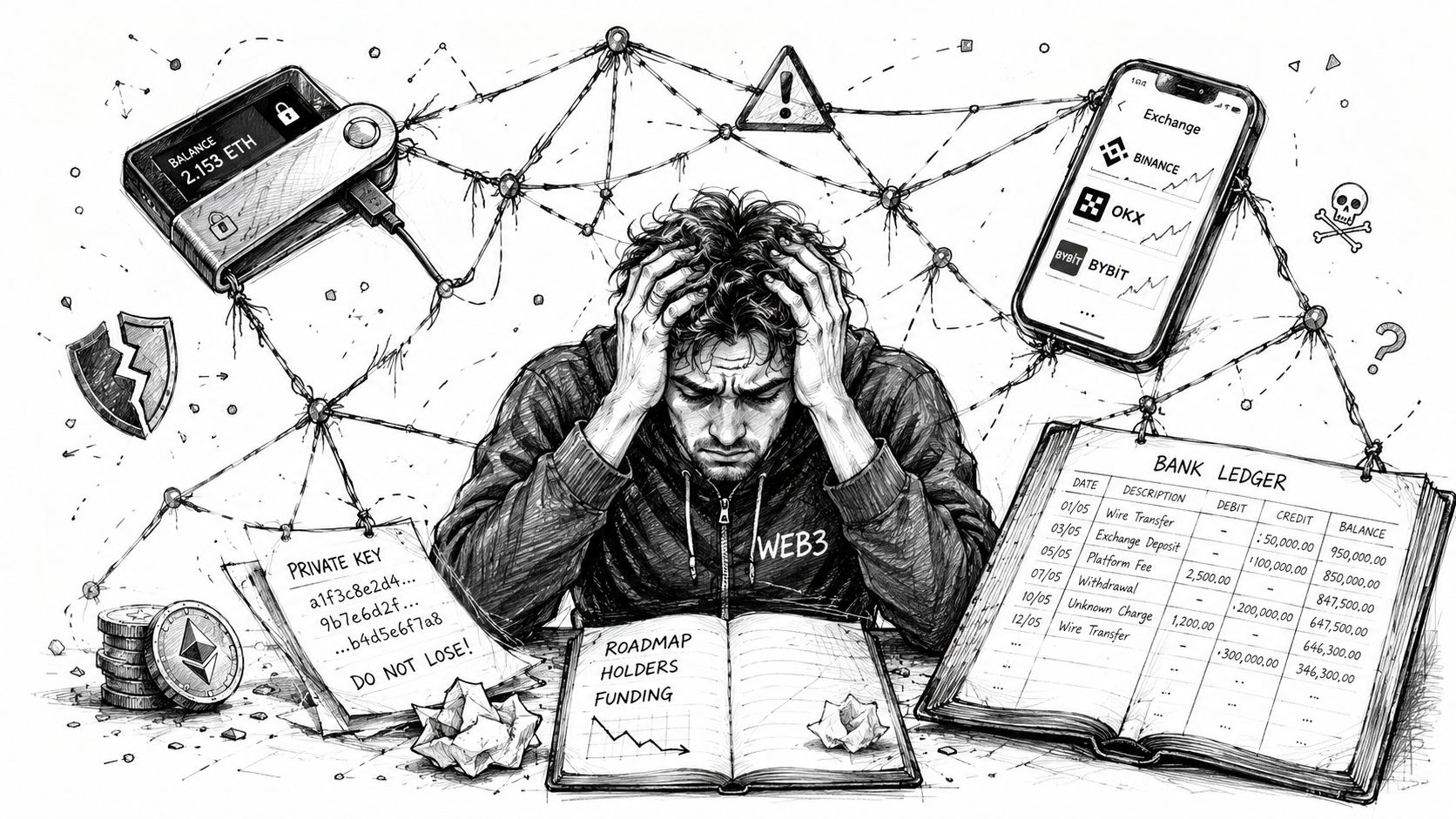

Your finance lead has one balance in a bank portal, another on an exchange, a treasury wallet on a founder's hardware device, and vendor payments waiting on someone in a different time zone to approve a transfer. Meanwhile, accounting needs clean records, legal wants to know who controls the keys, and operations just wants payroll and supplier payments to clear without drama.

