You're usually not thinking about a currency transaction report form until the day cash hits your business. A client wants to settle an invoice with physical currency. A retail operation has a large same-day cash deposit. A crypto-native company converts digital assets and someone asks whether the cash side triggers Bank Secrecy Act reporting. That's when teams realize CTR rules are old, specific, and still very relevant.

For startup CFOs, finance leads, and DAO operators, the hard part isn't the existence of the rule. It's knowing exactly when it applies, who counts as the transactor, and how to build a process that won't fall apart when cash shows up through an unusual channel.

Table of Contents

- The threshold turns on cash, identity, and timing

- What counts as reportable currency and what does not

- Scenarios that matter for startups and web3 firms

- Where teams should slow down

- Gather the file before you open the form

- Complete the parties carefully

- Enter the transaction details precisely

- Watch the problem fields

- What good completion looks like

- The deadline is short, and the clock starts fast

- The mistakes that create exam problems

- Recordkeeping should answer the examiner's next question

- A control model that works in practice

- Does foreign currency count for a CTR

- Can you get in trouble for filing a CTR when you didn't need one

- What is an exempt person and why is it risky

- What is structuring

- Does crypto conversion itself trigger a CTR

- What should a first-time filer do internally before submitting

What Is a Currency Transaction Report and Why It Matters

A startup CFO closes a legitimate enterprise sale, then learns the customer wants to settle part of the invoice in cash before the books close. A DAO-adjacent operating team converts crypto to fiat for an in-person vendor payment, and someone suggests using cash to speed things up. In both cases, the commercial purpose may be clean, but the cash handling creates a separate compliance question. That is where a Currency Transaction Report, or CTR, enters the picture.

A CTR is a federal reporting requirement for certain currency transactions. The filing is made on FinCEN Form 112, and its purpose is straightforward. It gives regulators a standardized record of large cash activity so they can trace the movement of physical currency through the financial system.

Why the government tracks large cash movements

Physical currency remains a focus for AML controls because it can move with less visibility than bank wires, card payments, or many digital transfers. A CTR captures who conducted the transaction, who benefited from it, and the core facts of the cash movement. For investigators, that record is useful even when the payment itself is lawful.

This is routine reporting, not a fraud finding and not a statement that anyone did something improper.

That distinction is where teams often go wrong. CTRs are different from Suspicious Activity Reports. A SAR depends on facts that suggest unusual or suspicious conduct. A CTR is tied to reportable cash activity under the rule, whether the transaction looks ordinary or not.

For modern businesses, including crypto companies and web3 organizations, this point gets missed. Treasury teams may assume wallet activity, exchange transfers, or stablecoin settlements sit outside the old cash-reporting framework. Often they do, until physical currency enters the chain. Once a crypto-to-fiat conversion ends in actual cash received, paid out, deposited, or withdrawn, traditional CTR analysis can become relevant fast.

Why operators get tripped up

The failure point is usually internal coordination, not legal complexity. Sales accepts funds. Operations logs the payment. Finance books revenue. Compliance is told later, or not at all. By then, nobody is sure who acted on whose behalf, whether same-day transactions should be grouped, or who was supposed to make the filing decision.

That risk is higher in organizations with split ownership. Global companies may have U.S. entities, overseas ops teams, and local finance staff all touching the same customer relationship. DAOs and web3 groups add another layer. Signers, delegates, foundation staff, and service companies may each control one part of the payment flow, while no one owns the reporting analysis from start to finish.

Clear operating rules reduce missed filings. If your team is formalizing how legal obligations become day-to-day procedures, Smart Receipts on business rules offers a useful framing. If finance, treasury, and compliance teams need consistent terminology for payments and reporting, a shared banking and compliance glossary reduces internal confusion.

Identifying When You Must File a CTR

A founder closes a large cash sale in the morning. That afternoon, the same customer sends a colleague to make another cash payment at a different location. Finance books two ordinary receipts. Compliance sees one reportable event.

A CTR is required when a single cash transaction, or multiple cash transactions that must be aggregated, exceed $10,000 during one business day. The rule applies when the institution knows, or has reason to know, that the transactions were conducted by or on behalf of the same person. For startups, global finance teams, and DAO-linked operating entities, that knowledge question is usually where mistakes start.

The threshold turns on cash, identity, and timing

One over-the-counter cash deposit above the threshold is straightforward. Harder cases involve split payments, multiple branches, couriers, employees paying on behalf of a business, or treasury staff treating related activity as separate because it arrived through different operational channels.

