UPI now handles hundreds of millions of transactions a day in India. At that scale, it stops looking like a domestic payment feature and starts looking like core financial infrastructure.

For readers outside India, especially founders used to cards, ACH, SWIFT, stablecoins, or local bank transfer schemes, the easiest way to place UPI is to compare it to a bank-native, always-on payment rail with a shared address layer on top. Apps sit on the surface. The rail sits underneath. A user can pay from one bank account to another in real time without needing the sender and receiver to use the same app.

That distinction matters for international businesses. UPI is not only a consumer checkout option. It is a system you can use to collect funds from customers in India, pay local contractors and partners, and connect Indian rupee flows to broader treasury and on-ramp operations. If you run a global finance stack, UPI belongs in the same conversation as Faster Payments in the UK, PIX in Brazil, card acquiring, and crypto fiat ramps.

India launched UPI in 2016 through the National Payments Corporation of India, under the oversight of the Reserve Bank of India. Since then, it has grown into the default layer for a large share of the country's digital payments. For a web3 operator, that makes UPI interesting for a practical reason. It is one of the clearest examples of what happens when identity, routing, and instant bank settlement are combined into one interoperable network.

The result is simple for the end user and strategically important for everyone else. A payment experience that feels as fast as sending a message can still move through regulated bank accounts, at national scale.

Table of Contents

- What Is UPI and Why It Matters Globally

- The four main players

- What a VPA actually does

- A typical QR payment flow

- Why this architecture matters to product builders

- Payment rail comparison

- Where UPI beats legacy expectations

- Where UPI does not replace everything

- Why IMPS still comes up

- Accepting payments from Indian customers

- Paying Indian contractors and vendors

- UPI and crypto on-ramps

- The mental shift for international founders

What Is UPI and Why It Matters Globally

More than 640 million transactions now move through UPI each day, which is why global operators can no longer file it under "local payment method" and move on.

UPI is a bank-to-bank payment protocol that gives India a shared payment language. Many apps can sit on top of it, many banks can connect to it, and money still moves between bank accounts using one common standard. For a reader used to cards, ACH, wires, or stablecoin transfers, the closest comparison is a real-time payment rail with a universal addressing layer and broad app-level interoperability.

That design changes the business question.

In many markets, companies piece together different rails for different jobs. Cards handle checkout. Wires handle larger international transfers. ACH-type systems handle lower-cost bank movement with some delay. Wallets often stay inside their own closed loop. UPI reduces that fragmentation for domestic Indian payments. A customer can pay from one app, a merchant can accept with another, and both still settle through the banking system.

For international and web3 businesses, that matters less as a consumer story and more as an operations story. If you collect revenue from Indian users, UPI is often the expected local rail. If you pay Indian contractors, agencies, or suppliers, UPI reshapes expectations around speed and account-to-account delivery. If you build crypto or fintech products, UPI is a useful case study in how a fiat rail can become a practical on-ramp into digital finance behavior without requiring users to learn banking details, card networks, or crypto-native flows first.

A useful analogy is API standardization. Before a common API spec, every integration is custom work. After a common spec, many front ends and many service providers can connect to the same underlying system. UPI applies that logic to money movement. The result is not just convenience for Indian consumers. It is a lower-friction way for global businesses to plug into India's domestic payment habits.

UPI's scale changes the global conversation because scale reveals whether a payment system is a side option or core infrastructure. As noted earlier, UPI has grown into the world's largest real-time payment system by transaction volume. It supports a very large share of India's banking ecosystem and handles payment frequency that rivals, and in some measures exceeds, the largest global card networks on a daily basis.

That does not mean every cross-border flow can run on UPI today. It does mean any company with Indian customers, Indian counterparties, or India-linked treasury paths should treat UPI as a core domestic rail with global operational implications.

