Your vendor says the invoice was for $10,000, but their bank statement shows less. Your team checks the outgoing wire confirmation and sees a neat flat fee at initiation, so everyone assumes the bank made a mistake. Usually it didn't. You paid the visible fee. You didn't price the transfer's landed cost.

That's the part most startups miss. SWIFT is reliable, global, and familiar. It's also built on a chain of institutions that can each take a slice or widen the exchange rate in ways that barely show up in your dashboard. If you run finance or operations for a global startup, a DAO, or any business paying contractors, suppliers, or entities across borders, those “small” gaps add up fast.

The fix starts with treating international wires as a cost stack, not a line item. Once you do that, it gets much easier to choose the right payment path, reduce reconciliation headaches, and stop letting hidden FX spreads eat working capital. If you're reviewing broader cross-border payment options for global teams, this is the operational lens that matters most.

Table of Contents

- Start by reducing the payment chain

- Use fintech rails where banks stay vague

- When crypto rails make more sense

- Why did money still get deducted from my OUR transfer

- Can I know intermediary fees in advance

- How do I prove I sent the full amount

- When should I stop using SWIFT entirely

The Hidden Tax on Global Business

A common ops failure looks boring on the surface. Treasury sends a wire. AP marks the invoice paid. A few days later, the recipient says the amount arrived short, and now someone has to untangle whether the issue was the sender fee, an intermediary deduction, a receiving bank charge, or an exchange rate that moved against you.

That gap is a substantial tax on global business. Not tax in the legal sense, but an operational drain that shows up as lost cash, extra reconciliation work, and vendor friction. The dangerous part is that teams often measure the wrong number. They focus on the fee they approved at the start instead of the amount that ultimately lands in the beneficiary account.

According to Karbon Card's breakdown of SWIFT landed costs, the landed cost of a SWIFT transfer is often misread as a flat fee, even though intermediary banks can deduct $15 to $50 per hop, FX markups can add 1% to 5%, and the total can reach 1% to 4% or up to 6.49% globally. That same breakdown notes that up to three intermediary banks may take lifting fees from principal, which is why companies can still see reduced receivables even when they think they selected the “safe” instruction.

Practical rule: If your team only records the outgoing wire charge and not the shortfall at receipt, you're understating payment cost.

This matters more for startups than for incumbents. Large enterprises can absorb leakage and argue with relationship managers later. A startup paying global contractors, cloud vendors, legal counsel, and exchange counterparties needs cleaner settlement. Cash efficiency depends on knowing the difference between the invoice amount, the wire amount, and the delivered amount.

The Anatomy of a SWIFT Transfer Fee

SWIFT fees make more sense when you think about a package crossing borders. The courier you hired isn't always the only party handling the package. Other depots can touch it, customs can slow it, and the final local carrier can still add handling. The payment chain works the same way.

The broad benchmark is sobering. The PayAngel summary of the World Bank Remittance Prices Worldwide figure states that the global average cost of sending money through traditional SWIFT-based bank transfers is approximately 6.36% of principal on a standardized $200 transfer. It also breaks that cost into several layers: an initiation fee from the sending bank, correspondent lifting fees of $10 to $30 per hop across 2 to 4 intermediaries, and an FX spread of 0.5% to 2.0% at each conversion point.

What you see first

The easiest fee to understand is the one your bank discloses up front.

- Sending bank fee: This is the amount charged when you create the wire. Teams usually see this in online banking or on the payment confirmation.

- SWIFT message cost: In some bank pricing structures, the secure message itself is part of the charge stack rather than a separate customer-visible line.

- Internal approval friction: Not a bank fee, but still real. Every manual confirmation and exception path raises the operational cost of using wires.

This is why finance teams often think they understand swift transfer fees. The sending fee is visible, approved, and logged. It feels like the whole story.

It isn't.

What usually stays hidden

The more expensive parts tend to sit inside the routing path or the FX quote.

| Cost layer | What happens | Why teams miss it |

|---|---|---|

| Intermediary fees | Correspondent banks handle the payment in transit and can deduct charges from the principal | The route isn't always known at initiation |

| Receiving bank fees | The beneficiary's bank may charge to accept or process the incoming wire | The sender often never sees this in advance |

| FX spread | The bank converts at a rate worse than the mid-market benchmark | It's embedded in the rate, not shown as a separate fee |

A clean mental model helps. The sending bank fee is the label you pay for. Intermediary fees are the toll booths on the highway. The receiving fee is the unloading charge at the destination. The FX spread is the part where someone revalues the package while it's in transit.

Most finance teams negotiate the visible fee first. The bigger savings usually come from reducing hidden conversions and unnecessary routing steps.

When a payment moves in the same currency and through a direct corridor, cost tends to be easier to predict. Once the transfer crosses currencies, touches multiple banks, or lands in a market where your bank lacks direct reach, opacity rises quickly. That's why treasury should review not just the wire fee schedule, but also the routing path, currency pair, and who controls conversion.

