert volume.

Can one system really cover fiat and crypto

Sometimes yes. Often partially. The better question is whether one control framework can cover both rails coherently.

For many hybrid businesses, the winning design is less about one monolithic product and more about one investigation and governance layer that can ingest signals from multiple sources. If a vendor claims full hybrid coverage, ask them to demonstrate a complete cross-rail case from start to finish.

What should the first ninety days focus on

Keep the scope narrow enough to make the control real.

A good first phase usually focuses on:

- Highest-risk payment flows: channels and customer segments that create the most exposure

- Data completeness: making sure key transaction and customer fields arrive in the system

- Core rules: a smaller set of explainable scenarios that analysts can defend and tune

- Case handling discipline: queue ownership, review notes, closure standards, and escalation paths

Don't chase perfect coverage on day one. Chase reliable coverage in the places where a miss would hurt the business most.

If you're operating globally and touching both fiat and digital asset workflows, a platform like OneSafe is worth evaluating for the operational side of that equation. It helps companies manage multi-currency business accounts, payments, cards, and crypto-compatible workflows in one place, which makes it easier to reduce fragmentation before your monitoring program has to make sense of it.