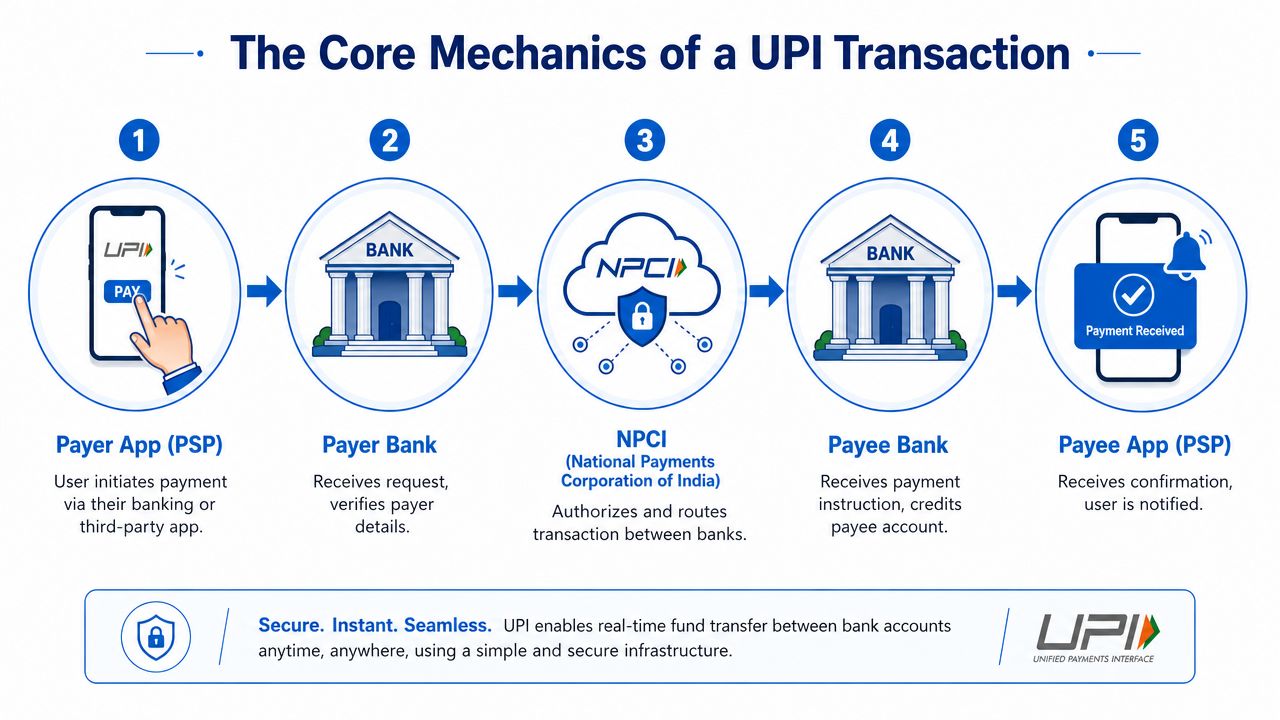

The Core Mechanics of a UPI Transaction

A UPI payment feels simple because the complexity sits in the network, not in the user experience.

From the outside, it looks like this: scan a QR code, enter an amount, approve with a PIN, done. Underneath, a few distinct parties coordinate in seconds so the payer and payee don't need to exchange bank account details directly.

The four main players

A useful mental model is a digital postman.

- Payer app: The sender uses an app such as a bank app or a third-party payment app to initiate the payment.

- Payer bank: The sender's bank checks whether the payment request is valid and whether the account can authorize it.

- NPCI switch: The National Payments Corporation of India acts like the routing hub. It doesn't behave like a consumer wallet. It coordinates the message flow between the institutions.

- Payee bank and app: The recipient's bank receives the instruction and credits the account, while the recipient's app confirms receipt.

What a VPA actually does

One of the most confusing parts for non-Indian readers is the Virtual Payment Address, often called a VPA or UPI ID.