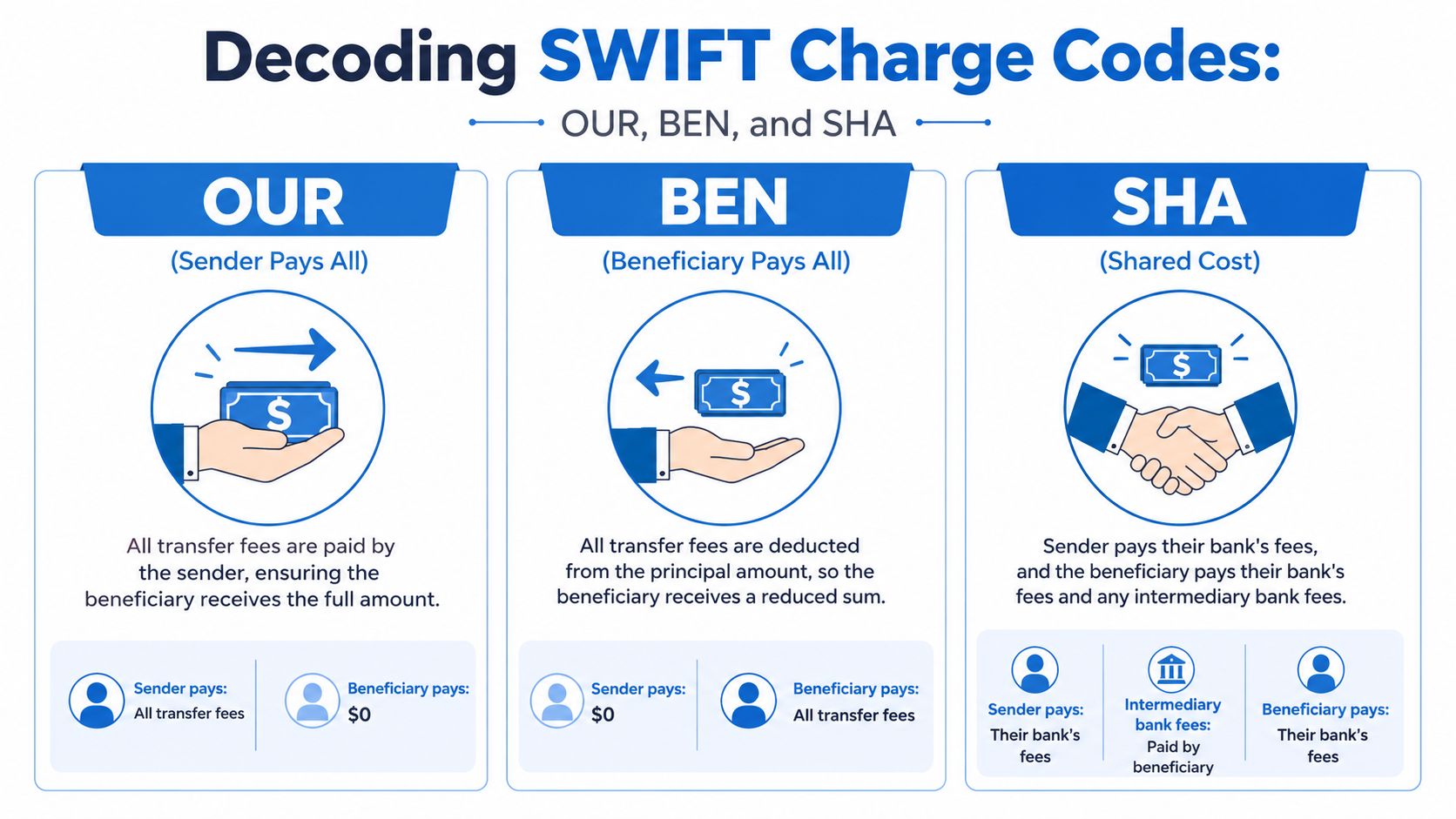

Decoding SWIFT Charge Codes OUR BEN and SHA

The charge code decides who absorbs the fee stack. It doesn't eliminate the stack. That distinction matters, because many payment disputes start when the sender thinks they bought certainty and the recipient still receives less than expected.

The Cambridge Currencies guide to SWIFT charges notes that SWIFT transfer fees are structurally compound and typically total 1% to 4% of transaction value. It also states that SHA is the industry standard, where the sender pays their own bank's fee while the beneficiary pays intermediary and receiving fees. Under BEN, the recipient absorbs all costs, which can materially reduce what lands and force treasury teams to calculate gross-up amounts if they want the vendor to net the intended figure.

What each code actually means in practice

A side-by-side view is more useful than the bank dropdown label.