Use this working test:

- Confirm that physical currency is involved. Start with paper money and coin, whether in U.S. or foreign currency.

- Identify the actual actor. Check who conducted the transaction and who benefited from it.

- Review activity across the full business day. The focus is on same-day transactions.

- Aggregate related cash events. Separate receipts can create one CTR filing obligation.

Two below-threshold cash payments from the same client on the same day are the classic miss. I see this often in businesses with fragmented intake. One office logs a customer payment. Another office logs a second payment from the same customer's employee or representative. Nobody combines them, so nobody files.

If your records do not show who acted for whom, your aggregation analysis breaks before the filing process starts.

What counts as reportable currency and what does not

Confusion often arises from mixing cash rules with broader payment activity. CTR analysis is narrow. It covers currency transactions, not every transfer of value.

| Transaction Type | Counts Toward CTR Threshold? |

|---|---|

| Cash deposit in U.S. currency | Yes |

| Cash withdrawal in U.S. currency | Yes |

| Currency exchange using physical cash | Yes |

| Loan payment made with physical cash | Yes |

| Purchase of monetary instruments with physical cash | Yes |

| Deposit of foreign paper currency or coin | Yes |

| Wire transfer | No |

| ACH transfer | No |

| Credit card payment | No |

| Debit card payment | No |

| Crypto-to-crypto transfer | No |

| On-chain wallet transfer without physical cash | No |

That distinction is easy to state and easy to mishandle. A large wire from an exchange is not a CTR event. A cash withdrawal that follows an off-ramp may be. The reporting question is tied to the physical currency transaction itself.

Scenarios that matter for startups and web3 firms

Modern operators need to apply old cash-reporting rules to newer payment flows without forcing every crypto transaction into a CTR framework.

- Customer pays an invoice with physical cash: Reportability depends on the amount and whether same-day related payments must be combined.

- Exchange conversion followed by cash pickup or cash withdrawal: The electronic conversion step and the later cash event should be analyzed separately. The CTR question attaches to the cash event.

- Foreign customer pays in local banknotes: Foreign currency can still count if it is legal tender and part of a reportable same-day currency total.

- DAO-related operations using nominees or service providers: If a signer, foundation employee, or local administrator conducts a cash transaction for the operating entity, review the on-behalf-of relationship instead of stopping at the individual's name.

- Crypto settlement followed only by bank wire: No CTR issue arises from the wire itself, though other monitoring obligations may still apply.

This is a real pressure point for DAO structures and global groups. Cash may be handled by a local affiliate, an outsourced operator, or a foundation support team while the economic activity belongs to another entity. If no one is responsible for connecting those roles, the organization can miss aggregation that looks obvious in hindsight.

Where teams should slow down

The usual failure is not the threshold. It is internal classification. Accounting records “payment received.” Treasury records “fiat settlement.” Operations records “customer cash intake.” CTR analysis needs a cleaner answer. Was it currency, who was it for, and what else happened that same day?

For first-time filers, I recommend mapping payment channels before reviewing any single transaction. Separate true cash activity from wires, card payments, exchange transfers, and on-chain movements. Then assign one person or function to make the aggregation call across entities, desks, and locations. Without that control, the filing decision becomes guesswork.

