Your finance lead closes the month and sees three different truths at once. Stripe shows sales on Friday. Your bank shows a smaller deposit on Tuesday. Your crypto wallet shows a conversion still in transit. None of those records are wrong, but none tells the full story on its own.

That gap is where founders get frustrated. You know money was earned. You can see it moving. But you can't cleanly answer a basic question: where should it sit in the books right now?

A clearing account solves that problem. Think of it as a financial waiting room. Transactions land there briefly while your team confirms what happened, matches records across systems, and moves each amount to its final account. That keeps your books usable even when payments settle in batches, processors deduct fees later, or crypto and fiat legs of the same transaction arrive at different times.

If your business operates across cards, wires, ACH, SWIFT, wallets, exchanges, and multiple entities, this matters more than most startup accounting guides admit. You don't need more dashboards. You need a disciplined way to handle timing gaps without muddying cash, revenue, liabilities, or retained earnings.

That discipline starts with the account structure itself. A good setup for banking rails and digital asset workflows makes reconciliation much easier, especially when you're building around a business account setup for fiat and crypto integration.

Table of Contents

- Introduction Why Your Business Needs a Financial Waiting Room

- The plain English definition

- Why accountants bother with this extra step

- Where traditional guidance breaks down

- Governance rules that matter in mixed fiat and crypto operations

Introduction Why Your Business Needs a Financial Waiting Room

Most founders first run into clearing accounts during a mismatch that looks small but creates real confusion. Sales are booked today. Cash arrives later. Fees come out separately. A refund posts in one system before it appears in another. In crypto, token movement can show up before the fiat conversion reaches the bank.

A clearing account gives those in-between transactions a temporary home. HighRadius defines a clearing account as a temporary general ledger account that holds transactions until they can be accurately matched and reconciled before permanent recording, and notes that it is often called a wash account because it should return to zero by the end of the reconciliation period (HighRadius explanation of clearing accounts).

That zero-balance idea is the part many non-accountants miss. The point isn't to create another bucket of money. The point is to prevent in-transit items from distorting your books while they're still being validated.

Practical rule: If money is moving but its final classification isn't confirmed yet, it probably belongs in a clearing account before it belongs anywhere else.

This matters more in a fast-moving business than in a tidy textbook example. Payment processors settle on their own schedule. Payroll providers pull cash on different dates than pay dates. Exchanges and banks don't always line up cleanly. Without a clearing account, teams start forcing temporary transactions into permanent accounts, and that usually creates month-end cleanup work, unexplained balances, or both.

What Is a Clearing Account and Why Does It Exist

The plain English definition

A clearing account is a temporary holding account inside the general ledger. It catches transactions that are real, expected, and identifiable, but not fully settled or fully matched yet. You know the transaction belongs to the business. You just don't want to post it permanently until the rest of the records catch up.

The staging-area analogy works well here. In logistics, a package may arrive at a sorting hub before it reaches its destination. That hub isn't the final address. It's the place where the shipment is checked, sorted, and routed correctly. A clearing account does the same thing for money and accounting entries.

The phrase many accountants use is wash account. The reason is simple. The account should end the cycle at zero after every item has been transferred to its proper permanent account.

Why accountants bother with this extra step

If you skip the clearing step, you can create misleading balances. Cash might look too high or too low. Revenue may be recognized against deposits that haven't settled. Liabilities can end up mixed with operating expenses. The books still "have numbers," but they stop reflecting operational reality.

Institutional accounting guidance treats clearing accounts as mandatory control accounts that must be supported by entries in the general ledger and subsidiary records, and it also states that clearing accounts do not belong on the balance sheet permanently because their purpose is to preserve data integrity until the books are confirmed (Indiana State Board of Accounts guidance).

That sounds formal, but the practical lesson is straightforward:

- Known transaction, not fully matched: Use a clearing account.

- Temporary timing difference: Use a clearing account.

- Final home not yet ready: Use a clearing account.

- Goal at close: Clear it to zero.

A clearing account isn't a workaround for messy bookkeeping. It's the control that keeps temporary timing issues from becoming permanent accounting errors.