OUR

You're instructing the payment so the recipient should get the full amount. In practice, teams use this for supplier payments, payroll-related wires, fund transfers between owned entities, or any invoice where being short creates friction.BEN

The beneficiary absorbs the cost chain. This is rarely the right choice for vendor relationships because it guarantees the amount received will be lower than the amount sent.SHA

The sender pays the originating bank fee, while downstream fees fall on the recipient side. This is common because it's the default in many bank flows and looks cheaper at initiation.

Here's the operational reality: SHA works best when both sides know the convention and expect minor variation. It works badly when your contract says a vendor must receive an exact amount.

Which code finance teams should pick

There isn't one universal answer. There is a sensible default by use case.

| Use case | Usually best choice | Reason |

|---|---|---|

| Supplier invoice with fixed net amount | OUR | Reduces settlement disputes |

| Internal transfer between group entities | OUR or SHA | Depends on how you allocate treasury costs |

| Low-stakes reimbursement | SHA | Simpler if exact receipt doesn't matter |

| Any payment where recipient bears all fees | BEN only if explicitly agreed | Otherwise it creates avoidable friction |

If the contract says the recipient must receive the full invoiced amount, treasury should treat SHA as a reconciliation risk, not a savings tactic.

One more caution. Even when teams choose OUR, they should still verify how their bank implements it and whether any downstream behavior can still affect final crediting. The code is an instruction, not a guarantee that every institution in the chain behaves the way your AP team expects.

The Biggest Hidden Cost FX Markups

Teams commonly obsess over the wire fee because it's easy to spot. The bigger leak is often the exchange rate.

For high-value treasury work, the EximPe analysis of SWIFT charges and FX markups makes the point plainly: the FX markup is often the primary cost driver, frequently larger than a flat outgoing wire fee. Its example is simple and useful. A 3% FX margin on a $100,000 transfer equals $3,000, which makes a flat $50 wire fee look negligible. The same source adds that choosing better FX execution providers can reduce total cost of funds by 2% to 3% per transaction.

Why flat fees distract teams

Flat fees trigger approval behavior because they're explicit. FX spreads don't.

A bank can quote a transfer in a way that feels reasonable because the visible fee is modest and the all-in debit still clears. Meanwhile, the conversion rate bakes in the actual margin. Unless someone on the team compares that rate with an independent benchmark, the spread passes through as if it were market reality.

That's why traders watch spread mechanics closely. If you want a simple primer on how spread behavior affects execution and why small pricing gaps matter, this guide on boost your trading profitability is worth reading. The same discipline applies to operational FX, even if your goal isn't trading profit but cleaner treasury execution.

How to audit an FX quote before you approve it

Use a repeatable process. Don't rely on intuition.

Capture the bank's quoted rate

Save the exact conversion rate offered at approval time.Check an independent benchmark

Compare it with a reliable market reference using a live business currency converter.Calculate the spread in money terms

Teams get fooled when they only look at percentages. Convert the difference into base currency cost.Decide whether the corridor justifies it

Some routes are structurally harder than others. That doesn't mean every markup is acceptable.

A treasury team that can explain the FX spread in dollars, not just basis points, makes better payment decisions.

A practical workflow helps here. Separate the payment decision from the FX decision. Ask two questions every time: “Do we need SWIFT for delivery?” and “Do we need this provider for conversion?” Banks like bundling those together because it hides comparison. Finance teams should unbundle them whenever possible.

For web3 companies, this point is even sharper. If your treasury already holds stablecoins or frequently moves between fiat and digital assets, an embedded bank FX spread can become the most expensive part of an otherwise modern payment stack.

Strategies to Reduce SWIFT Fees in 2026

The goal isn't to eliminate SWIFT in every case. It's to stop using it blindly when cheaper, cleaner rails exist for part or all of the flow.

The need for alternatives is obvious from the market-level picture. According to Topmost Labs' 2025 cross-border payments fee review, SWIFT-facilitated global cross-border payment volume reached $180 trillion in 2025, yet the average remittance fee remained 5.8%. That same review highlights corridor differences, with the US-to-India route at 1.5% while transfers to Africa average 9%, far above the G20 roadmap target of 3% by 2030.

Start by reducing the payment chain

The first lever is structural. Fewer institutions in the path usually means fewer surprises.

- Use local rails for local legs: If funds can enter or exit through systems like domestic bank transfer networks rather than crossing the whole distance by SWIFT, costs often become more transparent.

- Hold the payout currency ahead of time: Multi-currency treasury reduces forced conversions at the moment of payment.

- Route predictable invoices in batches: Fewer fragmented payments usually mean fewer chances to absorb repeated bank handling costs.

Many startups improve quickly once they stop thinking in terms of “international wire” as a single product and start rebuilding the path into origin funding, currency conversion, and local disbursement.