A Practical Guide to Completing the CTR Form

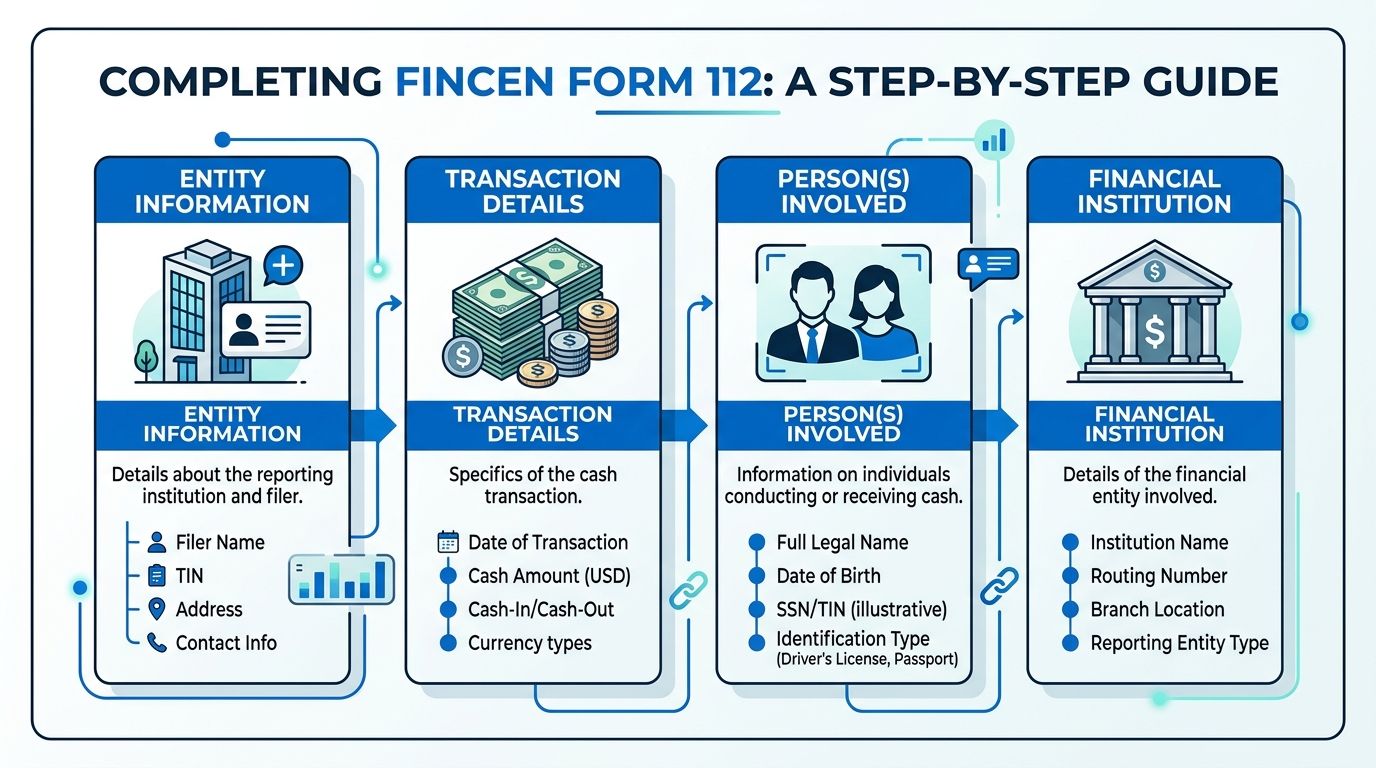

A startup CFO closes a cash sale on Friday afternoon. A DAO operations lead sends a local representative to handle a fiat deposit tied to a crypto off-ramp. By Monday, the hard part is no longer deciding whether the activity was reportable. The hard part is getting Form 112 right the first time.

The currency transaction report form used in practice is FinCEN Form 112. Treat it as a documented compliance decision, not a data-entry chore. Filing errors are usually caused by incomplete identity records, weak support for who acted on whose behalf, or transaction details that blur cash activity with wires, exchange transfers, or other non-currency movements.

Gather the file before you open the form

Build the file first. Then complete the CTR.

That means pulling together the transaction record, teller or cashier notes, identification reviewed at the time of the transaction, and any internal documentation showing the relationship between the person who handled the cash and the business or entity behind it. Teams with mixed fiat and digital-asset flows should also separate any crypto settlement records from the CTR file so staff do not accidentally include non-cash activity in the reported amount. For treasury teams refining that control environment, these crypto treasury management practices for business operations help keep payment channels and approval trails distinct.

For startups, foundations, and DAO-related operating entities, this step often determines whether the filing will hold up later. The form expects an identifiable human transactor. If a finance lead, signer, foundation staff member, or local administrator acted for an entity, your records should show that clearly and contemporaneously.

Use this checklist before anyone starts entering fields:

- Who physically conducted the transaction

- Who owned or controlled the funds

- What currency was received or paid out

- Which same-day cash events were aggregated

- Which legal entity, branch, or business unit handled the activity

Complete the parties carefully

The party fields are where first-time filers lose precision. If an individual acted for a company, foundation, or operating subsidiary, record the person as the transactor and preserve the entity relationship accurately in the form and supporting file. Do not merge the human being and the business into a single identity.

That point matters even more for web3 structures. A DAO may make decisions on-chain, but cash activity is still handled by people acting through a wrapper entity, foundation, service company, or authorized signer arrangement. The CTR process still asks the old-fashioned question regulators care about. Who handled the cash, and for whom?