Common Types of Clearing Accounts

Four common versions you will actually use

Different businesses use different clearing accounts, but four show up constantly.

| Account Type | Primary Use Case | Example Transaction |

|---|---|---|

| Payroll clearing | Hold payroll amounts before wages, taxes, and related payments fully post | Payroll run is recorded before bank withdrawals complete |

| Accounts receivable clearing | Bridge customer payments received through processors before bank settlement | Card sales batch from a payment gateway |

| Intercompany clearing | Track amounts moving between related entities until both sides post correctly | Parent company pays a vendor on behalf of a subsidiary |

| Income summary clearing | Aggregate period revenue and expenses before closing to retained earnings | Year-end or month-end close transfer |

A payroll clearing account helps when the payroll journal and the bank movement don't occur on the same day. A receivables clearing account is useful when a processor groups many sales into one deposit. Intercompany clearing keeps one entity from carrying a vague "due to someone" balance forever. And the income summary account acts as a classic clearing mechanism that gathers revenue and expenses before the net amount moves to retained earnings at period close, as noted in the earlier institutional guidance.

A simple transaction flow

Take a common card-sales batch:

- Your store records customer sales today.

- Instead of posting directly to the operating bank account, you post the amount due from the processor to a clearing account.

- The processor deposits the net amount later.

- Fees and deductions are booked separately.

- The clearing account returns to zero once the gross amount is fully matched.

That flow solves a basic mismatch. The sales event and the cash event are related, but they aren't identical and they don't happen at the same moment.

Founders often ask whether they need multiple clearing accounts. In practice, yes, if the workflows are materially different. Payroll, processor settlements, and intercompany transfers usually deserve separate accounts because each has its own owner, reconciliation cadence, and failure pattern.