That's the point where digital asset custody stops being a crypto topic and becomes an operating model problem.

Failure doesn't typically stem from misunderstanding wallets. It stems from running a real business on top of fragmented access, informal approvals, and tools that weren't designed for shared control. The risk isn't only theft. It's also delayed settlements, missing audit trails, mistaken transfers, sanction exposure, and a treasury setup that can't scale when more people, entities, and currencies enter the picture.

Table of Contents

- Security is mostly workflow design

- Compliance lives inside the custody process

- Insurance needs line-by-line reading

- The shortlist questions that matter

- The settlement layer is part of custody

- What a good choice feels like operationally

- What happens if my custodian goes bankrupt

- Is self-custody safer for a startup

- Why is crypto-to-fiat settlement part of custody diligence

- What should we test before going live

The Hidden Risk in Your Web3 Treasury

A familiar setup looks like this. The company raised in stablecoins, keeps some reserves on an exchange for convenience, stores long-term holdings on a hardware wallet, and receives fiat into a traditional business account. Nobody planned it that way. It just happened as the company grew.

Then the actual problems show up.

A contractor needs payment in fiat, but treasury sits in crypto. A founder is traveling and has the only device that can move funds. A bookkeeper can see outgoing wires but can't trace the wallet that funded them. Compliance asks who approved an on-chain transfer, and the answer is buried in chat screenshots.

Where treasury setups break first

The first break usually isn't a hack. It's governance.

When one person controls a signing device, your company has a key-person risk. When assets sit across exchanges and wallets with different ownership assumptions, reconciliation turns slow and error-prone. When crypto and fiat operations live in separate systems, every conversion becomes a handoff between teams, tools, and counterparties.

Practical rule: If your treasury process depends on memory, chat approvals, or one individual's hardware wallet, you don't have a custody process. You have a temporary workaround.

That's why the old phrase “not your keys, not your coin” still matters, but businesses need a more operational reading of it. The useful version isn't ideological. It's about control design, recovery paths, and who can authorize movement of funds under policy. For a grounded refresher, Coiner Blog's essential insights on crypto security are a helpful baseline.

Why businesses need structure, not just storage

A startup can survive ad hoc wallet management for a while. It can't run payroll, vendor payments, treasury conversions, and investor reporting that way for long.

Digital asset custody solves a business problem: who controls assets, under what rules, with what approval flow, and with what evidence after the fact. Good custody reduces the chance of catastrophic loss, but it also reduces daily friction. It gives finance, operations, legal, and leadership a shared control layer instead of a pile of disconnected accounts.

What Is Digital Asset Custody

Digital asset custody is the professional safekeeping and controlled management of the private keys that represent ownership of crypto and other on-chain assets. For a business, that means more than “where coins are stored.” It means the infrastructure and policies used to authorize transactions, enforce approvals, recover access, and maintain records.

The easiest analogy is a high-security vault built for programmable money. A personal wallet gives one person direct possession. A custody setup gives an organization controlled access with rules.

What custody actually covers

For a company, custody usually includes several layers working together:

- Key protection: How private key operations are secured so theft, loss, or unilateral control are less likely.

- Transaction governance: Who can initiate, review, approve, and release transfers.

- Operational access: How your team moves assets without exposing root credentials.

- Recordkeeping: How you prove what happened, who approved it, and when.

- Recovery planning: How the company regains control if a device, employee, or provider becomes unavailable.

That's the difference between a wallet and a custody system. A wallet helps you hold assets. Custody helps an organization operate around them.