I tell operators to assume an examiner will review the file with no background on the organization chart. If the relationship is not obvious from your documentation, fix that before filing.

Enter the transaction details precisely

The transaction section creates trouble when staff copy the full commercial story into a form that only captures the currency piece. The CTR is about reportable cash activity. It is not a summary of the customer relationship, the invoice, or the crypto leg of a broader transaction.

That distinction is easy to miss in global businesses and crypto-linked operations. A single client event may involve digital assets, a fiat conversion, internal treasury movement, and a cash deposit or withdrawal. Only the currency portion belongs in the CTR amount fields. If the cash activity was connected to a crypto-to-fiat conversion, document that context internally, but keep the reported transaction details focused on the actual currency handled.

This video gives a useful visual walkthrough of the filing workflow:

Watch the problem fields

Certain fields create repeat errors because they look simple.

- Amounts in and out: Record the cash movement cleanly. Do not combine it with wires, ACH, card payments, exchange transfers, or on-chain transfers.

- Foreign currency handling: Preserve the original currency details in your internal records and make sure the form entry matches the institution's transaction documentation.

- Government-issued identification: Use the document reviewed when the transaction was conducted.

- Business relationship notes: Keep enough internal support to explain the on-behalf-of relationship, even if every detail does not appear on the filed form.

Good record discipline also matters here. Small finance teams that need a cleaner documentation process can learn financial organization from Steingard.

What good completion looks like

A defensible CTR file lets a second reviewer answer two questions quickly. Why was the filing required, and who acted for whom? If those answers depend on tribal knowledge, the file is weak.

Strong CTR completion is plain, consistent, and easy to reconstruct. The amount ties to actual cash. The transactor is identifiable. The business or entity relationship is documented. The aggregation decision can be explained without guesswork. That is the standard startups and DAO operators should aim for, especially when cash activity sits beside crypto operations and cross-border entity structures.

Filing Deadlines Recordkeeping and Common Mistakes

A startup CFO closes a large cash deposit on Friday, assumes the bank will sort out the reporting, and moves on to payroll. A DAO operations lead sends a team member to handle a cash-heavy vendor payment after converting crypto to fiat, but no one documents who acted for which entity. Those are the situations that create avoidable CTR problems. The filing itself is only one part of the job. Actual exposure comes from late reporting, weak records, and poor coordination between operations, finance, and compliance.

Regulators regularly focus on two failures. Firms miss the filing window, and they fail to aggregate related cash activity across offices, business lines, or operating teams. The FDIC addresses both points in its CTR and exemption review guidance.