A VPA is best understood as a stable alias for a bank account. Instead of asking for an account number and routing code, someone can pay name@bank or scan a QR that resolves to that identifier. The sender doesn't need the underlying account details, and the receiver doesn't need to expose them.

If you come from crypto, this feels familiar. A wallet address lets a network route value without revealing every internal system detail behind custody and compliance. A VPA does something similar for bank payments, but in a more user-friendly, human-readable format.

A typical QR payment flow

Here's the plain-English sequence for a merchant payment:

- The buyer opens a UPI app and scans the merchant's QR code.

- The app reads the merchant's VPA and prepares the payment request.

- The buyer enters the amount, or the amount is prefilled in some checkout flows.

- The buyer approves with a UPI PIN.

- The request moves through the network, reaching the relevant banks through the central switch.

- The merchant receives confirmation inside their app or payment system.

This is why UPI often feels simpler than card checkout. There's no card number to type, no expiry date, no CVV, and no merchant need to store card credentials.

Practical rule: When people ask “what is UPI,” the shortest accurate answer is: it's a shared bank transfer network with app-level convenience.

Why this architecture matters to product builders

The breakthrough isn't only speed. It's interoperability plus abstraction.

Apps can compete on experience while still using a common payment rail. Banks remain in the loop. Merchants can accept payments without forcing customers into one closed ecosystem. That's why UPI is interesting to web3 builders too. It shows how a standard can separate the interface layer from the value-transfer layer without fragmenting liquidity.