Why this matters now

The scale of the market changed the standard. The digital asset market reached roughly $1.6 trillion by the end of 2023, more than doubling from the start of that year, and the approval of spot Bitcoin and Ethereum ETFs in 2024 increased the need for institutional-grade safekeeping of on-chain assets, according to LSEG's digital asset market research.

That matters because businesses now hold digital assets in more forms than just speculative crypto. Treasury reserves, stablecoin payment balances, tokenized assets, and operational working capital all create the same basic question: how do you protect the keys while still moving at business speed?

Custody is where ownership, controls, and operations meet. If one of those is missing, the setup won't hold under pressure.

An exchange account can feel like custody because assets appear in a dashboard. But exchange access is still exchange access. It's a platform relationship first. A custody arrangement is designed around asset control, policy enforcement, and survivability when staff changes, markets turn volatile, or regulators ask hard questions.

Comparing Digital Asset Custody Models

There isn't one right custody model. There's only a fit between your operating reality and your risk tolerance. Early teams often overcorrect in one of two directions. They either keep everything in founder-controlled wallets for “sovereignty,” or they outsource everything to a third party and lose operational flexibility.

Most businesses need to compare control, workload, and settlement needs together.

Custody Model Comparison

| Attribute | Self-Custody | Third-Party Custody | Hybrid Model (MPC-based) |

|---|---|---|---|

| Control | Highest direct control. Your team manages keys and workflows. | Lower direct control. Provider manages core custody infrastructure. | Shared control. Your team keeps policy authority while using managed infrastructure. |

| Security burden | Highest. Your team owns device security, backup design, access reviews, and recovery. | Lower internal burden, but you inherit provider and legal dependency risk. | Balanced. Strong technical controls with fewer internal single points of failure. |

| Operational overhead | Heavy. Good for small, highly technical teams. Harder for finance operations. | Simpler day to day. Better for teams that need outsourcing. | Moderate. More setup than exchange storage, less burden than pure self-custody. |

| Scalability | Often weak once multiple approvers, entities, and currencies are involved. | Can scale well if the provider supports your workflows. | Usually strongest for companies needing approvals, automation, and on-chain activity. |

| Speed of execution | Can be fast or painfully slow, depending on who holds devices and signs. | Often efficient, but process may depend on provider operating windows or controls. | Strong for teams that need policy-based approvals and continuous operations. |

| Best fit | Small treasuries with technical operators and simple workflows. | Firms prioritizing delegation and external infrastructure. | Companies balancing governance, flexibility, and business continuity. |

What works and what doesn't

Self-custody works when the team is small, technically disciplined, and willing to treat key management like a formal internal control function. It breaks when founders try to scale it informally. Once there are board approvals, entity-level permissions, and recurring vendor payouts, the manual process becomes the risk.

Third-party custody works when legal structure, service levels, and controls are clear. It doesn't work well if your business needs frequent on-chain operations, fast conversions, or custom treasury workflows and the provider forces you into a rigid operating model.

Hybrid custody, often built around MPC, tends to be the practical middle ground. It keeps your team in the approval loop without making your team manually hold every sensitive credential.

If you're evaluating the trade-offs in self-managed wallets before moving to business-grade controls, this breakdown of self-custody wallet benefits and risks is useful context.

The extra factor most teams miss

Global businesses shouldn't evaluate custody in isolation from market access and settlement behavior. The custody model that looks fine on paper may create friction when you need to convert, move, or source liquidity across jurisdictions and providers. If your team is comparing operational environments across regions, Zaro's guide to compare SA cryptocurrency exchanges is a practical example of how venue differences affect real treasury execution.

A custody model should reduce operational dependency. If it creates more waiting, more manual reconciliation, or more person-based approvals, it's the wrong fit.

The Technology Powering Secure Custody

Institutional custody isn't built on one magic tool. It's a stack of controls designed to remove single points of failure. The most important piece today is Multi-Party Computation, or MPC.