Use fintech rails where banks stay vague

Banks still tend to bundle fees, routing, and FX in a way that makes comparison difficult. Modern fintech stacks work better when they expose each moving part.

A stronger setup usually includes:

- Published payment pricing

- Visible FX pricing

- Multi-currency balances

- Approval controls for ops and treasury

- A way to choose between wire, local payout, and digital asset movement

That's also why finance teams increasingly compare bank wires against crypto-enabled treasury paths instead of assuming they serve separate use cases. If you want a concrete comparison of where traditional bank costs stack up against digital alternatives, this breakdown of Bank of America wire transfer fees vs crypto costs is a useful reference point.

The fastest cost reduction usually comes from forcing price visibility. Once the team can see fee type, FX rate, and delivery rail separately, waste becomes easier to remove.

A second operational change matters just as much. Don't let AP choose the rail by habit. Build a payment policy. Vendor invoices above a certain size should trigger an FX review. New corridors should trigger a payout-method review. Treasury-owned transfers should require a landed-cost estimate before approval.

A quick visual walkthrough helps if you're redesigning that process:

When crypto rails make more sense

Banks won't volunteer this, but some payments shouldn't touch SWIFT at all.

For web3 startups, DAOs, global contractor networks, and businesses already comfortable with stablecoin settlement, crypto rails can remove major sources of leakage:

| Payment challenge | Traditional path | Crypto-enabled alternative |

|---|---|---|

| Cross-border vendor settlement | Wire plus correspondent path plus FX spread | Stablecoin settlement, then local conversion if needed |

| Treasury rebalancing | Multi-bank transfers and slow reconciliation | Onchain transfer with faster internal visibility |

| Urgent contractor payout | Bank cutoffs and uncertain arrival amount | Digital asset settlement with clearer receipt confirmation |

This doesn't mean every recipient wants crypto. Many don't. But the operational model is powerful when the sender can settle in a digital dollar, convert near the endpoint, and avoid intermediary banks taking fees along the way. In practice, the best workflows often blend rails. Use fiat where regulation, counterparties, or accounting policy require it. Use crypto where it cuts path length, improves timing, or avoids avoidable FX spread.

The finance teams that manage this well don't ask whether crypto replaces banking. They ask a more useful question: which segment of this payment should use which rail?

SWIFT Fee FAQs for Global Businesses

Why did money still get deducted from my OUR transfer

Because OUR is an instruction, not a forensic audit of the routing chain. If the sending bank's implementation is narrow, or if another institution in the path handles the payment in a way that creates deductions or conversion effects, the recipient can still report a shortfall.

The practical fix is procedural. Save the payment confirmation, request the wire trace when the amount arrives short, and compare the expected currency and settlement path with what happened. If this recurs on the same corridor, stop treating it as an exception and change the payment method.

Can I know intermediary fees in advance

Often not with precision. That's one of the core weaknesses of legacy correspondent banking. The route can vary by corridor, beneficiary bank, currency, and the commercial relationships between institutions in the chain.

You can still improve predictability:

- Ask the bank if it has a direct corridor for that beneficiary bank and currency.

- Send in the destination currency only when the quoted FX is acceptable.

- Use providers with published fee logic rather than bespoke opaque pricing.

- Track actual landed amounts by corridor so your team builds its own operating data.

The internal record holds greater significance than often acknowledged. After a handful of payments, you'll know which routes are stable, which ones leak, and which vendors should be moved to a different rail.

How do I prove I sent the full amount

Use a packet, not a single screenshot. Finance should retain the invoice, payment instruction, bank confirmation, exchange rate used, and any wire reference or trace details. If the recipient disputes the amount, send all of it together.

A clean vendor-facing note usually includes:

- The instructed principal amount

- The charge code selected

- The payment date

- The currency sent

- The transaction reference

- Any note that downstream bank fees may affect receipt if applicable

That won't solve every dispute, but it does move the conversation from guesswork to evidence.

When should I stop using SWIFT entirely

Stop using it by default when the payment has one or more of these traits:

- The recipient needs exact settlement and prior wires have arrived short

- The corridor regularly triggers hidden FX pain

- The amount is large enough that conversion economics dominate

- The recipient can accept a local payout or digital asset workflow

- Your team spends more time reconciling wires than executing them

If a payment path creates repeated exceptions, it's no longer a finance process. It's a recurring operational bug.

SWIFT still has a place. It remains useful for certain banks, jurisdictions, and counterparties that require traditional rails. But it shouldn't be the reflex option for every international payment. Treasury should choose it because it's the best route for that payment, not because it's the oldest one on the menu.

If your team is managing global payouts, multi-currency balances, and crypto-to-fiat treasury flows, OneSafe is worth a look. It combines business accounts, cross-border payments, cards, and crypto-compatible workflows in one place, which makes it easier to see costs clearly and choose better rails before hidden wire fees eat into your cash.