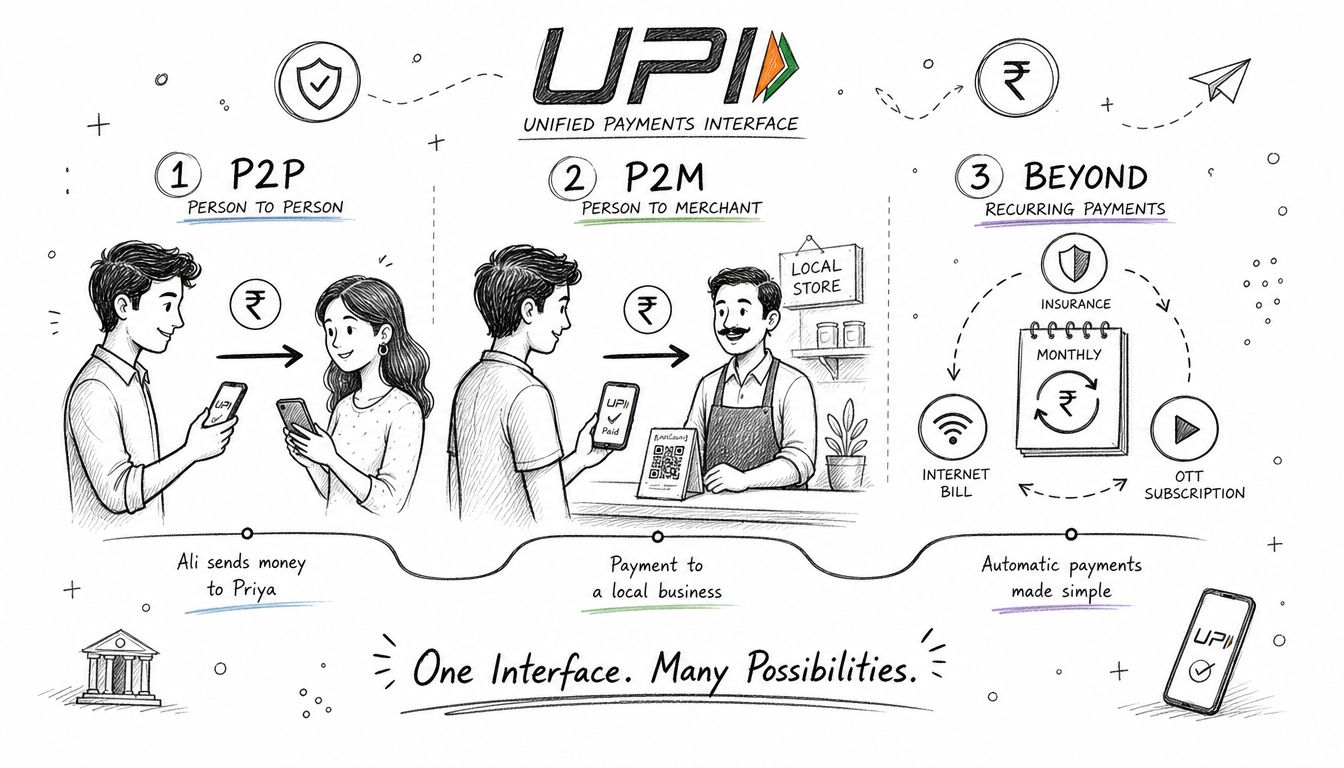

P2P, P2M, and Beyond The Main UPI Transaction Types

Once you understand the rail, the next question is how people use it. UPI supports several payment patterns, but most real-world usage falls into a few recognizable buckets.

P2P payments

P2P means person-to-person.

This is the easiest category to map to Western products. A friend repays another friend for dinner. A family member sends money home. A roommate covers utilities and gets reimbursed. The sender chooses a contact, mobile-linked identity, or VPA, enters the amount, and approves the transaction.

For users, P2P is where UPI feels most like Venmo or Cash App. The difference is that the money movement is bank-native, not trapped in a proprietary balance.

P2M payments

P2M means person-to-merchant.

Here, UPI becomes more relevant for businesses. A customer pays a store, restaurant, freelancer, software seller, or online merchant using the same underlying rail. The merchant doesn't need card details from the customer. The customer doesn't need to trust a separate wallet balance.

There are three common P2M patterns:

- Scan and pay: A customer scans a QR code at a shop counter or from a screen during checkout.

- Intent flow: Another app hands off the payment to a UPI app already installed on the phone. The user authorizes and returns.

- Collect request: A merchant sends a request for payment, similar to a lightweight invoice prompt inside the UPI flow.

How the three methods feel in practice

A quick comparison helps:

| Method | Best for | What the user does |

|---|---|---|

| Scan and pay | In-person payments | Scans a QR and approves |

| Intent | Mobile app checkout | Gets redirected to a UPI app and confirms |

| Collect request | Invoice-like requests | Receives a payment request and accepts it |

Each method solves a different product problem. QR works well when buyer and seller are in the same place. Intent is cleaner for app-based commerce. Collect works when the seller initiates the payment request.

Beyond simple one-off payments

UPI also supports broader use cases than “send money now.”

Teams can use it for bill payments, merchant collections, and recurring flows where the user experience needs to stay lightweight. That's one reason UPI became infrastructure rather than a passing consumer trend. It can support both tiny retail interactions and more structured commercial flows without changing the user's mental model.

For a non-Indian company, that consistency is the key insight. Whether you're collecting from a consumer, paying a local contractor through a domestic partner workflow, or supporting a fiat entry path for users, the same network logic applies.