MPC splits private key operations across multiple secure environments so no single entity ever holds the full private key. That reduces compromise risk and supports policy-based approvals, according to this overview of MPC in digital asset custody.

How MPC changes the failure model

Think of MPC as a signing process that requires multiple protected participants, but without assembling a complete key in one place. That design matters because many business losses come from concentration. One compromised laptop, one rogue admin, one exposed backup phrase, one rushed approval. MPC is built to stop that pattern.

For a finance team, the practical upside is simple:

- Approvals can be distributed across roles instead of concentrated in one operator.

- Transactions can follow policy such as maker-checker workflows, limits, and review gates.

- Recovery is more manageable because access doesn't depend on a single device or person.

Where HSMs and secure hardware fit

MPC solves the key concentration problem. Hardware-backed protection helps secure the environments where cryptographic operations happen. That's where Hardware Security Modules, or HSMs, and secure enclaves come in.

They act like hardened safes for sensitive cryptographic activity. In business terms, they lower the odds that a standard workstation, mobile device, or server becomes the weak point in your custody design.

For teams that want a plain-English grounding in the underlying concepts, GoSafe's piece on practical cryptography for MSPs is a useful read because it connects cryptographic ideas back to operational protection.

You can also see how business-oriented MPC wallet design is framed in this Spanish guide to MPC crypto wallets for secure digital assets.

Good custody technology doesn't just block attackers. It also limits the damage a trusted insider, lost device, or rushed process can cause.

Multi-signature wallets still have a place in some setups, especially where independent approvals matter. But for companies handling active treasury operations, MPC often gives a smoother balance between security and day-to-day execution.

Navigating Security, Compliance, and Insurance

Teams often focus on key protection and stop there. That's incomplete. A business custody framework stands on three legs: technical controls, operating policy, and financial risk transfer.

If one is weak, the whole system becomes fragile.

Security is mostly workflow design

A secure setup starts with infrastructure, but day-to-day safety comes from boring rules. Who can create a wallet? Who can add a whitelisted address? Who can initiate a transfer above the normal operating band? Who reviews destination details before release?

The strongest teams use layered controls such as:

- Role separation: One person initiates, another reviews, a different person approves higher-risk actions.

- Transaction policies: Different limits for payroll, trading, treasury rebalancing, and unusual destinations.

- Address controls: Internal review before new counterparties or wallet destinations become usable.

- Access hygiene: Tight user provisioning, mandatory MFA, and immediate access changes after role updates.

Compliance lives inside the custody process

Institutional custody infrastructure must use both MPC and hardware-backed protection such as HSMs, while supporting real-time sanctions screening and Travel Rule compliance under frameworks including DORA and MiCA, as explained in Fireblocks' review of custody strategy for banks.

That matters because compliance failures rarely happen in a vacuum. They happen during movement of funds. Treasury converts crypto to fiat. Ops pays a vendor. A new wallet appears in a workflow. If screening and policy checks sit outside the custody flow, people route around them.

For a compliance-focused perspective on how institutional crypto infrastructure is being handled in practice, this look at Anchorage Digital compliance success in crypto banking is a relevant reference point.

Insurance doesn't fix a bad control environment. It only narrows the financial damage from specific failures that the policy actually covers.

Insurance needs line-by-line reading

A lot of teams ask, “Is it insured?” That's too broad to be useful.

The better questions are narrower. Does coverage apply to assets in cold storage only, or also in more active environments? Does it cover internal fraud? What about losses from a transaction that was properly authorized but sent to the wrong address? What exclusions apply when a breach involved compromised user credentials rather than custodian infrastructure?

Insurance helps. It does not replace transaction governance or legal diligence. If your approval chain can authorize an irreversible but mistaken transfer, the policy may offer less protection than your team expects.