The Accounting Behind Clearing Accounts A Practical Example

A payment processor batch from start to finish

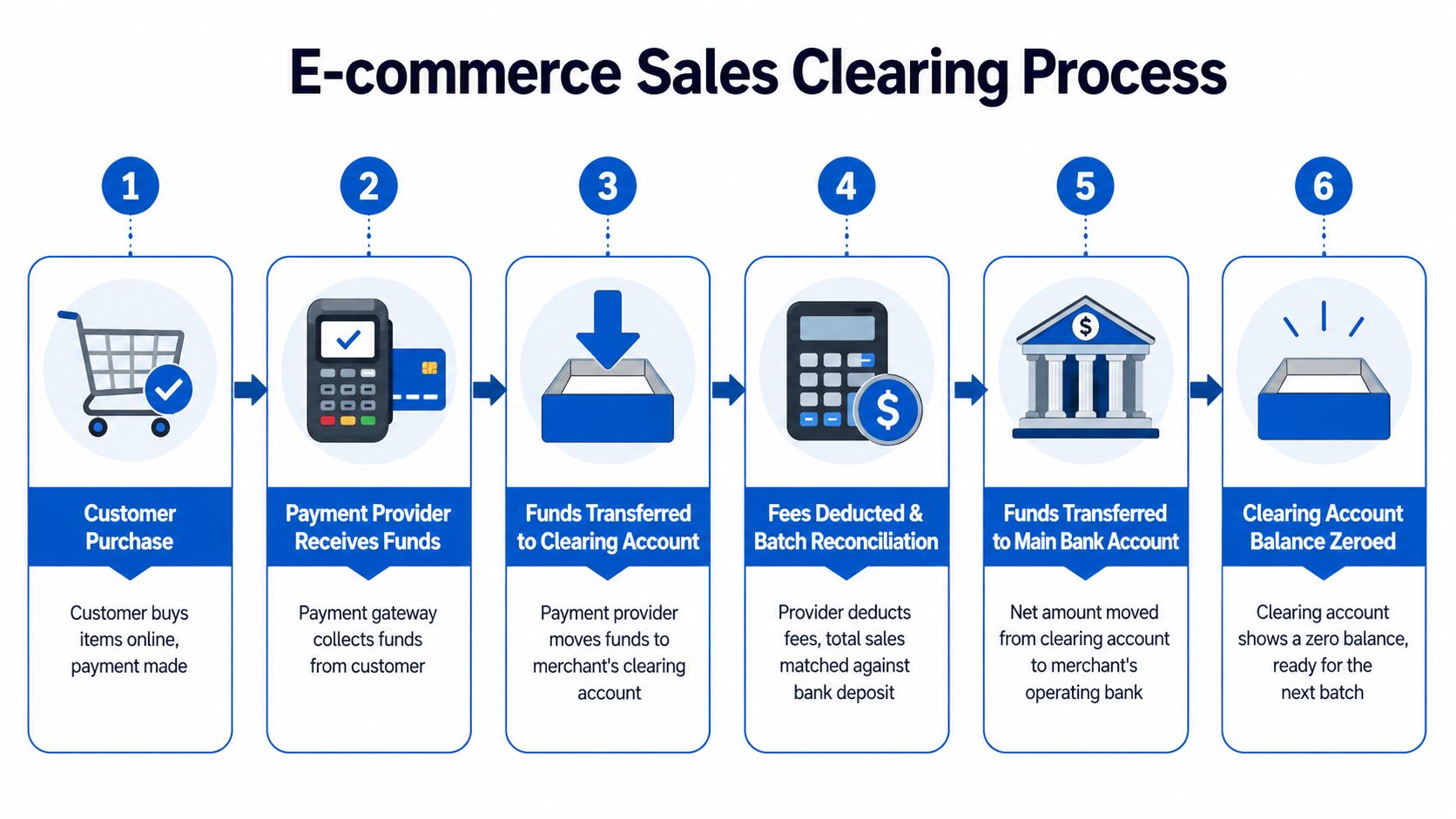

Let's make this concrete with an e-commerce example. Your store makes sales through a payment provider on Monday. The provider sends a bank deposit later and deducts its fee before cash arrives.

On the day of sale, the clean entry is:

- Debit payment processor clearing

- Credit sales revenue

That records the business event when it happens. You earned the revenue, but you haven't received settled bank cash yet.

When the provider later sends the deposit, the next entries usually look like this conceptually:

- Debit bank

- Debit payment processing fees

- Credit payment processor clearing

Now the clearing account should wash out. It held the gross amount temporarily, then released it into the two final destinations that matter: cash received and fee expense.

If you want a quick refresher on how debits and credits fit together before building these entries, download this accounting resource. It's a useful one-page reference for operators who don't live in the general ledger every day.

Why this works better than posting straight to cash

Posting straight from sales to bank sounds simpler, but it breaks as soon as the deposit date, net deposit amount, or fee structure differs from the original sale. That's exactly what processors, marketplaces, and cross-border rails tend to do.

A clearing account keeps each part of the event in the right place:

- Revenue stays tied to the sale date

- Cash stays tied to the actual deposit

- Fees stay visible instead of disappearing into net settlement

- Reconciliation becomes a matching exercise, not a guessing exercise

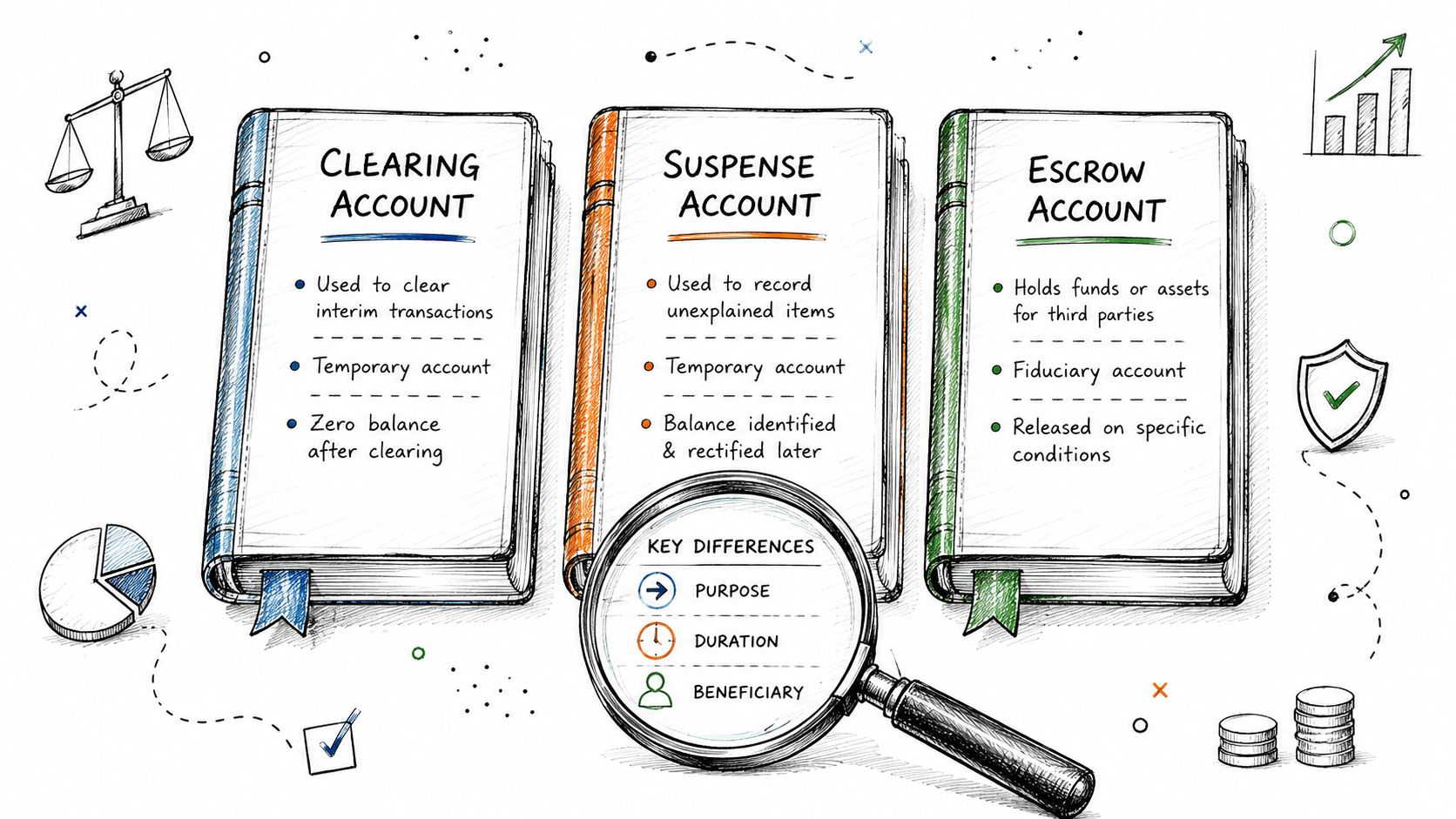

This is also where people confuse clearing with suspense or escrow. They aren't interchangeable. A clearing account is for a known transaction moving through a timing gap. A suspense account is for something unresolved that needs investigation. Escrow is usually a contractual holding arrangement involving funds restricted for a specific purpose.

If the processor deposit doesn't tie out and the clearing account doesn't return to zero, don't leave the residual there indefinitely. That leftover amount has changed categories. It is no longer a normal in-transit item. It has become an exception that needs investigation, which belongs in the next discussion.

Clearing Accounts vs Suspense and Escrow Accounts

People mix up these three accounts because all of them sound temporary. Their jobs are different.

Three temporary accounts with very different jobs

A clearing account is for a transaction you understand. You know what the money relates to. You're waiting for settlement, matching, or final posting.

A suspense account is for a transaction you don't fully understand yet. Something is missing, mismatched, or failed. The unresolved balance sits there while your team investigates.

An escrow account is different again. Funds are held for a contractual or legal condition, usually by a third party or under restricted terms. That's not an accounting timing tool. It's part of the deal structure.

For a visual explainer, this short video gives a useful conceptual comparison before you build your own policies:

What to do when clearing fails

This is the workflow many startup teams miss. If a clearing account doesn't hit zero, you don't just "wait one more month" and hope the difference disappears. Gaviti notes that the remaining balance should be moved to a suspense account for investigation when a clearing account fails to clear, because leaving it uncleared creates compliance risk (Gaviti glossary on clearing accounts).