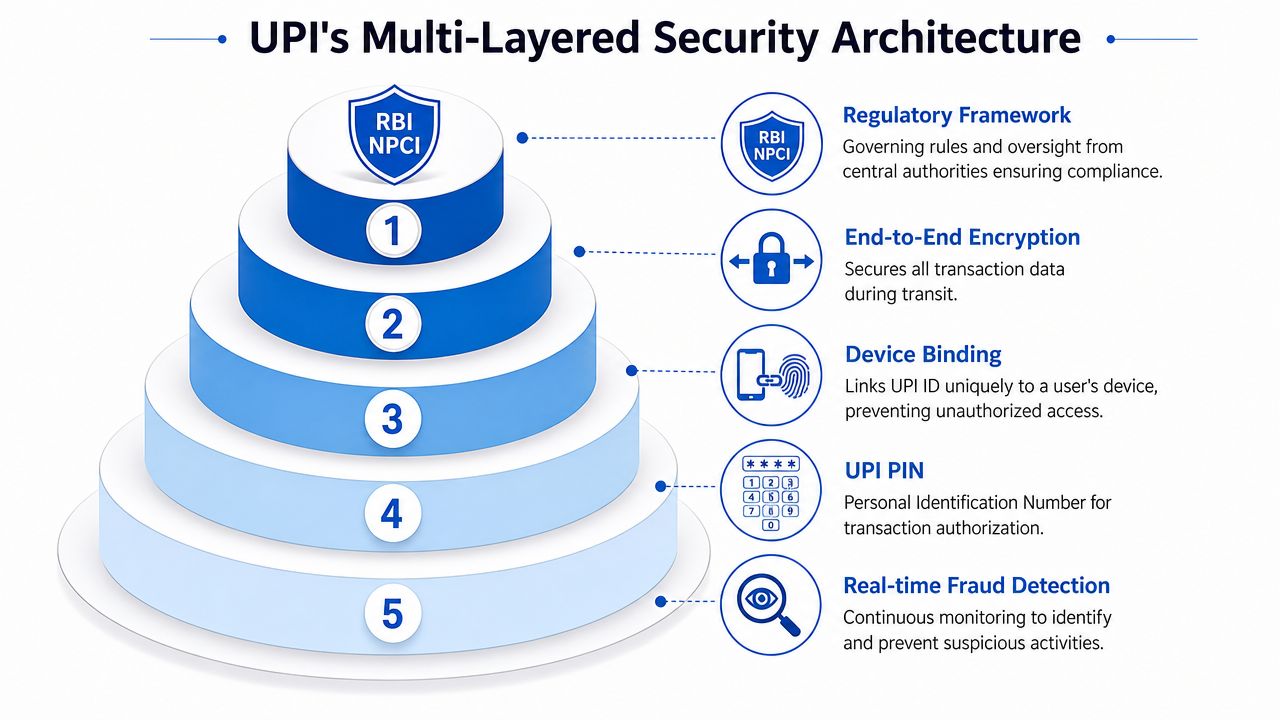

Security Layers, Settlement, and Rules of the Road

UPI processes payments at a scale that would break weaker systems, so its trust model matters as much as its speed. For an international business, this is the part that answers a practical question: can a domestic real-time rail in India be reliable enough for collections, contractor payouts, and fiat movement tied to a global treasury stack?

The authentication model

UPI uses a two-factor model built around device possession and PIN knowledge. As described in this security architecture analysis of UPI, the flow can include SIM binding during registration, device fingerprinting, app-specific tokens, a UPI PIN for authorization, failed-attempt controls, RSA-2048 for secure transmission, and PBKDF2-based PIN hashing.

A useful comparison for non-Indian readers is modern wallet security mixed with bank-grade authorization. The phone acts like a registered hardware endpoint. The PIN acts like the transaction approval secret. One credential alone is not enough.

That design matters for fraud control and for product design. If you are building a fiat on-ramp or local payout flow, you are not asking users to type long account numbers or hand over reusable card credentials. You are asking them to approve a bank-to-bank transfer from a known device inside an interoperable app environment.

If you want a broader explanation of how financial systems handle encryption choices and key protection, this overview of AES-256 and banking security models provides useful context.

Settlement and what “instant” really means

UPI feels instant at the user layer because the payer and recipient see confirmation quickly. For operators, the better mental model is a high-speed messaging and authorization rail tied to bank accounts, with reconciliation and interbank settlement handled underneath the interface.

That distinction is familiar to card and crypto teams.

A card authorization can look final to the customer before downstream settlement files finish moving. A stablecoin transfer can settle onchain immediately, while the business still has offchain bookkeeping to complete. UPI sits closer to real-time bank transfer infrastructure, but the same product lesson applies. User confirmation, bank posting, and institutional reconciliation are related steps, not one giant atomic event.