The deadline is short, and the clock starts fast

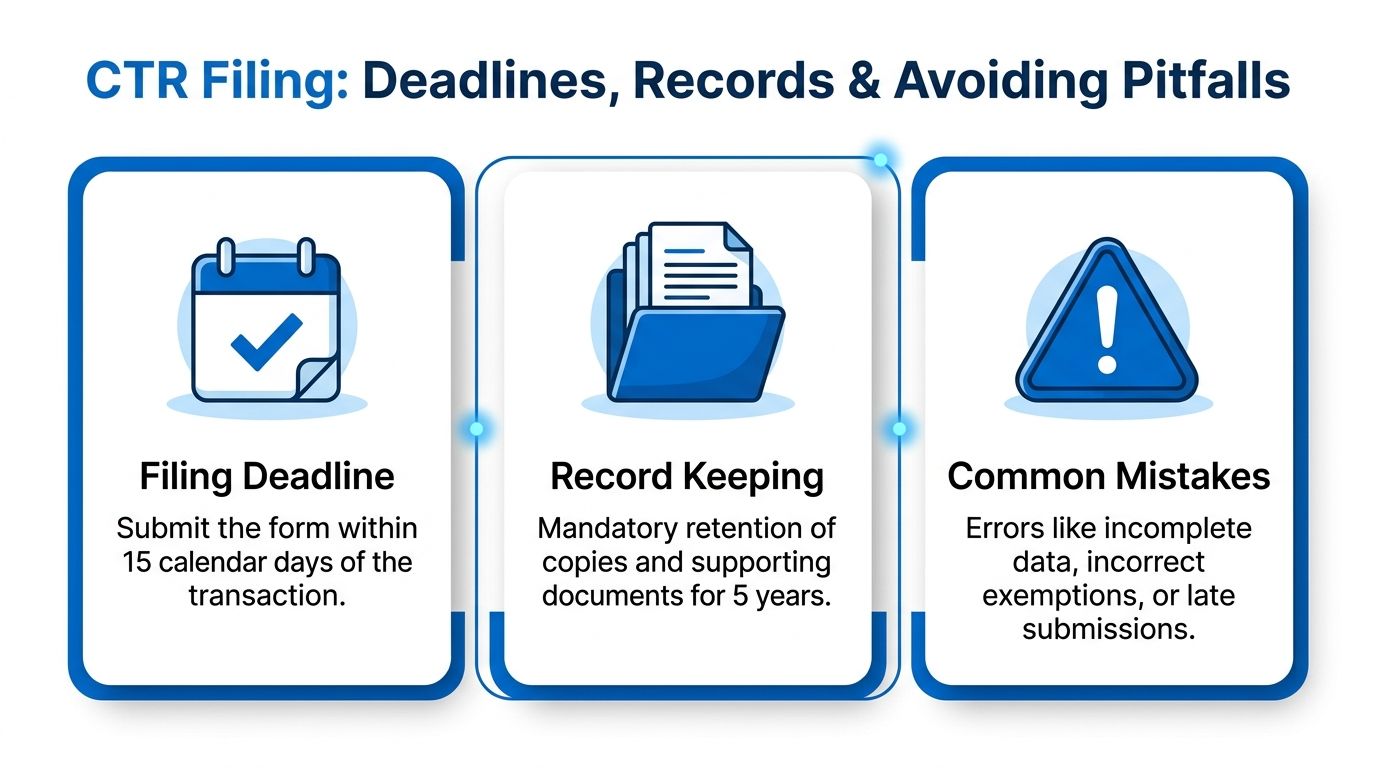

A CTR generally must be filed within 15 calendar days of the reportable transaction, and institutions are expected to retain the filed report and related support for five years, as noted earlier in this guide. In practice, that means the compliance clock starts when the cash transaction happens, not when someone on the finance team finally reviews the day's activity.

Weekend and holiday timing can affect internal handling, but that should not drive your process. Strong teams treat the cash event itself as the trigger. They log it immediately, assign ownership the same day, and clear open questions while the people involved still remember what happened.

That matters even more for businesses that move between crypto and fiat. A treasury team may be watching wallets, exchange accounts, and bank balances, while the reportable event sits in a physical cash transaction handled offline. If those workflows are separate, deadlines get missed.

The mistakes that create exam problems

The recurring errors are operational, not theoretical.

- Aggregation breaks down across locations or teams: One branch, office, or operating unit sees only part of the day's cash activity and no one combines the full picture.

- The on-behalf-of relationship is unclear: A signer, employee, runner, foundation officer, or service provider handles the cash, but the underlying entity relationship is not documented well enough to explain the filing.

- Exemption treatment is applied too casually: Teams assume a customer or counterparty is exempt without keeping the support needed to defend that position.

- The filing is late: Staff identify the issue but treat the deadline like an internal service target instead of a legal requirement.

- Records sit in separate systems: Cash logs, ID records, treasury approvals, and entity documentation live in different tools, so reviewers cannot reconstruct the transaction cleanly.

A late CTR is still a violation. An on-time CTR built on bad aggregation can create the same kind of scrutiny.

Recordkeeping should answer the examiner's next question

Keep the submitted form, but do not stop there. A defensible file also includes the transaction record, internal escalation notes, documentation showing who conducted the transaction, and support for why the activity was aggregated or treated as reportable. For a web3 company or DAO-linked structure, the file should also show which legal entity was involved and who had authority to act for it outside the digital realm.

Smaller teams frequently encounter difficulties with their financial operations. The bank account may sit with one entity, treasury decisions may come from another group, and the person handling the cash may be a contractor or local operator. If that chain is not documented at the time of the transaction, it becomes much harder to explain later.

If your company needs to tighten documentation habits generally, especially across small finance teams, this guide to learn financial organization from Steingard is a practical companion for building more disciplined record retention. For crypto-native finance teams trying to align cash controls with broader treasury processes, these best practices for crypto treasury management are useful for building audit trails, approval rules, and clear ownership.