How to Choose Your Custody Partner

Vendor selection gets harder as the market matures. The global digital asset custody market is projected to reach USD 7.08 trillion by 2035, and top providers including Coinbase Custody, BitGo, and Fireblocks hold a significant share of the market, which makes careful evaluation more important, according to Business Research Insights on the digital asset custody market.

That growth is useful context, but your choice still comes down to operating fit.

The shortlist questions that matter

Don't start with marketing pages. Start with failure scenarios.

Ask each provider:

- How is key control structured? You want a precise explanation of MPC, hardware protections, approval flow, and recovery design.

- What happens during urgent movement of funds? Treasury doesn't only store assets. It converts, settles, pays, and rebalances.

- How are users and roles managed? Finance, founders, legal, and operations shouldn't share the same permissions.

- What visibility do we get? You need audit trails, transaction status, and clear evidence of who approved what.

- What's the legal treatment of client assets? This matters as much as the tech.

- How does fiat settlement connect to custody? For many businesses, this is the hidden make-or-break issue.

The settlement layer is part of custody

Many custody evaluations falter in this regard. A provider may secure keys well but still create operational friction when your team needs to convert crypto to fiat and push funds into payroll, vendor payments, or treasury accounts.

If your business handles both rails, ask about:

- Conversion workflow: Who executes the crypto-to-fiat step, and how much manual handling is involved?

- Settlement timing: Can treasury act when markets move, or are you waiting on operational windows?

- Counterparty exposure: What entities are involved between asset movement and fiat arrival?

- Reconciliation: Can accounting trace the path from wallet debit to fiat credit cleanly?

One option in this category is OneSafe, which combines multi-currency business accounts, payments, cards, and crypto-compatible treasury workflows in one interface, while using Fireblocks-based custody as part of its security model. That kind of combined setup can matter when the primary issue isn't only storage. It's reducing the handoffs between custody, conversion, banking, and spend management.

A quick product walkthrough is useful when you're evaluating how these workflows look in practice.

What a good choice feels like operationally

The right partner makes treasury less person-dependent. Approvals are clear. Conversions are traceable. Fiat and crypto movements don't require a relay race across unrelated tools. Finance can work from policy instead of memory.

If you leave a vendor demo thinking mainly about security buzzwords, keep digging. The ultimate test is whether your team can run normal business operations faster, with fewer risky handoffs and better evidence.

Frequently Asked Questions on Business Custody

What happens if my custodian goes bankrupt

This is one of the most important diligence questions. State Street notes that clients directly ask, “If my custodian goes bankrupt, will I get my assets back?” and that legal segregation of customer assets from a custodian's liabilities is an essential but often poorly explained issue in digital asset custody, as described in its discussion of digital asset custody questions from clients.

The practical takeaway is simple: don't assume technical security answers the insolvency question. You need to examine client asset segregation, legal title, account structure, and the contractual path for asset return or transfer.

Is self-custody safer for a startup

It can be, if the team is highly disciplined and the workflow is simple. It can also be far less safe if “self-custody” really means one or two people informally managing treasury from personal devices. Startups often underestimate backup design, access rotation, and approval governance.

Why is crypto-to-fiat settlement part of custody diligence

Because that's when business risk becomes real cash-flow risk. A wallet may be secure, but your company still needs funds to land in the right fiat account, on time, with enough visibility for accounting and compliance. If conversion and settlement happen through separate manual steps, the exposure shifts from key loss to timing, counterparty, and process failure.

What should we test before going live

Run a dry exercise. Set user roles. Approve a small transfer. Add a new destination. Simulate a staff absence. Review the audit trail. Confirm how crypto becomes fiat and where that step is controlled. If the process feels fragile in rehearsal, it will fail under pressure.

If your team is trying to reduce the gap between crypto treasury and day-to-day business finance, OneSafe is worth evaluating. It's built for companies operating across fiat and digital assets, with multi-currency accounts, payment rails, cards, and crypto-compatible workflows in one place, so custody doesn't sit off to the side as a separate operational silo.