For a global company, this affects treasury operations. If you collect from Indian users through UPI, your customer experience can be immediate while your internal finance team still needs the right partner setup for settlement timing, reporting, refunds, and exception handling.

Limits and special rules

The Reserve Bank of India sets operating rules around use cases and limits. As noted in the security analysis cited earlier, limits have been expanded for some categories such as hospitals and educational institutions, while UPI Lite is designed for small-value transactions with money stored on-device to reduce checkout friction.

UPI also supports UPI 123PAY for feature phones through channels such as IVR and missed-call based flows. That is easy to overlook if you only view UPI through the lens of smartphone apps.

The broader point is infrastructure coverage. UPI was built to serve a wide range of devices, banks, and user conditions inside India. For international businesses, that makes it more than a consumer checkout button. It is a regulated domestic rail you can use, through local partners, as part of a larger cross-border operating system: collect funds from Indian customers, pay India-based contractors, or move users from local bank money into a wallet, exchange, or platform flow with fewer steps than cards or wires.

UPI vs SWIFT, Cards, and IMPS A Global Comparison

For an international operator, the main question isn't just “what is UPI.” It's “where does it fit among the rails I already use?”

The short answer is that UPI occupies a different position from cards and SWIFT. Cards optimize merchant acceptance on global card networks. SWIFT coordinates cross-border bank messaging. ACH and SEPA handle bank transfers inside certain geographies. UPI is a domestic real-time bank rail with app-native usability.

Payment rail comparison

| Feature | UPI | Credit/Debit Cards | SWIFT | ACH / SEPA |

|---|---|---|---|---|

| Primary model | Bank-to-bank real-time payments through interoperable apps | Card network authorization and settlement | Interbank cross-border messaging and transfers | Domestic or regional bank transfers |

| User credential | VPA, QR, or app-based identity | Card number and card credentials | Bank account and bank transfer details | Bank account details |

| Typical use case | Everyday transfers and merchant payments in India | Consumer commerce, online and offline | International business payments | Payroll, bill pay, domestic transfers |

| Experience | Mobile-native and direct | Familiar for merchants, but more credential-heavy | Operationally heavier | Usually simpler than wires, less immediate in feel |

| Interoperability | High within the UPI ecosystem | High across card-accepting merchants | High across participating banks | High within supported banking zones |

Where UPI beats legacy expectations

UPI's strongest advantage is user experience with bank-native movement.

Cards are excellent for broad acceptance, but they come with card credentials, chargeback logic, and merchant acquiring complexity. SWIFT works for international movement, but it isn't designed to feel lightweight for retail or everyday contractor payouts. ACH and SEPA are useful bank rails, but they usually don't feel as app-centric or instant to users.

UPI changes the interface. Paying someone can feel closer to sending a chat request than filling out banking instructions.

Where UPI does not replace everything

UPI doesn't replace cross-border banking by itself. If your company operates in the US and Europe, you still need local collection accounts, treasury controls, compliance workflows, FX management, and payout infrastructure. UPI is best understood as a high-performance domestic rail inside India that can plug into broader global finance operations.

For teams comparing Indian payment products, this breakdown of Airwallex versus PhonePe in business payment contexts helps illustrate how local payment behavior and global finance stacks intersect.

Why IMPS still comes up

You'll also hear UPI compared with IMPS, another Indian instant transfer system. The practical difference is mostly about usability. IMPS is more like a direct transfer tool. UPI wraps a richer interface and identity layer around domestic bank movement, which is why it became the mainstream consumer and merchant experience.

That's the lesson for product builders: superior rails matter, but the abstraction layer often decides adoption.

Putting UPI to Work in Your Global Business

If you run a global company, UPI becomes useful when India is part of your money flow. That could mean customer collections, local vendor payments, contractor payouts, or treasury workflows that need a domestic leg inside India.