A control model that works in practice

The cleanest setup splits responsibility across the people closest to the risk.

| Control Area | Best Owner |

|---|---|

| Cash intake classification | Operations or cashier function |

| Same-day aggregation review | Finance or BSA/AML reviewer |

| Identity and behalf-of verification | Compliance or designated approver |

| Final e-filing and retention | Compliance operations |

This structure reflects how CTR failures happen. Intake staff see the cash first. Finance sees patterns across the day. Compliance checks whether the identified person, entity, and filing basis hold together. If one person is expected to do all of it, errors stay hidden until an audit, a bank review, or a regulatory exam.

CTR Nuances for Crypto DAOs and Global Business

Crypto operators often assume CTR rules are about legacy banking branches and cash-heavy local businesses. That's too narrow. If your organization touches physical currency after a crypto off-ramp, or if a banking partner handles a reportable cash event connected to your operations, CTR logic can become relevant very quickly.

The key distinction is simple. Crypto-to-crypto activity isn't a CTR event by itself. A CTR becomes relevant when the transaction involves physical currency, and that matters for some exchange withdrawals, cash-intensive counterparties, and hybrid treasury operations.

DAO operations create identity friction

Traditional CTR systems expect a person and, where relevant, an entity relationship. DAOs complicate that because operational control may be distributed while real-world cash handling is carried out by a signer, foundation officer, service provider, or operations lead.

That means the compliance question isn't “Can a DAO file?” The practical question is “Who is the identifiable human transactor, and what legal entity or operating structure are they acting for?” If your DAO already uses a formal banking or treasury setup, your records should answer that before any cash event occurs.

Global businesses need currency discipline

Foreign currency adds another layer. Physical foreign notes and coins can still fall inside CTR reporting logic when they're legal tender and part of the cash transaction being handled. Multinational teams often get this wrong because they document the commercial invoice well but don't preserve enough detail about the actual cash instrument received.

A global operator should maintain clean separation among:

- On-chain transfers

- Bank wires and ACH

- Exchange conversion records

- Physical cash transactions

Those are different rails with different reporting consequences. Mixing them in one ledger narrative creates confusion during reviews.

Strong compliance for web3 finance usually looks boring. Named signers, clear entity records, consistent channel tagging, and auditable transaction trails solve more CTR problems than clever legal theories do.

If your organization is formalizing treasury operations for decentralized structures, it helps to review banking setups designed for financial services for DAOs so the legal entity, signer, and payment-rail relationships are documented before an unusual cash event ever happens.

Frequently Asked Questions on CTR Filings

Does foreign currency count for a CTR

Yes, if it's physical coin or paper money that is legal tender and part of a reportable currency transaction. The practical issue is documentation. Your records should clearly show what was received, by whom, and how it fit into the reportable cash event.

Can you get in trouble for filing a CTR when you didn't need one

Over-filing can create noise and internal inefficiency, so it isn't something to do casually. But from a risk standpoint, under-reporting is usually the more serious problem. If the facts are close and your documentation supports a reasonable decision, teams generally prefer to escalate and review rather than ignore a potential filing obligation.

What is an exempt person and why is it risky

Some customers can qualify for exemption treatment, but teams often create avoidable exposure through this. Exemptions require the right criteria and strong supporting documentation. A bad system setting or a stale customer designation can lead to missed filings that are much harder to defend than routine CTR submissions.

What is structuring

Structuring is the intentional breaking up of transactions to avoid the reporting threshold. It's not a paperwork issue. It's a criminal issue. If a customer tries to split cash payments or asks your team how to stay below the line, that should be treated as a serious escalation point.

Does crypto conversion itself trigger a CTR

Not by itself. The CTR question turns on physical currency. If value moves from crypto to fiat electronically and never becomes a physical cash transaction, you're dealing with other compliance frameworks, not CTR cash reporting. If the flow ends in reportable physical cash, then the CTR analysis becomes relevant.

What should a first-time filer do internally before submitting

Use a short internal review:

- Confirm the channel: Was this physical currency, not a wire or ACH?

- Check the day's activity: Did related cash events aggregate above the threshold?

- Identify the human actor: Who conducted the transaction?

- Tie that person to the entity: Who were they acting for?

- Save the support file: Keep the documents that explain your decision.

A first-time CTR filing usually goes smoothly when the business has already mapped payment channels, ownership of the review, and record retention. It becomes painful when those questions are answered after the cash has already moved.

If your business operates across fiat and crypto rails, OneSafe can help bring those workflows into one place. OneSafe supports global business accounts, payments, cards, and crypto-compatible treasury operations, which makes it easier for startups and DAOs to maintain cleaner records before compliance questions turn urgent.