That matters in global and web3 finance because delays don't always mean simple banking lag. The issue could be a failed vendor payment, an invoice mismatch, an FX variance, or a blockchain transfer that never reached the expected final state.

Known and pending belongs in clearing. Unknown and broken belongs in suspense.

Escrow belongs in a different conversation entirely. If you're managing restricted funds, tenant deposits, M&A holds, or deal-based releases, your accounting treatment should reflect the legal arrangement, not the convenience of temporary bookkeeping.

Clearing Accounts in Modern Finance Web3 and OneSafe

Where traditional guidance breaks down

Basic articles on what are clearing accounts usually assume a simple fiat world. Card processor in. Bank deposit out. Done. That model breaks down when your treasury moves between wallets, exchanges, stablecoins, bank accounts, and global payment rails.

For web3 firms, guidance gets especially weak around classification. Atlar highlights a real ambiguity: when a clearing account holds in-transit crypto, it's not always obvious whether that balance should be treated as a current asset or liability during the timing gap, and that can distort financial statements when standard guidance assumes fiat-only rails (Atlar on clearing account ambiguity in web3 contexts).

That isn't just a technical accounting debate. It's an operating problem. A startup may convert USDC to fiat, send a vendor wire, and record invoice settlement across systems that update on different clocks. If the team posts too early, liquidity can look stronger or weaker than reality. If the team waits too long, month-end reporting becomes stale and operational decisions suffer.

Governance rules that matter in mixed fiat and crypto operations

Discipline, rather than software brand names, is paramount. In mixed fiat and crypto environments, finance teams should treat clearing accounts as active control points, not passive buckets.

Use rules like these:

- Separate flows by purpose: Keep processor settlements, payroll, exchange transfers, and intercompany activity in different clearing accounts.

- Match by evidence, not assumption: Reconcile against processor reports, bank records, wallet transactions, and approved invoices.

- Escalate non-zero balances quickly: If an item stops behaving like a timing difference, investigate it as an exception.

- Document classification logic: In-transit crypto and fiat legs should have a written accounting position approved by finance leadership and your external advisors.

Teams that also manage restricted or trust-like holdings should understand adjacent tooling as well. If your operation includes governed fund segregation, it helps to streamline financial management for CEFs with software built for escrow-style controls rather than trying to force those balances through ordinary clearing workflows.

For companies operating across token rails and banking rails, a platform view helps reduce blind spots. A single environment for payments, cards, conversions, and account visibility is easier to control than five disconnected systems. That's one reason operators looking at web3 treasury infrastructure often prioritize platforms built for global business banking for web3 companies.

Controls and Best Practices for Clearing Accounts

A practical operating checklist

A clearing account should never become a parking lot for old exceptions. Institutional guidance is clear that clearing accounts are mandatory control accounts and don't belong on the balance sheet permanently because their only purpose is preserving data integrity until the books are confirmed, as described in the earlier government accounting guidance.

The practical checklist is short, but it needs to be enforced:

- Assign one owner: Every clearing account needs a named person responsible for review and resolution.

- Reconcile on a fixed cadence: Daily is common for high-volume payment flows. Weekly may work for lower-volume accounts.

- Define the exit rule: Teams should know exactly what evidence allows an item to move from clearing to its final account.

- Move broken items out fast: If the balance stops being a routine timing issue, reclassify and investigate.

- Keep support attached: Processor reports, payroll registers, wire confirmations, wallet records, and approvals should sit with the reconciliation.

Security controls matter too. If the same environment handles treasury movement and ledger support, weak permissions can turn a reconciliation problem into a fraud problem. That's why finance leaders often pair accounting controls with broader system reviews, including resources on fast SaaS pentesting results when evaluating tools that store payment and treasury data.

A final habit worth adopting is policy documentation. If your team handles crypto conversions, payout approvals, and multi-entity treasury movement, write the workflow down. This is especially important for teams refining best practices for crypto treasury management, where timing gaps and authorization controls need to be explicit.

If your business moves money across fiat accounts, crypto rails, cards, payroll, and global vendors, OneSafe can help bring those flows into one operating environment. Explore OneSafe to see how teams manage multi-currency accounts, payments, cards, and crypto-compatible workflows with tighter visibility and control.