Accepting payments from Indian customers

Most foreign businesses won't connect to UPI as if they were a local Indian bank. In practice, they usually work through a local payment gateway, aggregator, or regulated partner that exposes UPI acceptance inside a broader checkout stack.

That setup matters for ecommerce, SaaS, gaming, creator platforms, and marketplaces selling into India. If your user base expects UPI and you only offer cards, your checkout can feel imported rather than local. Even when the product is global, the payment preference is local.

Paying Indian contractors and vendors

Finance teams often first encounter challenges with international wire transfers, which can be operationally heavy, slower to reconcile, and awkward for small or frequent payouts. Domestic receipt expectations in India are shaped by fast account-to-account movement, so a local payout rail can dramatically improve the experience for the person getting paid.

A common operating model looks like this:

- Your company funds a cross-border payment workflow through its business banking or treasury provider.

- A regulated partner handles the local leg in India and routes the payout into the domestic banking environment.

- The recipient receives funds through a familiar local method, often tied to the same behavioral expectations UPI created.

For teams building this stack, the challenge isn't just sending money. It's controlling FX, compliance, approvals, and reconciliation across multiple rails. That's why businesses often need infrastructure purpose-built for cross-border payments and treasury operations, not just a one-off transfer tool.

The operational win isn't only speed. It's reducing the gap between global treasury systems and local payout expectations.

UPI and crypto on-ramps

For web3 businesses, UPI matters because fiat on-ramps are rarely abstract. They're local, behavioral, and firmly tied to trust. In India, many users understand digital finance through mobile-first bank transfers and QR-based payment experiences. That makes UPI-adjacent flows highly relevant when a platform needs to bridge fiat into crypto participation.

A trading platform, wallet, or web3 payroll product may still need regulated intermediaries and banking partners. But if the user's starting point is local fiat, then understanding UPI is part of understanding the funnel.

A short walkthrough helps visualize how modern fintech stacks connect local rails with global operations:

The mental shift for international founders

Don't treat UPI as “India's version of cards.” That framing is too shallow.

Treat it as critical domestic payment infrastructure inside one of the world's most important digital economies. Once you see it that way, the use cases become obvious. You localize checkout. You improve payout design. You connect domestic collection and disbursement into a global finance stack. And if you operate in web3, you stop pretending fiat rails are secondary to the product.

The Future of UPI From Local Hero to Global Standard

UPI's long-term significance isn't limited to India. The more interesting question is whether UPI becomes a model for how countries connect real-time domestic payment systems to each other.

That idea is compelling because it attacks a stubborn global problem. Cross-border money still depends heavily on layered intermediaries, banking cutoffs, and fragmented user experiences. UPI suggests a different direction: strong domestic rails first, then interoperability between them.

What global finance can learn from it

Three lessons stand out:

- Interoperability beats app silos: Users don't need every payer and payee to share one branded wallet.

- Abstraction drives adoption: People use aliases, QR codes, and simple approval flows instead of raw bank details.

- Public infrastructure can enable private innovation: Banks, apps, and merchants can all build on top of a common standard.

Why this matters for web3 too

Web3 teams often talk about global money movement as if crypto alone solves the full stack. It doesn't. Users still enter and exit through local fiat systems. Treasury teams still reconcile against bank accounts. Vendors still want predictable settlement in the currency they use to live and operate.

UPI is a reminder that the future probably isn't one universal rail. It's a network of interoperable rails, where domestic systems do what they do best and global platforms connect them cleanly.

That's why “what is UPI” is a bigger question than it sounds. You're not just asking about an Indian payment method. You're looking at one of the clearest examples of how modern money infrastructure can be fast, interoperable, mobile-native, and broadly adopted.

If your company needs to connect local payment rails, global treasury, and crypto workflows in one place, OneSafe is built for that operating reality. It gives global and web3 businesses a way to manage multi-currency accounts, cross-border payments, cards, and crypto-linked finance operations through a single platform.